Albania: Staff Concluding Statement of the First Post-Program Monitoring Mission

March 20, 2018

An International Monetary Fund (IMF) mission, led by Ms. Anita Tuladhar, visited Tirana during March 7-20, 2018, for the first Post-Program Monitoring (PPM) discussions. The PPM process is intended for member countries that have substantial IMF credit outstanding following the expiration of their programs, and is especially focused on vulnerabilities and risks. At the end of the visit, the mission issued the following statement:

Albania is enjoying one of the fastest economic growth rates in the region. The macroeconomic and political environment is stable. Policymakers should use these good times to push for reforms to mitigate risks arising from high public debt and contingent liabilities, and non-performing loans in the financial sector; and to strengthen medium term growth potential against a difficult investment climate with high informality and weak rule of law. Key priorities are: advancing fiscal consolidation; enhancing the efficiency of public investment spending; strengthening the institutional framework for bank supervision and Non-Performing Loans (NPLs) resolution; and removing bottlenecks in business/investment environment through judicial and anti-corruption reforms. These efforts will also open the economy to new growth opportunities, help bring Albania closer to European Union (EU) integration and ensure higher standards of living for the Albanian population.

Economic growth remains strong

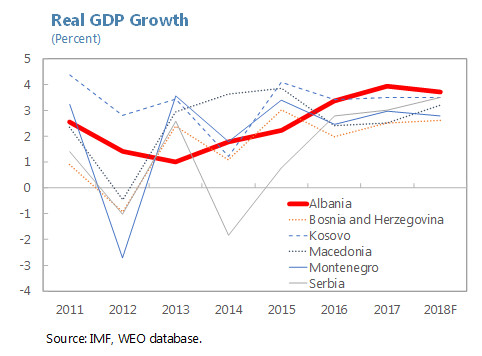

Albania is enjoying one of the fastest economic growth rates in the region with GDP growth projected to reach an estimated 3.9 percent in 2017 and 3.7 percent in 2018. Financing conditions are extremely favorable as inflation and interest rates remain very low. Investment is picking up and confidence remains high. Exports are rising, supported by the strong economic recovery in EU trading partners. The foreign exchange reserves of the Bank of Albania (BoA) are comfortable (at more than 6 months of import coverage) as flows of foreign direct investment continue at a robust pace. While the recovery remains creditless, the banking sector is stable, liquid, and profitable. Albania’s growth outlook remains positive, provided the reform momentum picks up, improving confidence and creating a favorable environment for new investment and growth.

Downside risks remain on the horizon

This economic growth momentum, however, may not last . Growth in the EU has been accelerating since 2016. However, the growth recovery is largely cyclical and the medium-term outlook remains subdued due to unresolved crisis legacy issues, weak productivity growth, and demographic headwinds. There are also global risks from a sudden financial market correction, political uncertainties and protectionist policies which could dampen confidence and growth. A slowdown would adversely affect Albania through trade, investment, and banking channels.

Domestic risks to growth over the medium-term are also important. The tapering of large infrastructure investments in the energy sector is expected to drag down growth. With public debt levels very high by regional standards and contingent liabilities increasing, fiscal slippages could dampen confidence, increase borrowing risk premia and lower private investments. The banking system is already weighed down by large NPLs and difficulties in collateral execution. More rapid deleveraging by EU-owned banks in Albania could lead to financial sector stress. Adverse weather conditions could again affect electricity generation, creating quasi-fiscal risks and headwinds to growth. Insufficient progress in implementing structural reforms, in areas such as energy, public financial management and judicial reforms, can undermine investor confidence, significantly reducing donor and capital inflows, and lowering growth.

Now is the opportune time to accelerate reforms to mitigate these risks and build up defenses against adverse shocks in the future

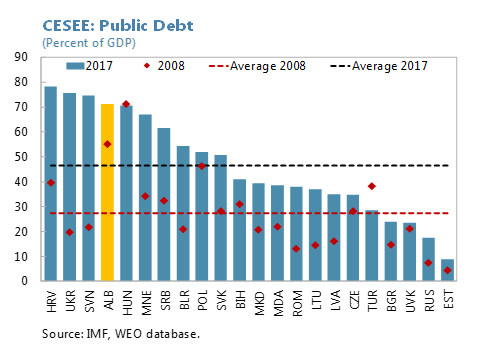

A faster fiscal consolidation is needed to create policy buffers . Given the high level of public debt (71.2 percent of GDP at end-2017, including local and central government arrears of 1.8 percent of GDP), negative shocks such as a slowdown in growth combined with higher interest risk premia and exchange rate depreciation, or realization of contingent liabilities, could adversely affect debt and external sustainability, necessitating a sharp fiscal adjustment. A more ambitious fiscal deficit target—consistent with an additional fiscal effort of around 1 percent of GDP over two years, compared to a constant general government deficit of 2 percent of GDP in the budget—would help achieve faster debt reduction to create additional room for maneuver in case these adverse shocks materialize. In this regard, strengthening revenues is a key priority to not only lower deficits but also create room for more infrastructure and education spending.

Stronger budgetary and public investment management frameworks are needed to mitigate fiscal risks and reduce waste of scarce resources.

- Public investments and public private partnerships (PPPs). As public investment is scaled up, the authorities should address shortcomings in project management, including in local governments and state-owned enterprises (SOEs). Prioritization of all projects, including PPPs, within the public investment envelope is needed, which should be properly funded in the medium-term budgetary framework. With regard to PPPs, a key priority is to reduce the fragmented decision-making and strengthen risk assessment processes at the Ministry of Finance (MOF). These processes are critical given the large contingent liabilities frequently embedded in PPP contracts over a long-term horizon. The current practice of unsolicited proposals should be eliminated. The government’s plan for establishing a development bank for financing public investments should take into account international experience with risks associated with such entities, including fiscal, financial and governance risks.

- Arrears control . Stronger enforcement of budgetary commitment controls iscrucial to prevent the buildup of arrears. Unfunded commitments in the medium-term budget and value-added tax (VAT) refund delays have led to an accumulation of new arrears of around 0.9 percent of GDP in 2017 (of which, 0.7 percent of GDP in VAT refunds), which need to be resolved rapidly.

- State-owned enterprises: Revitalizing reforms in the state-owned electricity sector to put companies on a financially sustainable footing are of critical importance. The authorities should tackle the accumulation of arrears and losses, and improve operational efficiency, including through stronger corporate governance, institutional and market design reforms and better targeting of investment.

Further improvements in debt management can help reduce rollover risks . Albania’s gross financing needs, at around 21 percent of GDP, remain high. The authorities’ plan to support secondary market development for the 5-year government bond market would help reduce this risk. Eurobond issuances should aim to amortize debt in foreign exchange while being vigilant to risk posed by excessive reliance on non-concessional borrowing in foreign currency. The debt management capacity at MoF is not adequate and requires further strengthening. Close coordination between the MoF and BoA and the markets is needed, given the high bank exposure to the public sector.

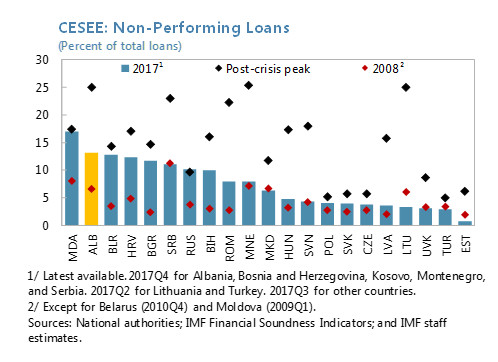

Addressing the resolution framework of NPLs is key to credit recovery. NPLs, at 13.2 percent of loans at end-2017, have been declining due to write-offs and restructuring efforts. Nevertheless, important reforms to accelerate the collateral execution are pending, including success fees for bailiffs and the regulation of out-of-court agreements, making banks risk averse. The authorities should also remain vigilant to potential risks related to large corporate exposures and growth in the construction sector. The recently launched de-euroization strategy would help reduce indirect credit risks from sizable unhedged foreign exchange exposures. This strategy should be implemented gradually to mitigate risks of financial disintermediation.

Enhanced bank supervision and regulation, aligned with EU standards, would provide the BoA with tools to better manage risks of systemic banks and build up capital buffers. The ongoing bank consolidation as EU-owned banks deleverage comes with governance risks. Ensuring that new market entrants have solid banking experience and meet fit and proper criteria to operate in the Albanian banking market will be critical. Strict monitoring of systemic banks should be further strengthened to contain the risk of large borrowers and mitigate the risk of related-party lending. The BoA should continue to align its regulatory and supervisory framework with the EU and progressively converge towards implementation of Basel III. In the non-banking sector, it is critical that the Albanian Financial Supervisory Authority complete the crisis management framework for investment funds, in coordination with the BoA and MOF.

Faster growth is needed to raise living standards and reduce poverty, which requires fundamental institutional reforms

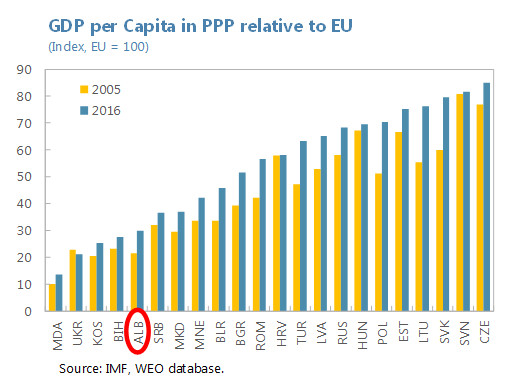

To attract higher investment and achieve faster convergence, Albania needs to address many structural impediments . Weak property rights and a corrupt, inefficient judiciary are frequently identified as the main obstacles for attracting investment. Lack of infrastructure connectivity, high informality, difficulty in accessing finance and weak human capital further undermine competitiveness. Addressing these challenges is all the more critical given the slowdown in investment and productivity growth seen in Albania and across Europe after the global financial crisis. These challenges to growth are exacerbated by high emigration from Albania. Now is the time to implement reforms to improve the investment climate, encourage growth and increase job opportunities.

Ultimately, mitigating risks and implementing the structural reform agenda will set the foundation for resilient growth as well as pave the way towards further EU integration.

The IMF team thanks the authorities and other interlocutors for their cooperation, open and constructive discussions, and warm hospitality.

IMF Communications Department

MEDIA RELATIONS

PRESS OFFICER: Andreas Adriano

Phone: +1 202 623-7100Email: MEDIA@IMF.org