Loading component...

Loading component...

Angola: The Road to Economic Reform

June 11, 2018

View of Luanda: Like other resource-rich countries in Africa, Angola has had to look at its non-oil sectors to offset the drop in revenue and exports (photo: IMF staff)

The IMF recently completed its annual health check of the Angolan economy and found that the country, under a new administration, has made strides in setting a reform agenda geared towards macroeconomic stability and growth that benefits all its people.

Here are some of the report’s highlights:

Since the election last year, the administration of President João Lourenço has started to implement policies aimed at restoring macroeconomic stability and improving governance, including dismissing officials linked to the previous administration, launching investigations into possible misappropriation of funds at several public entities, and creating a specialized anti-corruption unit.

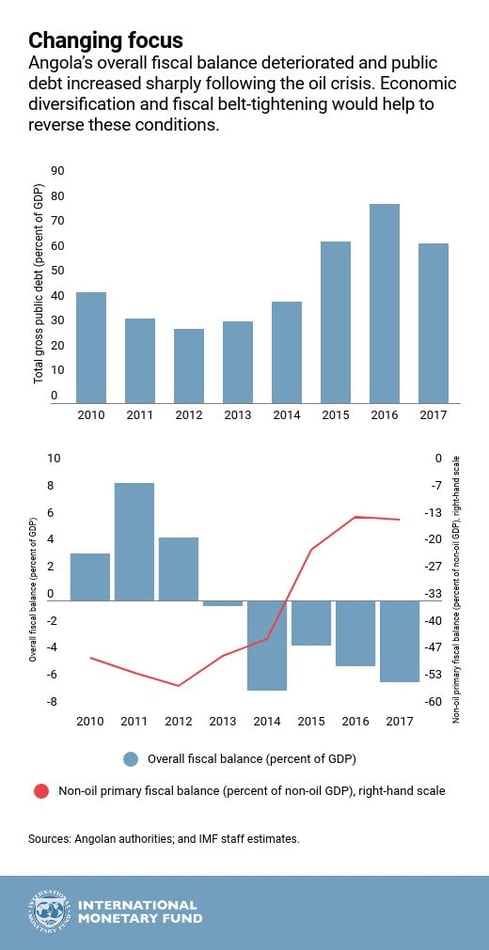

The dramatic drop in oil prices that started in mid-2014 substantially reduced tax revenues and exports, with growth coming to a halt and inflation accelerating sharply. This brought to the fore the need to address vulnerabilities more forcefully and diversify the economy away from oil.

The authorities undertook steps to mitigate the impact of the oil price shock, including a significant—17½ percent of GDP—improvement in the non-oil primary fiscal balance over 2015–16, mainly through spending cuts that included the removal of subsidies, and devaluing the kwanza against the U.S. dollar by over 40 percent between September 2014 and April 2016. The exchange rate, however, was re-pegged to the U.S. dollar in April 2016.

Angola was for many years mired in civil conflict, which destroyed its physical and human capital, and undermined the state’s ability to function normally. Since the conflict ended in 2002, the country has been working to improve its governance, and the 2017 election of a new president has helped regain confidence in Angola's overall outlook. As the sub-Saharan region’s second largest oil exporter, Angola was hard hit by the decline in oil prices that started in mid-2014, the pain of which is still being felt. With stringent attention to needed reforms, the economy could grow modestly in 2018.

Policies in the run-up to the August 2017 elections—fiscal expansion and a pegged exchange rate—led to a further erosion of fiscal and external buffers. The overall fiscal deficit worsened to 6 percent of GDP and public debt, including that of the state-owned oil company Sonangol, reached 64 percent of GDP in 2017. Gross international reserves declined to $17¾ billion—equivalent to 6 months of imports—while the spread between the parallel and official exchange rate was 150 percent in 2017.

The government launched the MSP in early January 2018. The plan envisages upfront fiscal consolidation, greater exchange rate flexibility, reducing the public debt-to-GDP ratio to 60 percent over the medium term, improving the profile of debt through a liability management operation, settling domestic payments arrears, and ensuring effective implementation of anti-money laundering legislation.

The National Assembly approved a prudent budget for 2018 that targets a 2 percent of GDP improvement in the non-oil primary fiscal balance. In January, the central bank exited from the peg to the U.S. dollar and has increasingly sold more foreign exchange in regular auctions as opposed to direct sales. The central bank is also revamping its monetary policy framework to include base money targeting.

The new government is making concerted efforts to improve the business environment.

The National Assembly recently approved a Law on Competition that introduces a framework to support competition in domestic markets and address monopolistic practices in key sectors, such as telecommunications and cement production. A Private Investment Law was also recently approved by the National Assembly that removes entry barriers to foreign direct investment. The government has also launched a program for diversifying exports and substituting imports.

Angola’s social gaps are large and widespread, including higher poverty incidence than predicted by income levels, and higher mortality rates than regional peers. Public spending is insufficient in critical areas like education. A well-designed conditional cash transfer program could help alleviate poverty and other social problems.