The European Central Bank, Frankfurt. Further reforms are needed to deliver a genuinely single and integrated capital market, say IMF economists (photo: Alex Domanski/Newscom)

The Euro Area Financial System: On-going Transformation

July 19, 2018

The euro area financial system—and especially the banking sector—has been transformed over the last five years. It’s now safer and better supervised than ever before. But much work remains to build an efficient, truly integrated financial system with banks that are sufficiently resilient to respond to new challenges.

Related Links

The global financial crisis and subsequent crisis in the euro area spurred authorities to embark on a bold project to create a banking union. Banks across the area would compete and provide services on a level playing field.

The aim was not only to make the best use of resources, but also to sever the “doom loop” between the state of the financial system and government finances.

The recently completed Financial Sector Assessment Program (FSAP) for the euro area takes an in-depth look at how far that project has progressed, and where further progress is most urgently needed.

The same high standard for banks

There is now a common framework to oversee the banking sector. The new “Single Supervisory Mechanism” (SSM) is designed to ensure that banks across the euro area are held to the same high standards. Under the SSM, euro area and national supervisors work together to identify concerns early on and deal with them before they become acute.

Policies are now also much more geared towards addressing macro-prudential risks—for example, when the price of housing in a region rises to unsustainable levels.

With thousands of banks in the euro area, occasional problems are inevitable, but the system for dealing with problem banks has been revamped. The “Single Resolution Mechanism” provides a range of instruments, procedures and facilities to handle such eventualities with minimal collateral damage to the rest of the economy or support from the taxpayer. This mechanism is not just a legal construct, but is embedded, for example, in detailed contingency planning and the accumulation of needed financial buffers.

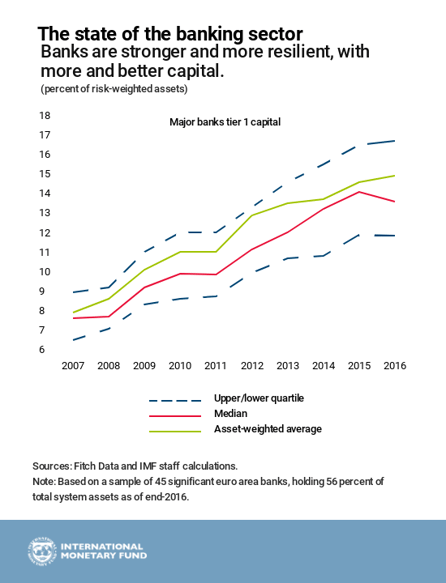

Stronger and more resilient banks

The banks themselves are, in many ways, stronger and more resilient, with more and better capital and more stable funding. Some banks are especially vulnerable to credit risks and others more to market risks or funding risks, but the picture is diverse.

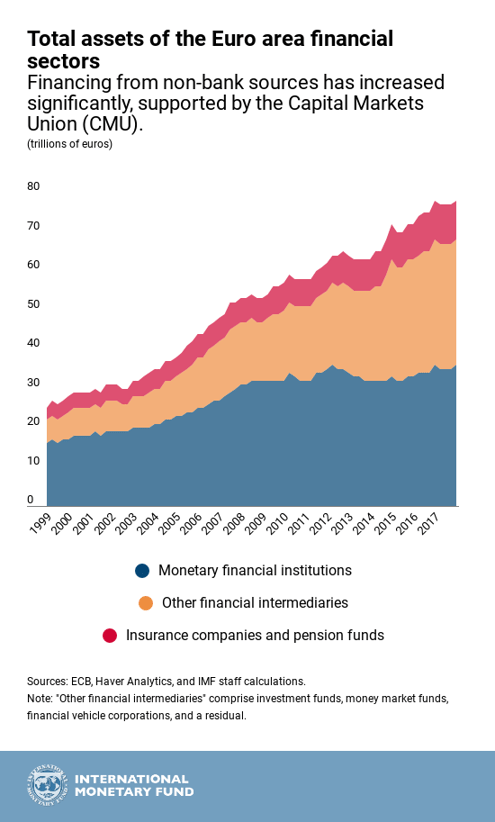

Financing from non-bank sources such as investment funds has increased significantly, supported by the Capital Markets Union (CMU) project, which aims to create a fully integrated capital market. Included are measures to help small firms raise financing across borders.

Remaining fissures along national lines

Yet important weaknesses remain, and financial markets are still fissured along national borders. The authorities and financial institutions need to make use of the current, relatively favorable circumstances to address these issues.

Many banks suffer from chronic low profitability even under present buoyant conditions. This inevitably reduces their resilience. Very often the low returns are due to stockpiles of nonperforming loans, but in other cases high operating costs seem to be responsible. For now, liquidity is plentiful and funding is cheap, but some banks may face challenges when monetary policy begins to normalize.

In some policy areas the SSM has to cope with a patchwork of national laws that create gaps and inconsistencies and work against the level playing field. A particular concern is the treatment of nonperforming loans, where a focused supervisory effort is beginning to pay off.

But to advance further, it would help to require banks to write down nonperforming loans in a time-bound way, improve the consistency of legal frameworks (for example, regarding credit rights) across countries, and sharpen valuation rules.

More progress in the practice of proactively addressing weak banks and in streamlining the legal and regulatory framework for resolution is needed to bolster the credibility of the new system. National frameworks vary widely, and incentives remain to “work around” approaches that may minimize the overall cost but also involve bailing in certain creditors.

Moreover, full credibility requires the further building up of buffers (notably “bail-in-able” liabilities that can absorb some losses; resources for funding in resolutions; and the European Deposit Insurance Scheme), and enough flexibility that contagion can be contained in a truly systemic event.

Further reforms are needed to deliver a genuinely single and integrated capital market. Greater harmonization of national insolvency regimes and securities regulations must be on the agenda. And the challenge is not just to create better instruments, but also to encourage the emergence of a large investor base interested in innovative and cross-border products.