Commercial container ship reaching the port of Walvis Bay, Namibia. Lower commodity prices and other factors could lower growth in sub-Saharan Africa (iStock/dani3315)

Navigating Sub-Saharan Africa’s Recovery Amid Greater Uncertainty

April 12, 2019

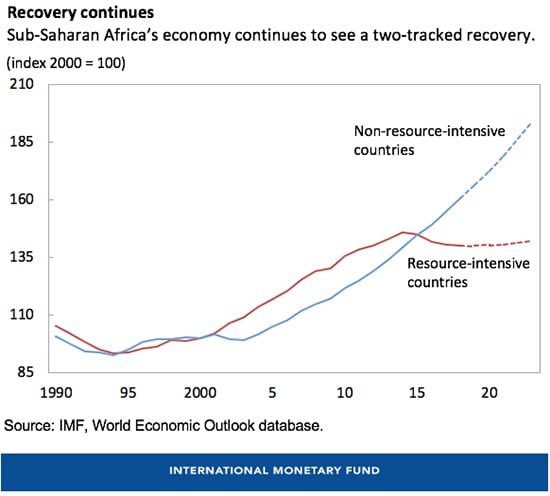

Sub-Saharan Africa’s economic recovery is set to continue, but along two tracks. Overall growth is set to pick up from 3 percent in 2018 to 3.5 percent in 2019, and stabilize at slightly below 4 percent over the medium term, the IMF said in its latest Regional Economic Outlook for sub-Saharan Africa.

Related Links

Declining budgets and a less supportive external environment complicate the challenge of finding ways to address human and physical capital investment needs, and create enough jobs to absorb the 20 million new entrants to labor markets each year. “Central to resolving this challenge is building up sufficient resources, enhancing resilience to shocks, and fostering an environment conducive to sustained, high, and inclusive growth,” said Abebe Aemro Selassie of the IMF’s African Department.

Here are six charts that tell the story.

1. Economic recovery is set to continue, but duality persists

Some 21 countries are expected to sustain growth at 5 percent or more in 2019. The remaining countries, mostly other resource-dependent economies, including the largest (Nigeria and South Africa) are set to face sluggish growth in the near-term.

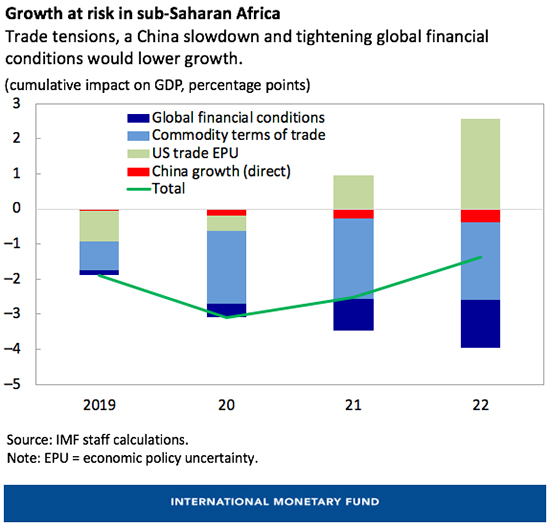

2. A deterioration in external conditions could slow growth in sub-Saharan Africa

Heightened trade tensions along with increased trade policy uncertainty in the United States, slower growth in China, lower commodity prices, and tighter global financial conditions could lower growth in sub-Saharan Africa by 2 percentage points this year. Commodity exporters would be the most affected, as will countries with stronger links to China and global markets, and/or those with large refinancing needs.

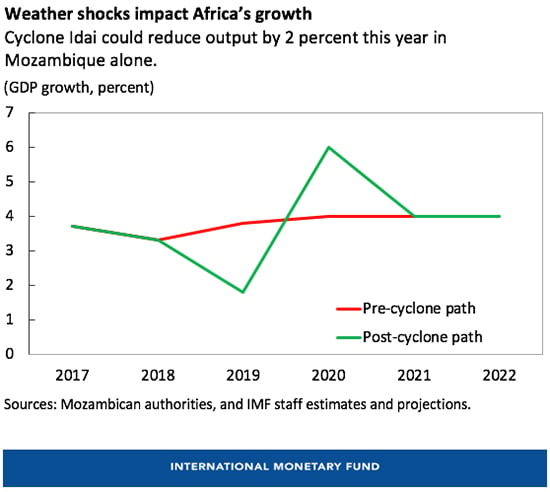

3. Weather shocks are creating further pressures on some countries in the region

Cyclone Idai, which made landfall in March 2019 in southeast Africa—affecting more than 2.6 million people and decimating physical infrastructure and farmland—illustrates the vulnerability of the region to weather-related disasters.

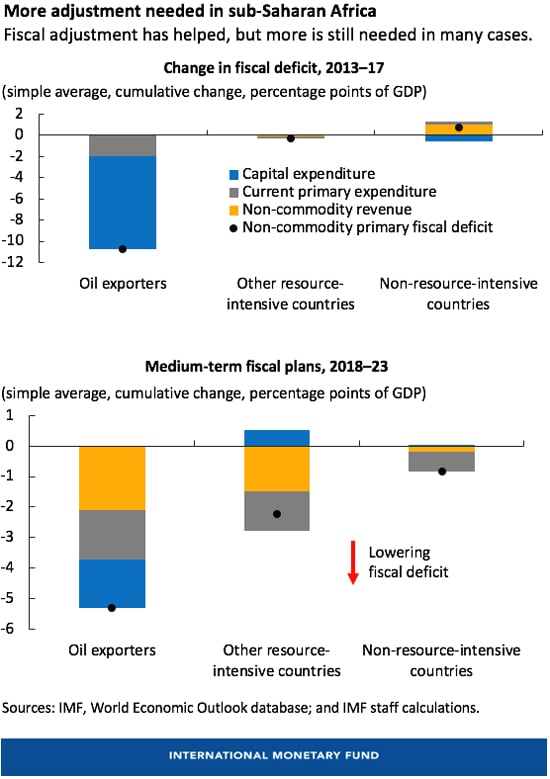

4. Fiscal adjustment has helped stabilize debt levels but more is still needed in many countries

The reduction in current debt ratios in some countries reflects the significant adjustment that has already taken place among oil exporting countries. But stabilizing or lowering debt ratios going forward requires more adjustment, consistent with existing fiscal consolidation plans.

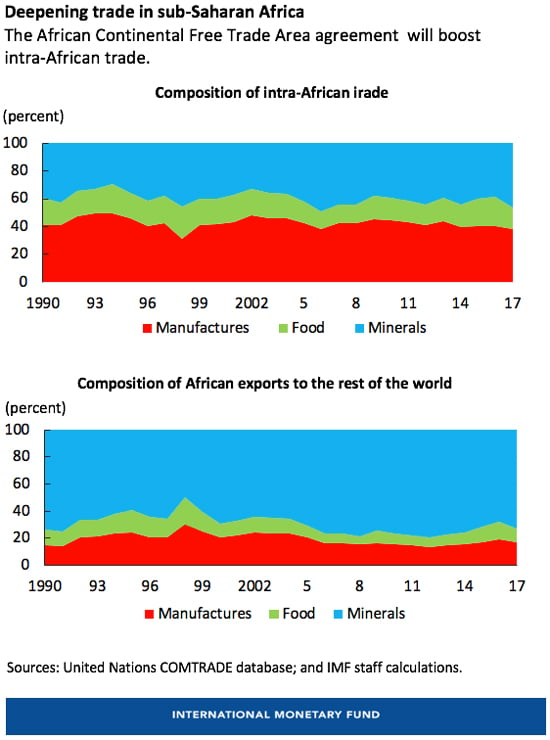

5. Boosting intra-regional trade is an important driver for growth

Once completed, the African Continental Free Trade Area agreement (AfCTA) will establish a market of 1.2 billion people with a combined GDP of 2.5 trillion dollars. This accord will significantly boost intra-African trade, particularly if non-tariff bottlenecks to trade are addressed.

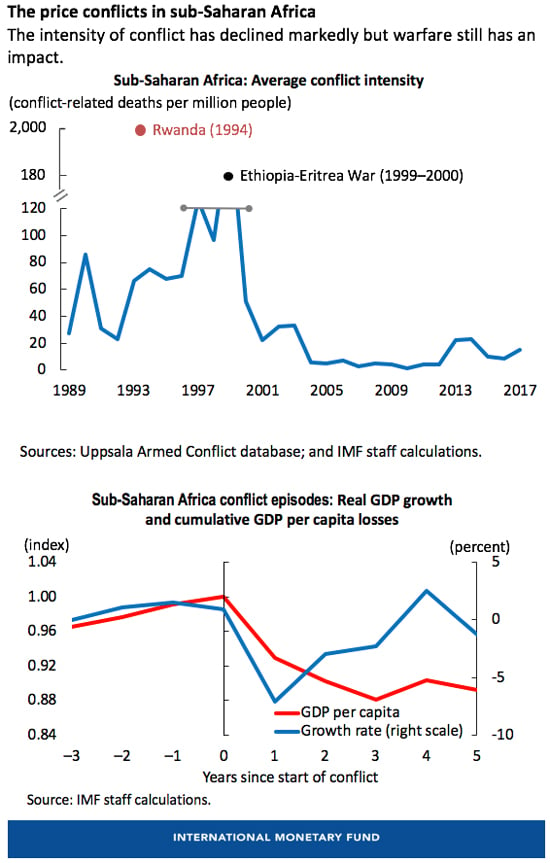

6. Security-related spending in fragile states and humanitarian assistance, including in host countries, pose further constraints

While the incidence and intensity of conflict in recent years is lower than in the 1990s, the region remains prone to conflicts. Conflicts in the region are associated with a large and persistent decline in GDP per person, and have significant spillover effects on nearby regions and countries.