Five Things to Know About the Economic Outlook in the Caucasus and Central Asia

April 29, 2019

While growth is stable, countries in the Caucasus and Central Asia (CCA) face an array of longstanding challenges that, if unaddressed, threaten to hold back the region from reaching its potential.

From lingering bank weaknesses to monetary policy frameworks in need of full modernization, countries must accelerate reform efforts if they are to raise living standards to those enjoyed elsewhere in the world. And amid slow global growth and policy uncertainty, this task is even more urgent.

Here are five key things to know from the latest IMF Regional Economic Outlook Update

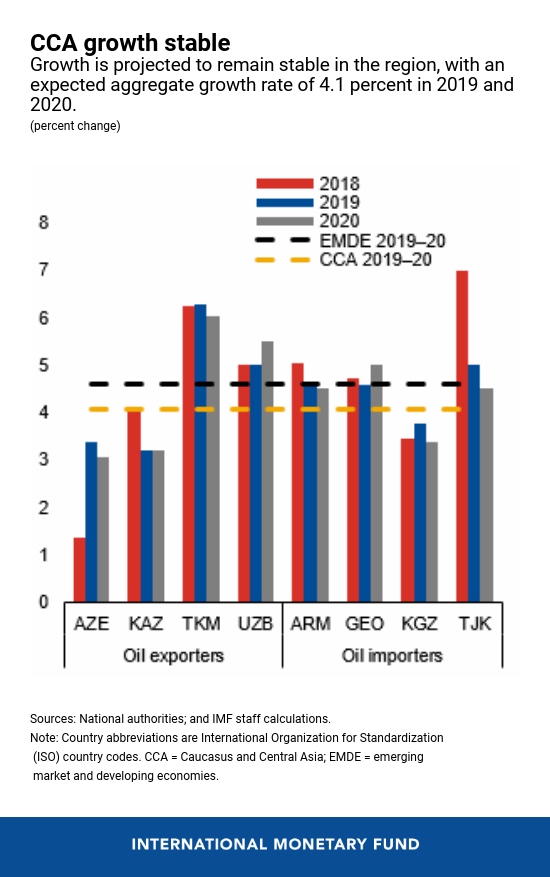

- The good news? Growth is stable, and inflation is low

In the years since the significant external shocks of 2014-16, growth in the region has stabilized, in part thanks to efforts to strengthen macroeconomic frameworks, such as tax code reform (implemented in Armenia, Georgia, and Uzbekistan) and the adoption of fiscal rules (implemented in Armenia, Azerbaijan, and Kyrgyz Republic). Strengthening of monetary policy frameworks and efforts to make exchange rates more flexible in some countries have also helped manage external pressures and contain inflation. Overall, growth in the region is projected at 4.1 percent in 2019 and 2020, which is in line with the 4.2 percent growth seen in 2018.

- Yet, growth remains too low, which is a drag on living standards

Although growth is stable, it is projected to average just 4.2 percent over 2020-23. This is less than half the recorded rate during the 2000s, and too low to raise the standards of living to those of comparable economies. Given demographic trends, it will take on average 18 years for countries in the region to either graduate from low-income status or reach the current per capital income levels of European emerging markets. - Persistent challenges remain—and banking weaknesses are near the top of the list

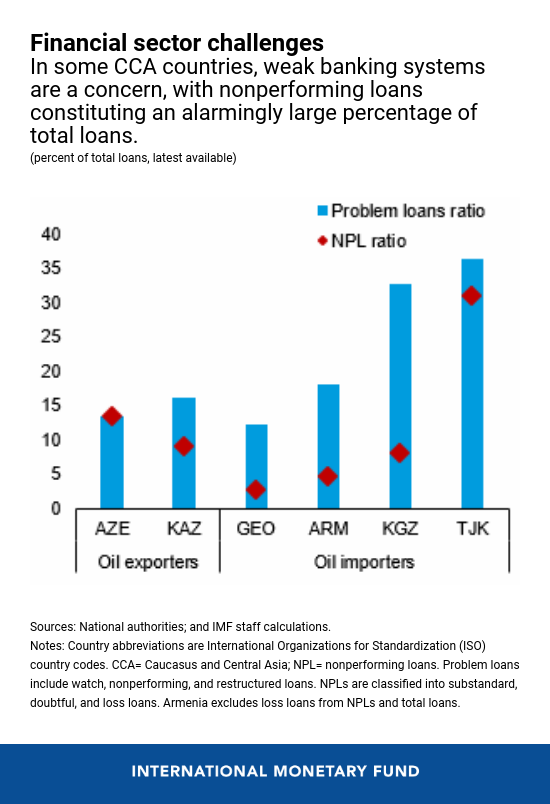

Countries in the Caucuses and Central Asia face legacy challenges from reforms that have long been left unresolved. For example, banking systems are burdened with problematic assets such as nonperforming loans (NPLs) and restructured loans. In some countries, the percentage of loans that have become troublesome has reached alarming levels. Tajikistan’s problem loans, for example, constitute more than 35 percent of its total loans, according to the latest data, with a significant majority of those being NPLs. As a result, pockets of bank stress persist, eroding lending capacity and inhibiting credit growth.

Adding to this challenge, monetary and exchange rate policy frameworks have not been fully upgraded, despite recent progress. As a result, exchange rates in the region remain largely managed, limiting countries’ ability to absorb external shocks. At the same time, a marked rise in public indebtedness in some countries strains fiscal buffers and space to support growth.

- The global economy makes the task even more challenging

While legacy challenges and reform efforts limit the region’s ability to realize its potential, risks to global growth and rising global uncertainties threaten the near-term.

Weaker growth outlooks in Russia and other key trading partners are already being felt through lower trade volumes and remittances. Meanwhile, a lack of diversity in exports makes countries particularly vulnerable to commodity price swings and a further slowdown in global growth. - What does this all mean? Reforms are needed now

Mounting external headwinds increase the urgency of boosting economic resilience by addressing legacy challenges and unfinished reform efforts.

Repairing the financial sector will be critical to support growth. This includes strengthening regulatory and supervisory frameworks. Stronger resolution and crisis management frameworks are also needed to facilitate orderly and faster resolution of nonviable banks.

Making economies more resilient also means fully modernizing monetary policy frameworks based on credible, rules-based regimes. This would keep inflation expectations well-anchored and foster full exchange rate flexibility, helping to support competitiveness and economies’ ability to absorb external shocks.

Many countries in the region should also rebuild fiscal buffers in growth-friendly ways by avoiding cuts to capital and social spending. This is particularly true in countries such as Azerbaijan and Tajikistan where public debt increased significantly because of past expansionary policies.

Additionally, private sector development and diversification remains paramount throughout the region. The state has long occupied an outsized role in CCA economies. Reducing its footprint and moving to more market-based approaches, including by improving the business environment and promoting good governance, would help spur medium-term growth across the region.