Shops are seen closed in Liberia’s capital Monrovia after the government instituted a strict lockdown in the early weeks of the pandemic. The country has managed to continue with economic reforms despite the crisis. (photo: Derick Snyder/Reuters/Newscom)

Four Things to Know on How Liberia Is Reforming Its Economy Amid COVID-19

December 21, 2020

On December 21, 2020, the International Monetary Fund provided additional financial assistance of $48.86 million to the Republic of Liberia under a program launched at the end of last year.

This decision follows debt relief and emergency assistance approved by the IMF earlier this year and is fully embedded in a reform agenda that the Liberian authorities are implementing to further stabilize the economy.

Here are four things to know:

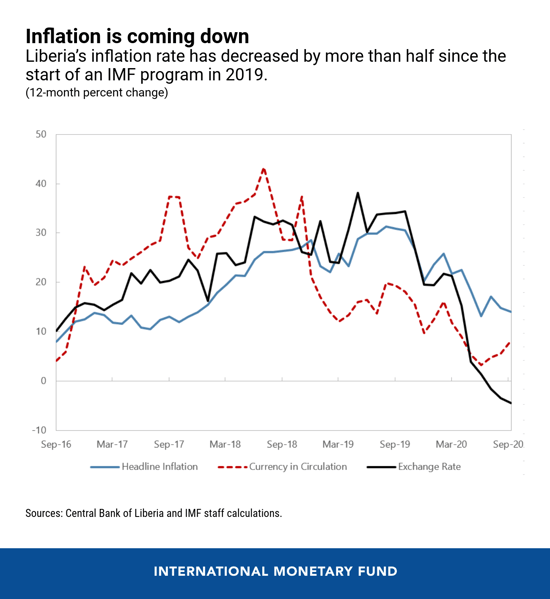

- The COVID-19 pandemic hit Liberia at a time of pre-existing fragility. The country held elections in 2017, leading to the first democratic transition of power between different political parties since 1944. Following the inauguration of the new administration in 2018, the United Nations Mission in Liberia, which had been in the country since the peace agreement of 2003, handed over its security responsibilities to the national police and military. These transitions coincided with the winding down of increased foreign aid after the 2014-16 Ebola outbreak. These events caused a sharp decline in net foreign exchange inflows to the country. This, in turn, heightened pressure on the Liberian dollar exchange rate and on inflation. To stabilize the economy, the authorities had to make difficult adjustments to an economy with less foreign exchange inflows, which created significant hardship for the Liberian people. The COVID-19 pandemic hit Liberia during this difficult adjustment phase.

- The government has worked hard to meet humanitarian needs during the COVID-19 pandemic. By taking lessons from the Ebola crisis, policy response was prompt. On March 21, the government mandated a general lockdown and enforced severe social distancing. But this policy response was costly in terms of economic slowdown, trade disruptions, and food insecurity. The IMF, along with other partners, provided emergency support during the height of the crisis. This most recent IMF assistance complements those actions as Liberia accompanies the difficult reform agenda the authorities have been pushing through amid the COVID-19 crisis.

- The government’s decisive actions and reform efforts have begun to bear fruit. At its peak in FY2018/19, the civil service wage bill accounted for 10 percent of GDP (or 70 percent of domestic revenue), which was crowding out the government’s fiscal space for much needed development, infrastructure, health, and education spending. The authorities took the difficult but necessary decision to cut the wage bill in all three branches of the government by 10 percent in the FY2019/20 budget, while still allowing the lowest-paid government employees to receive the minimum wage. The government also eliminated allowances that were not only costly but also adversely affected the morale of civil servants due to perceptions of unfairness. The action eliminated central bank financing of fiscal deficits. This eased inflation providing benefits to the poorest Liberians who mostly earn Liberian dollars in this dual currency economy.

- Reform efforts at the central bank have focused on rebuilding confidence in the banking sector. In October 2020, the National Legislature approved amendments to the Central Bank of Liberia (CBL) Act. With this amendment, the CBL now has more operational autonomy in enhancing the quality and quantity of Liberian banknotes. The CBL also has a formal mandate to ensure financial stability. With this new mandate, the CBL is committed to strengthening the financial supervisory and regulatory framework and, in turn, the banking sector that can support post-COVID recovery efforts.