The Saad Zaghloul local market in Cairo. Although the pandemic hit the economy hard, Egypt was one of the few emerging markets that maintained growth. (photo: IMF Photo/Roger Anis)

Egypt: Overcoming the COVID Shock and Maintaining Growth

July 14, 2021

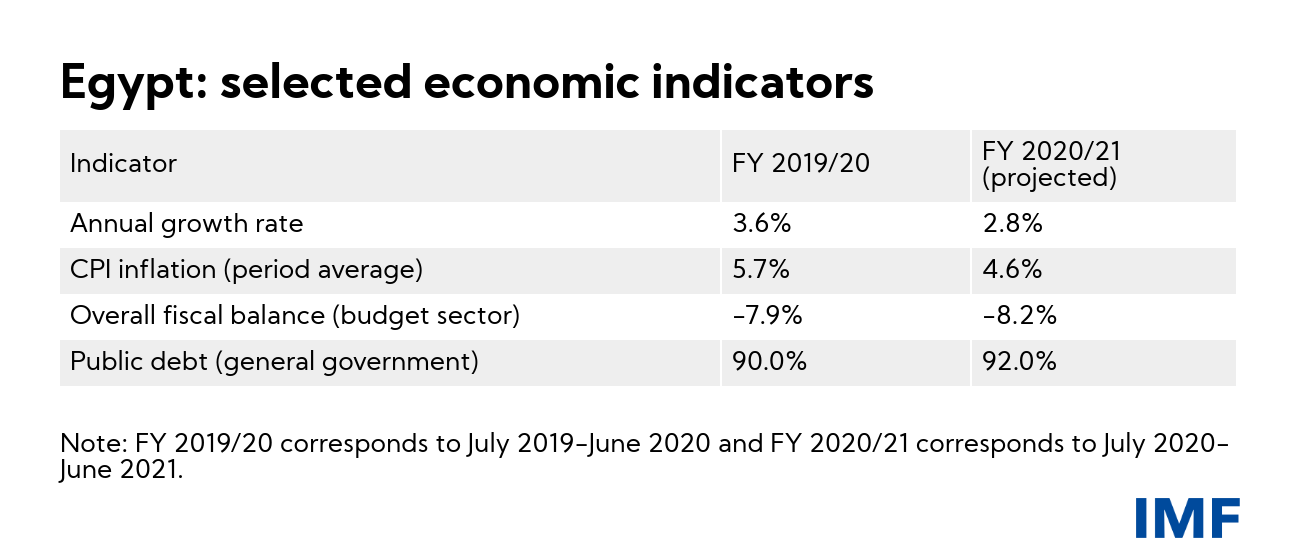

Egypt was one of the few emerging market countries that experienced a positive growth rate in 2020. As a result of the government’s swift and prudent policy response, coupled with IMF support, the Egyptian economy showed resilience in the face of the pandemic.

Related Links

IMF Country Focus spoke to the IMF team for Egypt about the government’s response to the pandemic, the IMF’s role in supporting Egypt, and the challenges and priorities moving forward.

How did the COVID-19 pandemic impact Egypt?

Suchanan Tambunlertchai: Like most emerging markets, the COVID-19 pandemic has been an enormous shock for the Egyptian economy. The fallout was immediately felt through a sudden stop in tourism—which, at the onset of the crisis, accounted for around 12 percent of GDP, 10 percent of employment, and 4 percent of GDP in foreign currency earnings. Precautionary measures to contain the spread of the virus, including partial lockdowns and restrictions on capacity in public spaces, resulted in a temporary decline in domestic activity, while the government’s budget was stretched as the economic slowdown reduced tax revenues. Egypt also experienced significant capital outflows of more than $15 billion during March-April 2020 as investors pulled out of emerging markets in a flight to safety. Nonetheless, Egypt was one of the few emerging market countries that experienced a positive growth rate in 2020, thanks to the government’s timely response, the short period of lockdown and Egypt’s relatively diversified economy.

What measures did the government enact to tackle the crisis?

Deeksha Kale: Egypt entered the COVID-19 crisis with sizable buffers, thanks to reforms implemented since 2016 to restore macroeconomic imbalances, including under the 2016-19 Extended Fund Facility (EFF). Those included floating the exchange rate to eliminate currency overvaluation, fiscal consolidation to reduce public debt, energy subsidy reform to address a key fiscal risk and create space for social spending, and structural reforms to strengthen the business climate, attract investment, and increase employment opportunities, in particular among youth and women. As a result, the government was able to quickly respond with a comprehensive support package while preserving economic stability. For example, fiscal support included relief to businesses and workers in the hardest-hit sectors such as tourism and manufacturing, the postponement of tax payments and the expansion of cash transfer programs to poor households and irregular workers.

In addition, the Central Bank of Egypt reduced policy interest rates by 400 basis points during 2020—with the overnight deposit rate cut from 12.25 percent to 8.25 percent—to help support economic activity and alleviate pressures in domestic financial markets. It also introduced several initiatives to reduce pressure on borrowers and ensure liquidity for the most impacted sectors, including increased access to credit at preferential interest rates and a six-month debt moratorium on existing credit. These exceptional financial sector measures were important to ensure smooth credit flow in the economy in the wake of the COVID-19 crisis.

What role did the IMF play in supporting Egypt’s response and recovery?

Matthew Gaertner: The IMF provided about $8 billion in financial support through a two-pronged plan to help Egypt address the financing needs that resulted from the pandemic. The Rapid Financing Instrument provided $2.8 billion in emergency financial assistance in May 2020 to ensure that the government had enough foreign currency to fund essential imports and other needs. The Stand-by Arrangement (SBA), approved in June 2020, provided the government access to a total of about US$5.4 billion over the subsequent 12 months.

The SBA helped the authorities maintain economic stability, rebuild international reserves to restore buffers drawn down in response to the crisis, and progress on key structural reforms, including with measures to strengthen public finances, further fiscal transparency and governance, and advance laws to improve the business climate, to position Egypt for a strong and inclusive recovery. Economic policies under the program struck a balance between supporting the economy to help shield it from the COVID-19 shock and ensuring debt remains sustainable to maintain investor confidence. As a consequence of the government’s timely and prudent policy response, coupled with IMF support, the economy has exhibited resilience, with growth expected at 2.8 percent for FY 2020/21.

What are the top challenges and priorities for Egypt moving forward?

Celine Allard: Over the past 12 months, the authorities’ commitment to prudent policies and their strong performance under the IMF program have helped mitigate the health and social impact of the pandemic while safeguarding economic stability, debt sustainability, and investor confidence. Growth is expected to rebound strongly in FY2021/22 to 5.2 percent, but the outlook is still clouded by uncertainty related to the pandemic, including regarding the full recovery of tourism.

In addition, Egypt’s high public debt and large gross financing needs—the amount of money the government needs to issue every year, both to renew loans that are maturing and to finance new debt—leave it vulnerable to external shocks, such as higher costs of borrowing at the global level as developed economies gradually withdraw their economic stimulus.

Going forward, continuing to preserve economic stability and reduce public debt will be important. With the immediate impact of the crisis subsiding, it will also be essential to focus on structural reforms to encourage private-sector led growth, such as policies to increase revenue for financing critical public goods including health, education and social safety nets, enhance governance and transparency, and further develop financial markets.

Reducing the role of the state in the economy, ensuring a level-playing field for all firms, improving the business environment, and increasing Egypt’s integration into global trade by reducing trade barriers and ensuring predictability of customs procedures will also be critical to unleash Egypt’s enormous growth potential, reduce poverty and improve inclusiveness. The IMF will continue to support Egypt’s reform efforts as specific policy measures to support these objectives are defined and implemented.