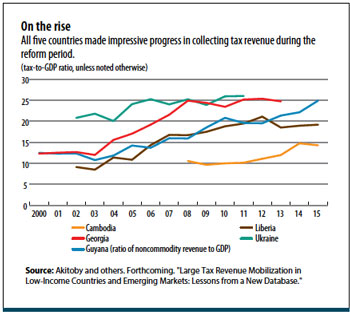

Lessons for tax reform

What does Georgia’s experience teach us about how best to increase tax revenue? While there is no one-size-fits-all solution, there are a few lessons that can be drawn from Georgia’s case as well as the experiences of the other four countries.

Have a clear mandate. Governments with a clear mandate to reform the tax system often succeed. Georgia’s comprehensive tax reform was feasible only after the country had reached a high degree of dysfunction, triggering a revolution. Similarly, in Ukraine, the 2004 Orange Revolution was a catalyst for tax reform. And in 2003, Liberia initiated reform after the civil war had ended.

Secure high-level political commitment and buy-in from all stakeholders. While a clear mandate is necessary, it is not sufficient. Many newly

elected governments do have such a mandate, but not all of them reform. Therefore, political commitment at the highest level and broad buy-in are needed. Social dialogue enhances the likelihood of reforms being implemented and sustained. Effective communication with stakeholders that emphasizes the intended benefits of reforms can help overcome resistance of vested interests. And compensating the losers has proved effective in winning public support for tax reform initiatives.

Simplify the tax system and curb exemptions. A simpler tax system with a limited number of rates is critical to fostering taxpayer compliance, as seen in the Georgia example. Notably, in fragile states, focus first on simplifying taxes, procedures, and structures. Simplicity of the tax system and legislation is the guiding principle for fragile states. This makes tax administration less challenging in weak states that lack such basic institutions as security and a well-functioning judicial system.

Liberia is a case in point. Following its emergence from civil war, Liberia introduced taxes on turnover or import values, such as the goods and services tax, excises, and customs tariffs, underpinned by simple tax legislation.

Curbing exemptions can also reduce the tax system’s complexity while boosting revenue by broadening the tax base. Many countries incur a sizable loss of revenue through ill-designed exemptions, such as costly tax holidays and other incentives that fail to attract investment. And discretionary granting of exemptions provides opportunities for corruption.

Reducing exemptions figured prominently in nearly all five countries. Guyana, for example, implemented a comprehensive exemption reform with main elements that included eliminating the power of the finance minister to grant discretionary exemptions, publishing exemptions annually, and limiting income tax holidays to every 5 or 10 years, depending on the sector.

Reform indirect taxes on goods and services. The VAT has proved to be an efficient and strong revenue booster: countries that impose this tax tend to raise more revenue than those that don’t (Keen and Lockwood 2010). In addition to reducing the rate, Georgia streamlined its VAT refund mechanism, allowing revenue from this source to rise from 8.5 percent of GDP in 2005 to about 11.5 percent in 2009.

Guyana successfully introduced a VAT on January 1, 2007, despite significant challenges in the preparatory work, including setting up the new VAT department with fully trained staff, putting in place the supporting IT system and procedures, and training potential registrants and practitioners. The VAT was broad-based, with a single rate of 16 percent and a limited number of exemptions for financial, medical, and educational services. As part of its reform, Ukraine also curbed VAT exemptions and revised the regime for agriculture by reducing the rate and eliminating refunds.

Increases in excise and sales taxes are the simplest measures because they can raise revenue fairly quickly without fundamental changes to the tax system. For example, Guyana in 2015 took advantage of the decline in the international price of oil to raise fuel excise taxes. This step buoyed revenue during the country’s economic slowdown. Similarly, Liberia broadened the scope of its goods and services tax while raising excise taxes on alcoholic beverages and cigarettes.

Introduce comprehensive tax administration reforms. Successful revenue mobilization cases tend to take a more holistic approach to modernizing tax institutions. In all five case studies, revenue administration reforms figured prominently and covered a broad spectrum of legal, technical, and administrative measures, such as

Management, governance, and human resources: Four of the five countries implemented some management and governance changes. Georgia gradually recruited new tax and customs officers and phased out the old ones as part of its anti-corruption reform.

Establishment of large taxpayer offices: A large taxpayer office allows a country to focus tax compliance efforts on the biggest taxpayers, as Cambodia has done. These offices also support good tax administration; they often pilot new tax and customs procedures before their rollout to the broader population.

Smart use of information management systems: Successful revenue mobilization hinges on managing information and leveraging the power of big data to improve compliance and fight corruption. Most of the countries studied have taken advantage of IT systems to leapfrog their revenue mobilization reforms. Georgia has automated most processes, including e-filing. It has also instituted a system for information sharing among tax authorities, taxpayers, and banks, as well as a one-stop Internet portal. Cambodia, Guyana, and Liberia have likewise computerized the administration of their taxes and customs.

More modern registration, filing, and management of payment obligations: All five countries have sought to establish or modernize basic rules and processes in these key compliance areas. For instance, Guyana implemented a unique system of taxpayer identification numbers and streamlined its process. It also introduced income tax withholding, a measure critical to fostering compliance.

Enhanced audit and verification program: A risk-based audit, which links the likelihood and nature of an audit to the taxpayer’s inherent risks, is the most effective type in terms of encouraging compliance. All five countries have made this a key part of their revenue mobilization strategy. Notably, Cambodia conducted risk-based audits of taxpayers at customs and of the 150 largest taxpayers and hired some 200 new auditors. Ukraine implemented a targeted audit program, improved the internal control of tax administration, fought fraudulent VAT claims, and developed an anti-smuggling program at the customs office.