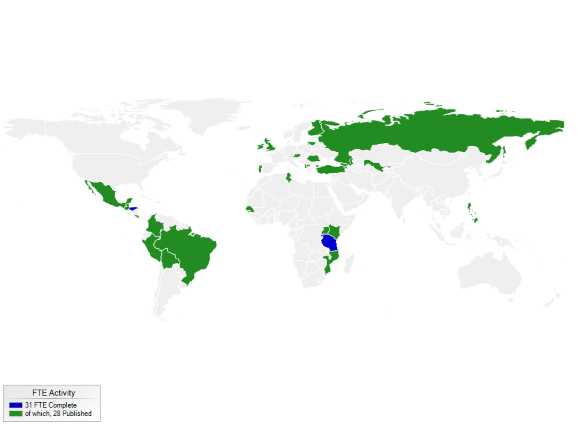

Published Fiscal Transparency Evaluations (FTEs): Albania; Armenia; Austria; Benin (also in French) Bolivia; Brazil; Chile; Colombia; Costa Rica; Estonia; Finland; Georgia; Georgia (update); Guatemala; Honduras (also in Spanish); Ireland; Jordan; Kenya (original); Kenya (update); Lithuania; Maldives; Macedonia; Malta; Mexico; Mozambique; Peru; Portugal; Philippines; Romania; Russia; Russia (update); Senegal; Slovak Republic; South Africa; Tunisia; Turkey; Uganda; United Kingdom; Uzbekistan; Uzbekistan (updated)

Fiscal transparency – the comprehensiveness, clarity, reliability, timeliness, and relevance of public reporting on the past, present, and future state of public finances – is critical for effective fiscal management and accountability. It helps ensure that governments have an accurate picture of their finances when making economic decisions, including of the costs and benefits of policy changes and potential risks to public finances. It also provides legislatures, markets, and citizens with the information they need to hold governments accountable. Greater fiscal transparency can also help strengthen the credibility of a country’s fiscal plans and can help underpin market confidence and market perceptions of fiscal solvency.

The Fiscal Transparency Code and Evaluation are the key elements of the IMF’s ongoing efforts to strengthen fiscal surveillance, policymaking, and accountability among its member countries.

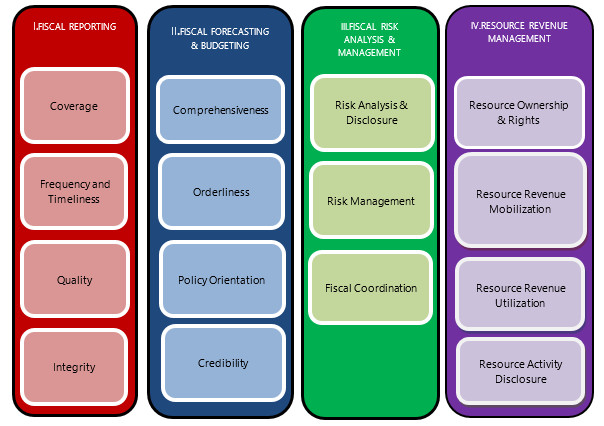

Fiscal Transparency Evaluations (FTEs) are the IMF’s fiscal transparency diagnostic. FTEs provide countries with:

FTEs are carried out at the request of countries. They also support capacity building, including the prioritization and delivery of IMF technical assistance. FTEs have been conducted in over 30 countries to date, across a wide range of regions and income levels and additional FTEs are planned. The IMF’s Fiscal Affairs Department would welcome interest from countries interested in undertaking an FTE.

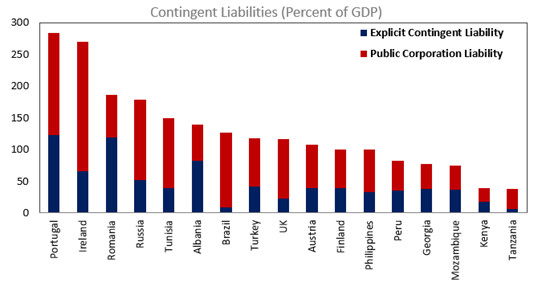

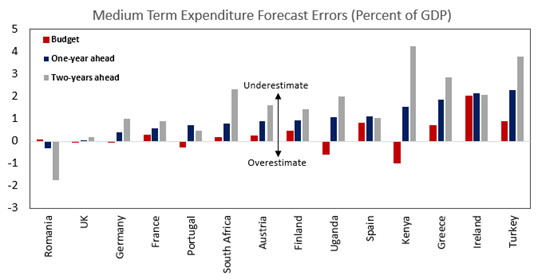

The results show there is scope for countries to improve their transparency practices, in particular by expanding the coverage of fiscal reports, strengthening the credibility of budget frameworks, and improving the disclosure and management of fiscal risks.