Macroprudential Policy and Financial Vulnerabilities

September 22, 2017

Loading component...

IMF Communications Department

MEDIA RELATIONS

PRESS OFFICER: Silvia Zucchini

Phone: +1 202 623-7100Email: MEDIA@IMF.org

By Tobias Adrian, IMF Financial Counsellor

European Systemic Risk Board Annual Conference, European Central Bank, Frankfurt

As Prepared for Delivery

Thank you, and good afternoon. I am extremely pleased and honored to participate in the second ESRB annual conference here in Frankfurt.

Today, I would like to speak about macroprudential policy and financial vulnerabilities.

Let me start my remarks by revisiting a basic question: what is financial stability?

A first, and well accepted answer equates financial stability with the absence of systemic risk, that is the risk of a disruption to the capacity of the financial system to perform its functions, and especially to its capacity to provide credit to the economy.

An alternative answer that is recently gaining currency equates financial stability with the absence of sharp movements in financial conditions. Sharp movements in financial conditions that arise from large increases in the price of risk and negative externalities created by financial vulnerabilities can give rise to financial stability concerns.

In this speech, I will propose that policy makers might care about sharp movements in financial conditions, even if those do not necessarily lead to systemic disruptions of the financial sector’s intermediation capacity.

Goals of Cyclical Macroprudential Policy

How does this idea fit with the accepted understanding of the goals of macroprudential policy? As is well known, macroprudential policy has two dimensions. Structural macroprudential policy aims to mitigate externalities from the failure of individual systemic institutions and the systemic risks arising from their interconnectedness within the financial system, including its ‘plumbing.’

Cyclical macroprudential policy is often described as mitigating systemic risk in the time dimension. However, in practice, I will argue that this amounts to aiming at mitigating the risk of sharp reversals in financial conditions. The reduction of systemic risk – the tail of the distribution of changes in financial conditions –is therefore an important outcome of these policies.

What do I mean by financial conditions? Financial conditions refer to the ease of financing across funding markets, including credit, equity, money, and foreign currency markets, reflecting the pricing of risk and underwriting standards in different asset markets.

I distinguish financial vulnerabilities from financial conditions. There are many dimensions to financial vulnerabilities. For example, one could distinguish the amount of leverage and maturity transformation that are prevailing in different sectors of the economy, such as the household sector, the nonfinancial corporate sector, the banking sector, or the shadow banking system. Financial vulnerabilities can lead to fire sales or investor runs, creating negative externalities.

Of course, financial conditions and financial vulnerabilities interact. Easy financial conditions sow the seeds for the buildup of financial vulnerabilities. When financial vulnerability is high and financial conditions are loose, risks to financial stability going forward are likely higher than when financial vulnerability is high and financial conditions are broadly neutral.

Both financial vulnerabilities and financial conditions tend to exhibit cycles. Cycles in the pricing of risk tend to be somewhat shorter than cycles in leverage or maturity transformation. In general, periods of easy financial conditions tend to be followed by a tightening, though the timing and durability of the tightening tend to vary from cycle to cycle.

In some cases, easy financial conditions are associated with the buildup of vulnerabilities that reflect unchecked underlying externalities and spread across institutions and markets via fire sales, runs, or disorderly deleveraging. In those cases, easy financial conditions could be followed by a sharper and even more prolonged tightening with larger adverse impacts on economic growth. The greater the imbalances that have built up during times of easy financial conditions, the larger the risks of a sharp adjustment in financial conditions, even if it does not result in a systemic disruption of financial intermediation.

As I will explain in more detail shortly, the key frictions that can lead to excessive variation in financial conditions can be fueled by certain market failures, namely:

extrapolative expectations,

competition leading to excessive risk taking across institutions,

the leverage cycle due to risk management practices.

In the face of these frictions, the tasks of cyclical macroprudential policies are two-fold:

To lean against the buildup of financial vulnerabilities with the goal of reducing macro-financial amplification mechanisms.

To build temporary buffers when financial conditions are overly easy and financial vulnerabilities are growing.

The rationale for the first of these objectives is to counteract temporary distortions in risk taking, i.e. to counteract the tendency of financial intermediaries to “dance until the music stops.” Aiming for a temporary increase in resilience makes sense because increasing resilience amounts to taking out insurance; and taking out insurance when financial conditions are easy is cheap.

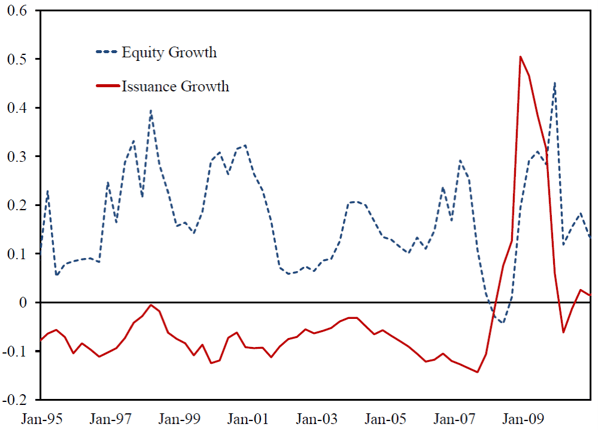

To illustrate, Figure 1 shows the net equity issuance in the run-up to the financial crisis, using the data of US trading institutions. Clearly, these institutions increased pay outs in the run-up to the crisis (as can be seen from the red line). Broker dealers only started to issue once their book equity (shown in the blue line) collapsed as the crisis hit. This illustrates nicely what it means to dance til the music stops.

Figure 1: Net Equity Issuance and Common Equity

Note: Security broker dealers from the U.S. flow of funds.

On net, firms issued equity when it was most expensive—in the midst of the crisis. It would have been cheaper to accumulate a larger equity cushion in the boom. But the three frictions that I alluded to earlier—extrapolative expectations, excessive risk taking, and the leverage cycle—all lead firms to keep paying out. Such behavior is more likely when banks are interconnected or highly leveraged ( Acharya, Le, and Shin 2016 ) .

Economic Frictions

I will argue that policymakers may care about sharp changes in financial conditions even if those changes do not necessarily lead to a crystallization of systemic risk within the financial system. It is sufficient for them to have measurable effects in amplifying economic volatility, because such amplification might well translate into adverse outcomes for GDP growth.

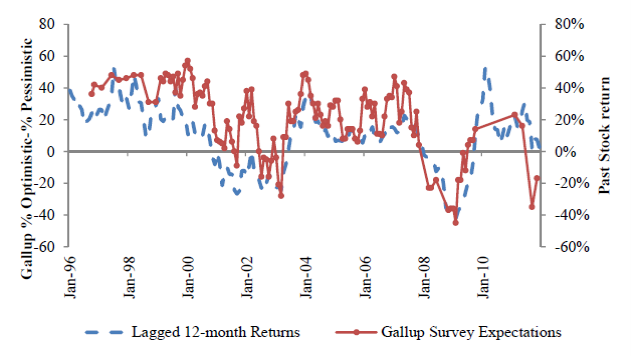

There are a number of economic channels that can lead to such amplification over time. From a cyclical macroprudential perspective, what matters is that the amplification mechanisms exhibit temporary time variation. The first amplification mechanism that I believe is important are extrapolative beliefs. The recent academic literature documents the pervasiveness of the phenomenon using a variety of equity, housing, and banking data. Analysts and CFOs extrapolate past returns to form expectations about future returns in equity markets ( Greenwood and Shleifer 2014 ). That means that they tend to expect the highest returns at the peak and the lowest returns at the depth of crisis (see Figure 2). That type of behavior is the opposite of what would be expected from rational economic theories, which predict low expected returns in booms, and high expected returns in busts. Of course, the presence of a significant amount of extrapolative economic actors means that asset pricing cycles tend to be exacerbated.

Figure 2: The Role of Past Stock Market Returns in Explaining Survey Expectations

Note: The dashed line denotes the 12-month rolling nominal return on the CRSP VW stock index. The solid line marked with circles denotes expectations from the Gallup survey (% optimistic - %pessimistic). Source: Greenwood-Shleifer (2014).

In a similar vein, housing market professionals including real estate brokers, real estate lawyers, and securitization experts continued to accumulate housing positions well into 2007 ( Cheng, Raina, and Xiong 2014 ). There is no evidence that they expected the housing cycle to turn. More generally, based on data since 1920 across 20 economies, bank credit expansions strongly suggest neglected crash risk: banks tend to lend well into the boom, even though such behavior strongly forecasts negative bank returns in the subsequent correction ( Baron and Xiong 2017 ). In sum, there is solid evidence that key economic actors tend to underestimate the risk of adjustments to the pricing of risk, and consequently take on excessive risk in the boom, leading to the buildup of financial vulnerabilities when financial conditions are easy.

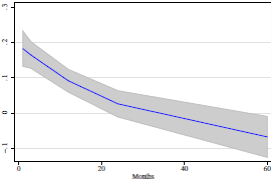

A second key economic friction consists of the competitive behavior across financial institutions. High returns on equity (ROE) across firms forecasts high equity market returns (see Figure 3 from Adrian, Friedman, and Muir 2015 ). Yet in the longer run, and in the aggregate, high financial sector ROE forecasts equity market returns negatively. Clearly, firms have incentives to take risks to increase ROE, as that gives them an advantage relative to their competitors. However, in the aggregate, that leads to an erosion of profitability, and hence aggregate ROE is forecast negatively. Worse, incentives of individual firms to take risk in order to maximize ROE might well lead to excessive risk taking. Coupled with a tendency for extrapolative beliefs, the consequence is behavior that looks shortsighted. Again, everyone dances until the music stops.

Figure 3: Forecasting equity returns with ROE across institutions

Note: This Figure plots the panel regression forecasting slopes for cumulative, overlapping, annualized returns at 1-60 month horizons from regressing future equity returns on ROE. Source: Adrian-Muir-Stackman (2016).

The combination of extrapolative beliefs and competition across institutions can act as an amplification mechanism for the leverage cycle. Theories of the leverage cycle tend to feature investors with heterogenous beliefs where optimists are pricing assets in the boom, while pessimists are the marginal investors in busts ( Geanakoplos 2010 ). As a result, leverage cycles lead to distorted pricing of risk, and consequently distorted real and financial allocations. In my own work, I have presented a leverage cycle that is associated with agency frictions among investors and managers of financial institutions (Adrian and Shin 2010 , 2014 ). The temptation of managers to invest in risky assets associated with their limited liability leads investors to impose a leverage constraint that depends on measured risk. In the boom, when those measured risks are low, institutions are able to take on leverage, which is excessive from a macroeconomic perspective. Hence prudent microeconomic risk management can be associated with an amplification of the leverage cycle in the aggregate. Of course, the mechanisms of the leverage cycle would be reinforced by the economic mechanisms described earlier, i.e. the tendency of market participants to extrapolate, and the urge of financial institutions to compete on ROE without taking aggregate consequences into account.

Financial Conditions, Financial Vulnerability, and Risks to GDP Growth

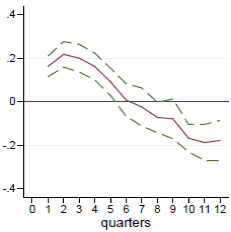

All three economic mechanisms provide incentives for the buildup of vulnerabilities during times of easy financial conditions. And these vulnerabilities tend to be associated with sharper declines in output once a bad shock hits. To illustrate this, Figure 4 shows the dependence of GDP volatility on financial conditions. At short horizons, up to 5 quarters, easier financial conditions forecast lower GDP volatility. But at longer horizons, there is a reversal, and easier financial conditions signal higher GDP volatility, as a shock is amplified by larger vulnerabilities (note that the financial conditions index used here is higher when conditions are worse, like a credit spread, or market volatility). This type of phenomenon is sometimes referred to as “volatility paradox” (e.g., Brunnermeier and Sannikov , 2014 ).

Figure 4: GDP Volatility and Financial Conditions

Note: The Figure plots the response of GDP volatility to financial conditions

Effects on output occur through a number of mechanisms. Those are at work both when the upswing in leverage results in a full-blown crisis, and when it does not. When vulnerabilities are high, an adverse shock will tend to increase borrower defaults, and this increase will be sharper when financial vulnerability is associated with a weakening of lending standards. When intermediaries sustain losses, they become constrained and reduce the supply of credit to the economy.

Importantly, using bank-level evidence, such credit crunch effects have been found to be at work both in crisis times and outside of full-blown banking crisis ( Nier and Zicchino , 2008 ). In other words, credit crunch effects are pervasive and can contribute to a deepening of recessions even outside of crises episodes, as documented in studies using aggregate data ( Claessens, Kose and Terrones , 2009 ). The collapse in the supply of credit that is associated with a full-blown crisis is therefore best understood to be just an extreme case of a more common phenomena associated with the movements in financial conditions.

Tightening financial conditions can also lead to a reassessment of debt levels, potentially forcing a deleveraging on the part of borrowers, particularly the household and corporate sectors. This results in a drop in investment and consumption ( Guerrieri and Lorenzoni, 2017 , Eggertsson and Krugman, 2012 ). This effect will be at work even when borrowers do not default on their debt (and therefore do not affect directly the health of the banking system), but adjust otherwise.

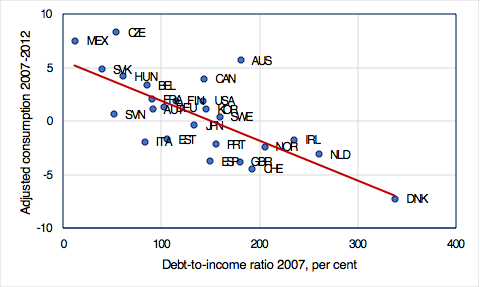

Using cross-county data for the Unites States, recent research (Mian and Sufi 2009 , 2014) shows that U.S. counties that experienced a larger increase in household leverage from 2002 to 2006 showed a sharper decline in durable goods consumption starting as early as the end of 2006. And this pattern also holds across countries (Figure 3). The drop in consumption was the larger, the higher household debt-to income ratios in 2007.

Figure 5: Relationship between debt-to-income ratio and

consumption growth between 2007 and 2012

Source: Riksbank’s Financial Stability Report, 2015

The available evidence shows that these mechanisms are not confined to episodes of full-blown financial crises. Even outside of such episodes, empirical research based on long runs of historical data has found that there is a close relationship between the build-up of credit during an expansion and the severity of the subsequent recession (see Jorda, Schularick, Taylor, 2013 ).

Hence vulnerabilities build up during times of easy financial conditions, and lead to amplification in downturns in reaction to adverse shocks. Even if adverse shocks do not cause systemic disruptions of financial intermediation, counteracting the frictions that lead to excess volatility can improve welfare as measured by downside risks to GDP growth. There is therefore a case for countercyclical macroprudential intervention aimed at taming these dynamics.

Of course, there are tradeoffs. Adjusting policy today might mitigate risks in the medium run, but that comes at the cost of distorted activity in the short run. Quantifying these types of tradeoffs is an important item on the macroprudential policy agenda, and a topic that is only now starting to be explored.

Monetary and Cyclical Macroprudential Policies

Now, one might ask: shouldn’t such countercyclical policies relative to financial conditions be undertaken by monetary policy? There is clearly a close connection to monetary policy, which acts by impacting financial conditions (always and everywhere). Monetary policy can also be steered deliberately to offset changes in financial conditions. Indeed, many have argued that monetary policy should take financial conditions into account even if central banks are targeting inflation. And in practice, monetary policy often offsets the easing or tightening of financial conditions.

The advantage of using monetary policy more systematically to steer financial conditions is that it can get into all of the ‘cracks’, while macroprudential policy can be arbitraged across jurisdictions, markets, or institutions. But there are also limitations to using monetary policy in this way.

Monetary policy cannot induce changes in resilience, unlike macroprudential policy. For instance, a tightening of the counter-cyclical capital buffer (CCyB) can bring about an increase in resilience. This can be very useful to protect against a future tightening of financial conditions, but is not easily achieved by a tightening of the monetary policy stance.

Monetary policy is not targeted enough to address differential financial conditions across sectors of the economy. For instance, a residential or commercial real estate boom may develop because of the behavior of lenders and borrowers in that segment, and occur at times when financial conditions are not unusually easy otherwise across the economy as a whole. Targeted macroprudential policy is then preferred.

Furthermore, monetary policy has price stability as primary mandate. It may not be able to respond enough to offset a build-up of risks given tradeoffs relative to its inflation objective. For instance, where the central bank is determined to stimulate, it cannot be used to offset easy financial conditions, and one may need additional tools to reduce the risks of borrowers overextending themselves.

Finally, monetary policy may not be able to ease aggressively enough when it is already at the lower bound. When financial or economic shocks result in stress on the financial system, the relaxation of macroprudential buffers can help alleviate those stresses, complementing an easing of monetary policy. Such relaxation can also help keep open the transmission of monetary policy, reducing the chance that monetary policy reaches its lower bound ( Nier and Kang, 201 6 ).

Timing

Operationalizing cyclical macroprudential policy requires addressing some thorny questions: at what point should prudential policy tools be used for cyclical macroprudential purposes, and by how much should they be adjusted? The challenge is that we have very little evidence to guide us.

A first key issue is: at what horizon do indicators forecast risks? In general, leverage type indicators like credit-to-GDP, household leverage, or corporate sector leverage tends to forecast downside risks at medium term horizons, such as 2 to 5 years into the future, while the household debt service ratio dominates at shorter horizons ( Drehmann and Juselius, 2014 ). Market indicators such as asset prices or financial conditions indices tend to have even shorter forecasting power, though of course the chart above does tend to indicate that financial conditions may also contain information about medium term imbalances.

In general, one can visualize a term structure of financial stability risks, which is spanned by different indicators at different horizons. The financial stability risks could be measured in the aggregate, or by subsectors. Such a term structure of financial stability risks could help macroprudential policy makers in determining what type of tools should be deployed at what point in time. In fact, the upcoming analytical chapters of the GFSR present some tentative results showing how the term structure of global financial stability risks is forecast by household leverage and by financial conditions.

Another key consideration in deploying macroprudential tools are implementation lags. While monetary policy transmission is subject to lags, the policy stance can be changed at a moment’s notice, prudential policy tools, however, often take many months, or even a full year to change. Hence, they are typically not well suited for addressing rapidly changing risks in the tightening phase. However, in response to an adverse shock, prudential policy tools can certainly be released quickly: this was the case in the U.K., when the CCyB was lowered following the Brexit referendum ( Bank of England, 2016 ); or when banks’ leverage ratio were eased following the September 11 attacks in 2001.

The way forward

I have argued that cyclical macroprudential policy might aim at mitigating sharp movements in financial conditions, even if those do not entail system disruptions in the intermediation capacity of the financial system. There is ample evidence that adverse movements to financial conditions impact risks to GDP growth adversely even in the absence of systemic disruptions.

The economic channels that I have laid out link the ease of financial conditions to the buildup of vulnerabilities. When financial conditions deteriorate, vulnerabilities are reduced, with adverse impacts on real activity. Importantly, the buildup and the unwinding of vulnerabilities has asymmetric effects on economic activity.

Of course, I am not arguing that policy makers should target financial conditions directly. Rather, the monitoring of financial conditions and vulnerabilities provides useful information about downside risks to GDP in the short and medium run, thus usefully guiding the stance of policy.

Thank you.

References

Acharya, V.V., H. Le and H. S. Shin, 2016, Bank Capital and Dividend Externalities, Bank for International Settlements BIS Working Papers, No. 580.

Adrian, T., E. Friedman, and T. Muir, 2015, The Cost of Capital of the Financial Sector, Federal Reserve Bank of New York FRBNY Staff Report, No. 755.

Adrian, T. and H. S. Shin, 2010, Liquidity and Leverage, Journal of Financial Intermediation, Vol. 19, pp. 418-437.

__________, 2014, Procyclical Leverage and Value-at-Risk, The Review of Financial Studies, Vol. 27, pp. 373−403.

Bank of England, 2016, Financial Stability Report, Issue No. 40, November 2016.

Baron, M. and W. Xiong, 2017, Credit Expansion and Neglected Crash Risk, The Quarterly Journal of Economics, Vol. 132, pp. 713−764.

Brunnermeier, M. K. and Y. Sannikov, 2014, A Macroeconomic Model with a Financial Sector, American Economic Review, Vol. 104, pp. 379−421.

Cheng, I., S. Raina, and W. Xiong, 2014, Wall Street and the Housing Bubble, American Economic Review, Vol. 104, pp. 2797−2829.

Claessens, S., M. A. Kose, and M. E. Terrones, 2009, What Happens During Recessions, Crunches and Busts?, Economic Policy, Vol. 24, pp. 653−700.

Drehmann, M. and M. Juselius, 2014, Evaluating Early Warning Indicators of Banking Crises: Satisfying Policy Requirements, International Journal of Forecasting, Vol. 30, pp. 759−780.

Eggertsson, G. B. and P. Krugman, 2012, Debt, Deleveraging, and the Liquidity Trap: A Fisher-Minsky-Koo Approach, The Quarterly Journal of Economics, Vol. 127, pp. 1469−1513.

Geanakoplos, J, 2010, The Leverage Cycle, In Acemoglu, D., K. Rogoff, and M. Woodford (eds.) NBER Macroeconomics Annual 2009, Vol. 24, pp. 1−65.

Greenwood, R. and A. Shleifer, 2014, Expectations of Returns and Expected Returns, Review of Financial Studies, Vol. 27, pp. 714−746.

Guerrieri, V. and G. Lorenzoni, 2017, Credit Crises, Precautionary Savings, and the Liquidity Trap, The Quarterly Journal of Economics, Vol. 132, pp. 1427−1467.

International Monetary Fund, Financial Stability Board, and the Bank for International Settlements, 2016, IMF-FSB-BIS Elements of Effective Macroprudential Policies—Lessons from International Experience, August 31, 2016.

Jorda, O., M. Schularick, and A. M. Taylor, 2013, When Credit Bites Back, Journal of Money, Credit, and Banking, Vol. 45, pp. 3−28.

Mian, A. and Amir Sufi, 2009, Household Leverage and the Recession of 2007 to 2009, Paper presented at the 10th Jacques Polak Annual Research Conference Hosted by the International Monetary Fund, Washington, DC─November 5−6, 2009.

__________, 2014, House of Debt: How They (and You) Caused the Great Recession, and How We Can Prevent It from Happening Again , Chicago: The University of Chicago Press.

Nier, E. and H. Kang, 2016, Monetary and Macroprudential Policies – Exploring

Interactions, In Bank for International Settlements BIS Papers, No. 86, pp. 27−38.

Nier, E. and L. Zicchino, 2008, Bank Losses, Monetary Policy, and Financial Stability—Evidence on the Interplay from Panel Data, International Monetary Fund IMF Working Paper, WP/08/232.

[1] Speech prepared for the annual conference of the European Systemic Risk Board of the European Central Bank in Frankfurt, Germany, on September 21-22, 207. The author thanks Erlend Nier for help in drafting the speech. Nellie Liang, Fabio Natalucci, Gaston Gelos, Dong He, Aditya Narain, Christopher Rosenberg, Ratna Sahay and Thorvardur Olafsson provided helpful comments.