A Changed Global Landscape: Policy Priorities in CESEE

May 23, 2025

It is a great pleasure to be with you in Ljubljana.

Let me begin by setting the stage for what I hope will be an insightful discussion on policy options in the presence of geoeconomic shocks and uncertainty.

I will focus on Central, Eastern and Southeastern European (CESEE) countries.

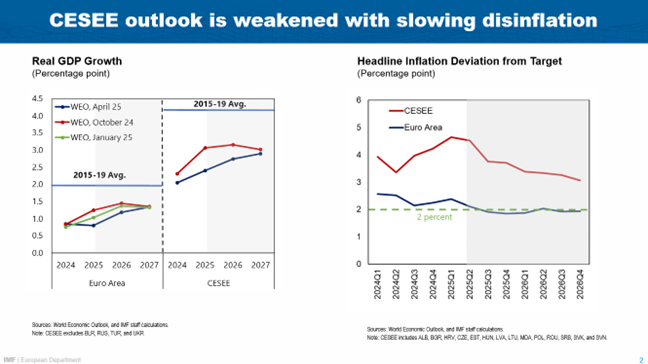

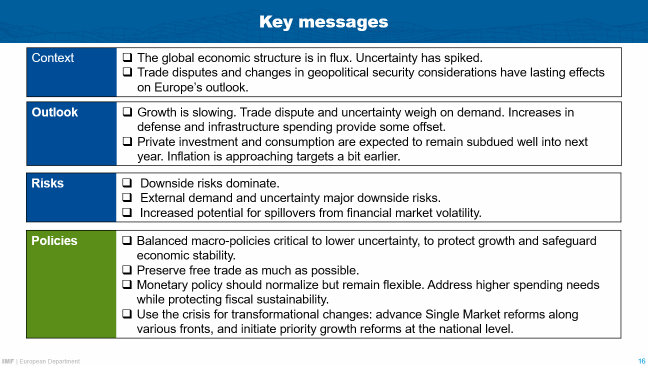

After a respectable recovery last year, we downgraded growth for 2025 and 2026 across Europe

Heightened uncertainty and trade policy volatility have been the main factors. And the latest data releases from Q1 2025 are so far in line with our forecast.

The downgrade for the CESEE region[1] has been more sizeable than for advanced Europe: from over 3 percent in 2025 and 2026 to 2.4 and 2.7 percent respectively.

The larger impact is primarily due to a comparatively larger manufacturing sector. The growth revision would have been even larger if not for the German infrastructure package and an acceleration of Europe wide-defense spending

Inflation in CESEE countries meanwhile is coming down somewhat faster. But, as the chart shows, inflation rates will remain above targets for some time. Persistent services inflation and lagged effects of still high wage growth are key drivers – a point I will return to later as a risk to competitiveness.

In my remarks today, I will address two points: (i) how the changing global landscape is affecting CESEE countries and (ii) what the key policy priorities are.

Let me give a summary of my key points

- What do we know so far about the effects of trade disputes including via trade diversion?

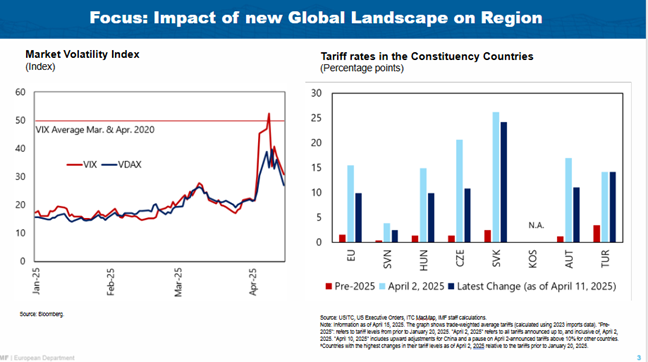

In a nutshell, the impact across the CESEE regions varies widely. Some of the most US-tariff-exposed countries, namely Hungary and Slovak Republic and to a lesser extent the Czech Republic, are in the constituency.

The tariffs between the US and China have just been lowered from very extreme levels, but they remain high and could increase again. Economic spillovers could be large for some specific sectors, even though our preliminary assessment is that the trade diversion effects should be manageable overall.

- What can policymakers do to navigate a more uncertain and volatile period?

Primarily, changes are permanent. Businesses and households will need to adapt to these. A principle-based approach can help lessen the impact.

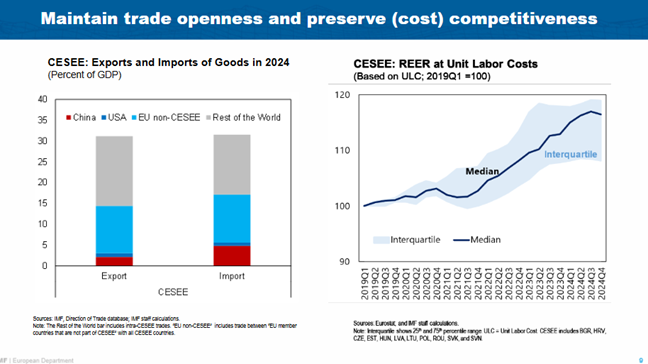

- First, maintain trade openness as much as possible. Protectionism will hurt inward investment, lower investment further and bring down productivity and income growth.

- Second, stay the course on sound macroeconomic policies. In times of uncertainty, markets will scrutinize fundamentals. Durable policies can limit increases in risk premia. This means that central banks should remain cautious on monetary normalization and governments need to keep an eye on fiscal sustainability.

- Third, generate growth through traditional means: domestic structural reforms. The size of untapped gains from domestic structural reforms is surprisingly large.

- The question here is how the CESEE region can overcome political constraints. In my final observation I will discuss how the EU budget can play a catalyzing role.

I will highlight two channels:

- Direct exposure to US tariffs

- Potential effects of trade diversion from US-China trade dispute

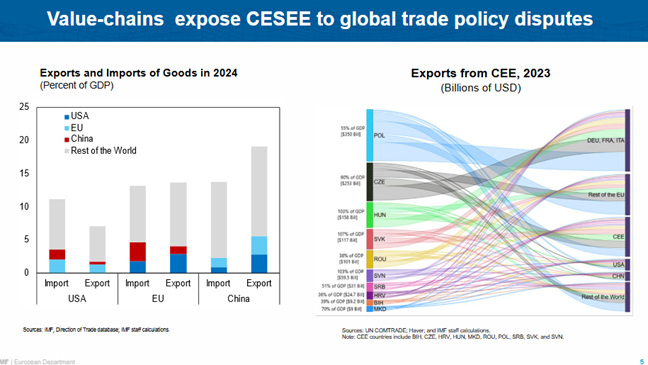

The CESEE region’s integration into global value-chains and trade linkages creates exposure to shifting trade dynamics.

The EU has sizable direct trade linkages with China and the US (LHS), and linkages by individual CESEE countries to the US are substantial.

Exposures are especially large in the Slovak Republic and Hungary. Exports to the US (primarily cars, car parts, batteries, and in the case of Hungary electronics) account for about 3 per cent of GDP in 2024.

Czechia and Hungary have also large export positions to the US via smartphones and computers exports. For the time being, tariffs on these items have been exempted per the announcement made on April 11.

Any increase in tariffs would have substantial dampening effects on growth.

Indirect effects via supply chains will also become important tailwinds. In a 2024 IMF study, we show that an increase in EV imports from China could have significant GDP effects in the range of 1-1½ percent over 5 years via the supply chains in CESEE countries heavily reliant on the automotive sector. A slowdown in Germany’s automotive sector has about a 5-10 times larger impact in percent of GDP in Slovakia and Hungary given their larger share of the sector relative to Germany.

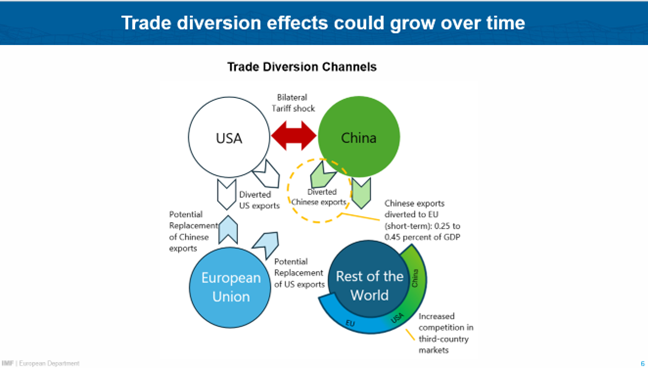

If US-China trade tensions persist, multiple channels of trade diversion could come into play.

EU imports from China could increase, U.S. companies could try to find new export destinations including in Europe, and European firms could seek to find new export opportunities in the U.S. and China as a result of high China-U.S. tariffs.

Finally, competition on third-country markets could increase as countries look for new export markets. CESEE countries could be innocent bystanders. For instance, Turkish businesses could experience increased competition in third markets reducing margin or market shares.

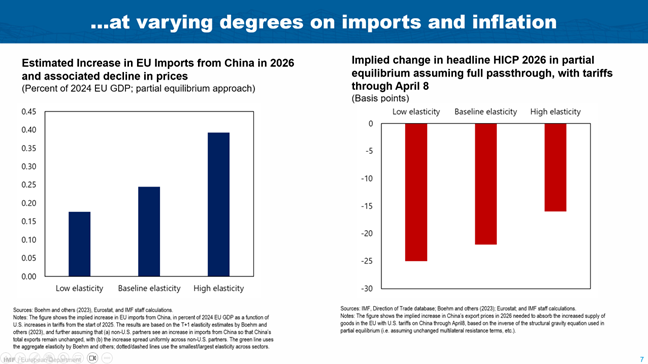

We have estimated the potential size of trade diversion from China using a partial equilibrium approach.

Our preliminary estimates from April 8 tariff announcements[2] for the EU are for higher imports from China of around 0.25 percent of EU GDP in the near term.[3] The estimates are similar to ECB estimates discussed in their latest economic Bulletin. The 90-day rollback of most bilateral tariffs imposed since April 2 announced by the US and China on May 12 implies lower numbers, but better to be prepared for the worst.

Trade diversion would also affect inflation. Increased import competition would likely lower final prices. Headline inflation could be reduced by 20 basis points in 2026.

The economic effects for consumers and producers are likely mixed. Lower final goods prices would benefit consumers. Similarly, lower imported intermediates could also benefit European firms by reducing input costs. But trade diversion means also a rise in competition and in specific sectors such as consumer electronics or transportation equipment, adjustment effects could be large.

With all that said, the aggregate size of trade diversion effects appears manageable, although the impact could be large in individual countries and sectors.

Let me turn to policy priorities.

Let me now say a few words on what the CESEE region can do in the face of tariffs.

- First, Europe—and everyone—needs more trade, not less. The EU as well as CESEE should continue its open trade policy and expand its network of trade agreements.

- Second, we must accept that the global trade regime has changed. This means that any support to mitigate tariff or trade diversion effects should remain temporary, and targeted.

Support measures cannot substitute for differences in the underlying fundamentals. In particular, the recent appreciation of CESEE currencies in unit-labor-cost adjusted terms is a concern.

What can policymakers do in the short term?

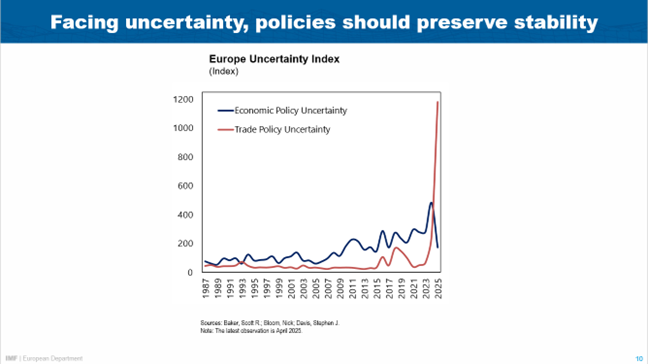

In the current global environment, navigating uncertainty is crucial.

In the short run, governments should aim to retain macroeconomic stability through credible and sustainable macroeconomic policies and build resilience.

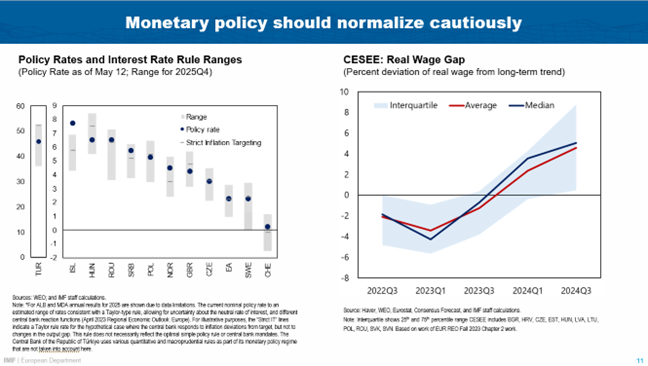

Starting with monetary policy, central banks need to remain focused on durably reaching price stability targets.

- In several large CESEE countries—including Hungary—inflation is slowing, but is still above targets.

- Central banks should ease cautiously. We advise caution because core inflation in the CESEE region remains higher than hoped for, and inflation expectations are more responsive to current inflation levels.

Still high wage growth requires close attention. Increases have outpaced productivity and are contributing to higher inflation persistency. High labor costs also pose a risk to CESEE’s competitiveness.

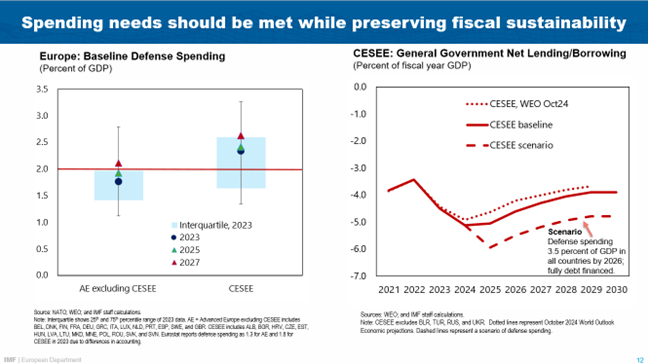

Our fiscal advice remains broadly unchanged. For many countries, rebuilding fiscal buffers is still a priority.

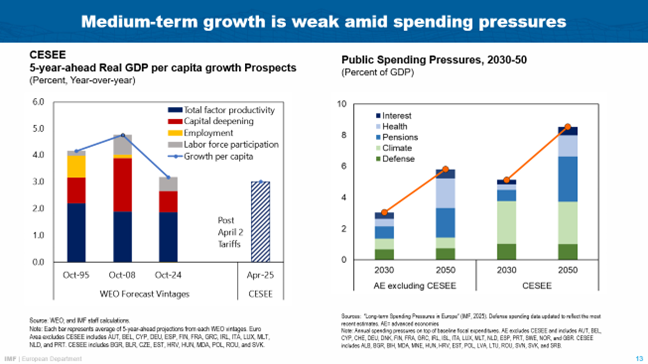

- The challenge is how to manage rising long-term spending pressures from aging, healthcare, climate, and now higher defense spending.

- Some countries can accommodate temporary increases in priority spending while keeping debt sustainability in mind.

- But for many CESEE countries the space is limited. This means they will have to undertake smart adjustments: (i) make public services more efficient and programs better targeted; (ii) reallocate spending priorities away from low priority areas, (iii) and boost fiscal revenues. In many cases, this can be done without raising tax rates by closing loopholes and more efficient administration.

We continue to have concerns about Europe’s medium-term outlook: growth is low and there are rising spending needs:

- Labor supply is dwindling because of aging.

- Investment has been slowing.

- And Europe’s productivity growth has been very low over the last two decades.

This makes meeting fiscal pressures increasingly difficult.

- Spending needs are expected to rise significantly over the next decades, for advanced economies by 5¾ percentage points and emerging economies by 8 percentage points of GDP.

- In the CESEE region, energy-related investments needs are urgent and very large.

- And across the region, defense spending is on the rise.

This brings us to my final point which is how CESEE countries could generate medium-term growth.

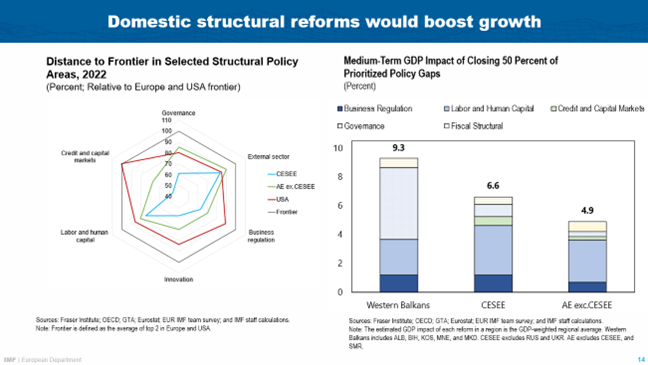

Domestic structural reforms, while often overlooked, provide a large untapped source of European growth potential.

- In a forthcoming study, we find that comprehensive national reforms could raise real GDP levels by about 5 percent in advanced economies and between 6.6 and 9.3 percent in the CESEE region.

- These are sizeable gains and could be an important growth antidote to the poisonous effects of uncertainty and volatile policy disputes.

These reforms would remove inefficiencies at home and complement the earlier discussed EU-wide reforms. Specifically:

- Domestic labor market and skill-upgrading reforms top the priority list in terms of their macroeconomic

- Fiscal-structural reforms and lower cost of business regulations would provide another substantial impetus.

- Reducing corruption and inefficiencies through governance reforms is particularly important in several CESEE countries.

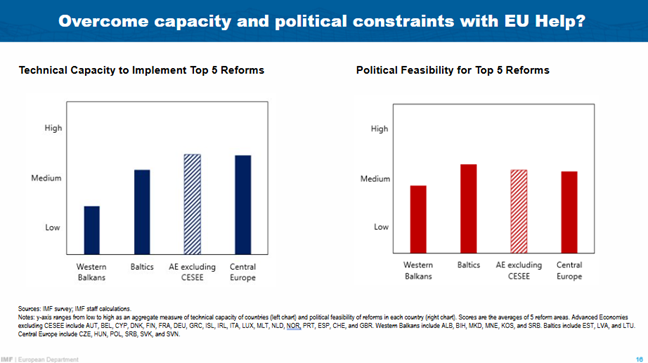

Successful implementation of these reforms will require political will, and in some cases, also capacity building.

Overcoming the reform inertia is “the challenge” of Europe.

Let me conclude with a few observations on how to overcome this obstacle.

We think the EU budget could play a catalyzing role. Recent initiatives—such as the Recovery and Resilience Facility (RRF)—have made important strides in strengthening policy performance. The next Multiannual Financial Framework (MFF) for 2028-2034 should build on this momentum, further embedding a performance-based approach, especially in areas where current incentives are weak, but outcomes depend heavily on effective effort.

This is particularly relevant for pre-allocated funds tied to national plans, where member states design and implement policies. In such cases, stronger performance incentives can help ensure that investments yield meaningful results.

To maximize the impact of EU financing, the budget could reward projects that complement EU-level objectives—for example, national reforms like streamlining permitting processes for local distribution networks that connect with cross-border energy infrastructure.

At the same time, policy coherence across all levels of government is essential. While the EU budget can offer strategic direction and alignment incentives, successful implementation ultimately depends on ownership at national, regional, and local levels. The EU budget can set incentives, but decisions need to be made at home.

Let me conclude here …

…and leave with a slide on our key messages.

I now look forward to hearing from you. Thank you!

[1] Excluding Belarus, Russia, Türkiye and Ukraine.

[2] “April 8 tariffs” refers to the tariff increases between the US and China announced just before the 90-day pause on April 9.

[3] This figure decreases to 0.09 percent with the May-12 tariffs

IMF Communications Department

MEDIA RELATIONS

PRESS OFFICER:

Phone: +1 202 623-7100Email: MEDIA@IMF.org