Liquid markets

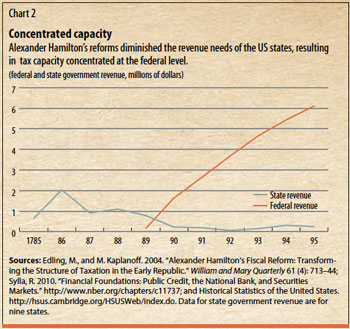

Hamilton was motivated by several additional considerations. Politically, he sought to ensure the allegiance of creditors to the federal government; institutionally, he wanted to foster deep and liquid markets for Treasury securities. A further political motivation was related to the fundamental matter of assigning taxation across levels of government. There were two issues to consider: first, the Constitution gave the federal government the exclusive right to levy tariffs. Overlapping authority for other instruments of taxation opened the door for tax competition among the states. Second, the federal government would assume states’ debt and therefore the interest payments that comprised the biggest expenditures in most states. In this way, the federal government would diminish the revenue needs of the states, with the result that the ability to tax would be concentrated at the federal level (see Chart 2). Hamilton proposed to shape the structure of government through the structure of the public finances.

Given the controversial nature of Hamilton’s report, it is not surprising that by June 1790, Congress had not yet decided to assume the debt of the states. On June 2, the House of Representatives passed Hamilton’s funding bill, but without the debt-assumption provision. Then another divisive issue emerged: where to locate the nation’s capital. The choice would not only increase the economic well-being of the host city but would have an indirect, albeit important, influence on political and policy decisions. Hamilton favored New York, which would thus become the center of political and financial power, like London—a perfect fit for his plan for a strong central government. On the other hand, Virginians such as Jefferson and Madison wanted the seat of government to be on the banks of the Potomac. A compromise was struck at that historic dinner, and in July 1790, Congress passed the Residence and Assumption bills in quick succession.

Jefferson nevertheless remained dissatisfied. More than two years later, in September 1792, the nation’s first secretary of state referred to the episode in a letter to President Washington:

“When I embarked in government, it was with a determination to intermeddle not at all with the legislature & as little as possible with my co-

departments. The first and only instance of variance from the former part of my resolution, I was duped by the Secretary of the Treasury and made a tool for forwarding his schemes, not then sufficiently understood by me; and of all the errors of my political life, this has occasioned me the deepest regret.”

Why the deepest regret? Ensuring financing of federal government operations and the assumption of states’ debt were only the first part of Hamilton’s program. By putting in place centralized public finances in support of a vigorous executive, Hamilton was ready to start carrying out specific policies in the areas of financial stability, crisis management, and trade. From that point of view, agreeing to separate the country’s political capital from its financial center was a minor concession.

It was now clear that the early policy confrontations between the two camps were signs of fundamental differences. In 1792, Madison and Jefferson organized their party to rival the Federalist party. That decision marked the beginning of professional, competitive party politics as a cornerstone of representative democracy in the United States. Fiscal policy, finance, and politics are inextricably intertwined. The same is true of debt, taxes, and state capacity.