IMFSurvey Magazine: Countries & Regions

Cotton workers in Tajikistan: CCA oil importers are seeing lower growth as a result of economic developments in Russia, says a new forecast by IMF staff (photo: ZUMA Press/Newscom)

REGIONAL ECONOMIC OUTLOOK

Caucasus, Central Asia Face Dimmer Growth Prospects

IMF Survey

November 3, 2014

- Slowdown in Russia weighs on growth, with oil importers hit hardest

- Countries should focus on gradual strengthening of fiscal cushions

- Structural reforms needed for sustainable, inclusive, and diversified growth

Growth in the Caucasus and Central Asia is expected to decline by about one percentage point of GDP in response to the slowdown in Russia, says the latest regional forecast by IMF staff.

The Regional Economic Outlook for the Middle East and Central Asia, released on November 4, projects that growth will fall to about 5.5 percent this year and next, in part owing to the region’s close ties with its economically struggling neighbor.

“Weaker growth in the CCA region stems from the economic slowdown and increased geopolitical risks in Russia, coupled with weaker domestic demand in a number of countries due to fiscal tightening and flat oil production in some countries,” Juha Kähkönen, Deputy Director of the IMF’s Middle East and Central Asia Department, told reporters in Almaty, Kazakhstan.

Economic developments in Russia significantly affect the growth prospects of the CCA region through a number of channels, mainly trade, remittances and investments. A protracted period of slower growth in other trading partners, particularly Europe or China, could also have a negative impact over a longer time horizon, the report cautioned.

Oil exporters see softer growth, dwindling budget and external surpluses

The CCA’s oil exporters—Azerbaijan, Kazakhstan, Turkmenistan, and Uzbekistan—are expected to see growth soften to 5.6 percent this year from 6.8 percent in 2013. These countries are shielded to some extent from Russia’s slowdown, thanks to diversified export markets and the high oil prices of recent years, which allowed large fiscal cushions to be built up.

Non-oil growth in the oil-exporting countries is nonetheless forecast to decline by about 1 percentage point, because of slower consumer lending, increased investor caution, and higher geopolitical risk related to the conflict between Russian and Ukraine, the IMF staff said.

Moreover, the recent decline in oil prices adds uncertainty to the outlook, Kähkönen told reporters. The region’s oil exporters are vulnerable to a prolonged period of low oil prices. Growth in these economies may slow further as oil revenues fall, while fiscal and external surpluses would weaken unless governments take policy action.

Weaker external demand, especially from Russia, is putting pressure on the current account balances, with the surpluses of the CCA oil exporters shrinking appreciably. Fiscal surpluses are experiencing a similar downward trend, with an expected drop to 2.1 percent of GDP this year and 1.4 percent in 2015, down from 3.4 percent in 2013.

Despite the more subdued growth, inflation is expected to rise throughout the region. Oil exporters will see a slight increase in inflation to 6.5 percent this year, up from 6.3 percent in 2013, mainly driven by recent currency devaluation/depreciation in some countries.

Lower trade and remittances in oil importers

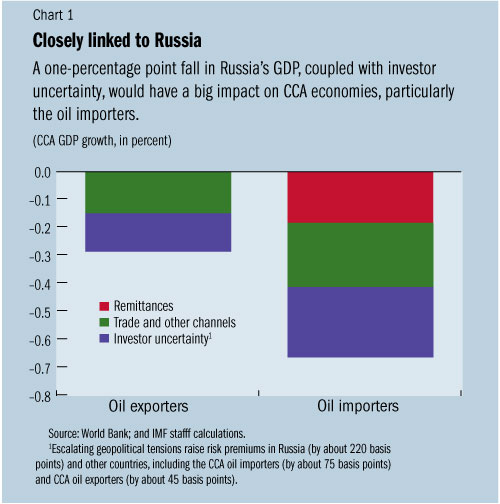

Growth in the CCA’s oil importers—Armenia, Georgia, Kyrgyz Republic, and Tajikistan—is forecast to slow by a full percentage point this year, to 4.6 percent of GDP. Because these countries have close trade and remittance linkages with Russia—as well as limited fiscal cushions—they will see a greater impact from Russia’s slowdown than the CCA’s oil-exporting countries, the IMF staff’s report noted (see Chart 1).

Lower remittances from Russia, in particular, will cause the current account deficit of these countries to widen to more than 8 percent of GDP in 2014-15 from 7 percent in 2013 (except in Armenia, where remittances have remained resilient).

Fiscal deficits are likewise expected to worsen this year. For countries such as Armenia and Georgia, though, a pause in fiscal consolidation may be warranted to allow growth to take hold, the report notes. A return to gradual consolidation over the medium term would be essential to build up buffers and place public debt on a declining path, the report adds.

Inflation is an issue for the CCA oil importers, as it is for the region’s other countries, with the rate forecast to rise to about 5 percent in 2014-15 from 3.6 percent in 2013. This rise in inflation is partly attributable to pressure on the Kyrgyz and Tajik currencies from a weakening of the Russian ruble and rising domestic food prices.

And the recent drop in oil prices will also affect the CCA oil importers, although the exact impact is as yet uncertain, Kähkönen suggested. While these economies would benefit from lower oil import bills, they are particularly exposed to negative spillovers from Russia, an economy that itself depends heavily on oil.

New economic model needed

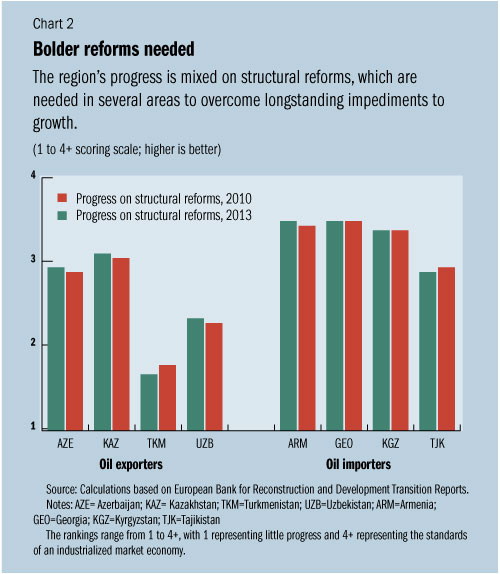

Despite two decades of solid economic performance, inequality in the CCA remains high, along with youth unemployment and emigration. Moreover, the region’s past growth was mainly driven by volatile sources such as commodity exports and remittance flows, the report noted. Structural reforms in several areas are required to overcome the long-lasting impediments to sustainable and inclusive growth (see Chart 2).

To move to a fairer, more viable development model, the report recommends that the region’s policymakers give priority to the following:

• Carrying out bold structural reforms to develop worker talent, increase competitiveness, and create an environment conducive to private sector-led growth;

• Promoting inclusive growth through better access to finance for small and medium-sized enterprises and a deeper, more stable financial system;

• Creating a diverse and dynamic non-oil tradable sector to diversify the region’s economies and reduce their dependence on oil and gas; and

• Pursuing broad-based, balanced trade integration at both the regional and multilateral levels.

Stay Connected

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Write to us

The IMF Survey welcomes comments, suggestions, and brief readers' letters, a selection of which are posted under What readers say. Letters may be edited. Please address Internet correspondence to imfsurvey@imf.org.