Germany’s Real Challenges are Aging, Underinvestment, and Too Much Red Tape

March 27, 2024

Germany faces some serious economic challenges, but they aren’t necessarily the ones getting the most attention. Solving these challenges requires ambitious reforms

Germany is struggling. It was the only G7 economy to shrink last year and is set to be the group’s slowest-growing economy again this year, according to our latest projections. Some pundits say Germany’s economic model is irreparably broken. They argue strong growth in previous decades was based on importing cheap Russian gas, which in turn powered Germany’s highly competitive export industries. With this cheap gas no longer available, the German manufacturing model doesn’t work anymore, or so the story goes.

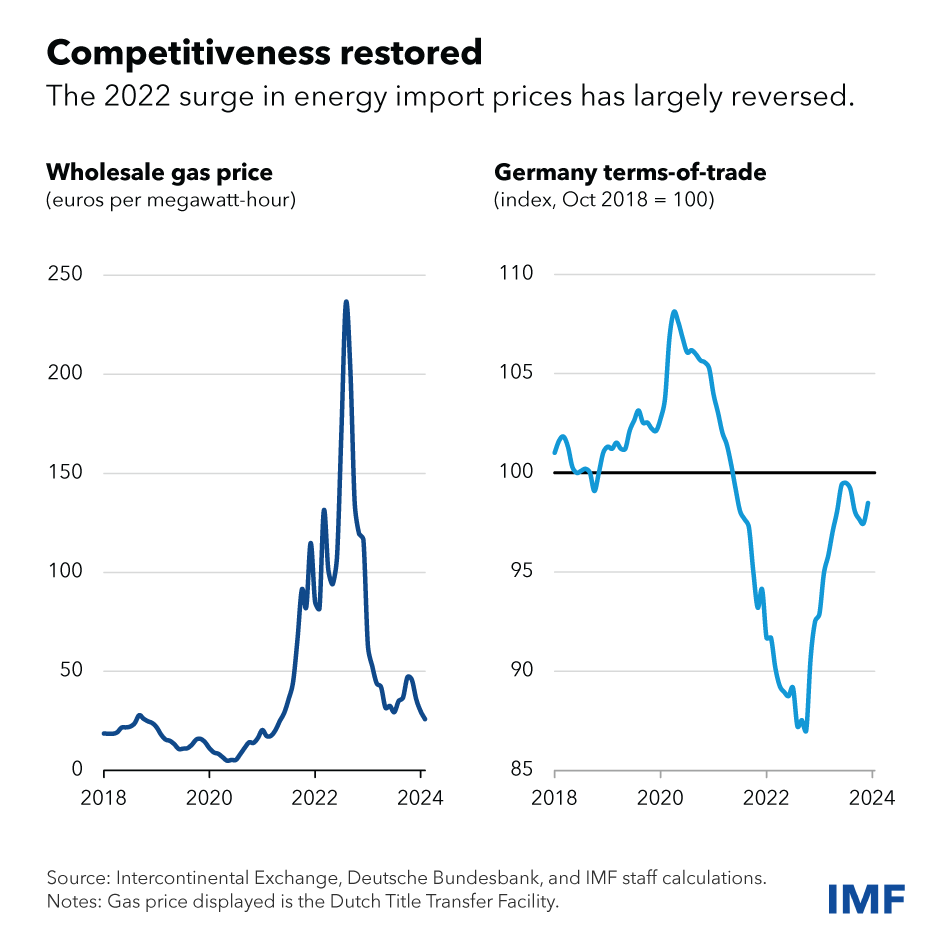

But is this accurate? It’s certainly true that the shutoff of Russian gas in 2022 contributed to spiking inflation and cost-of-living pressures. However, the rise in gas prices has proven to be temporary. After soaring in 2022, wholesale gas prices have now fallen back to 2018 levels.

Broader measures of Germany’s international competitiveness paint a similar picture of substantial recovery: Germany’s terms-of-trade (an index of export prices relative to import prices) has returned to the same level as before the energy shock. And Germany’s trade surplus reached 4.3 percent of GDP last year—lower than the excessively high surpluses of the pre-pandemic years but above the average of the last two decades—and is likely to increase further this year.

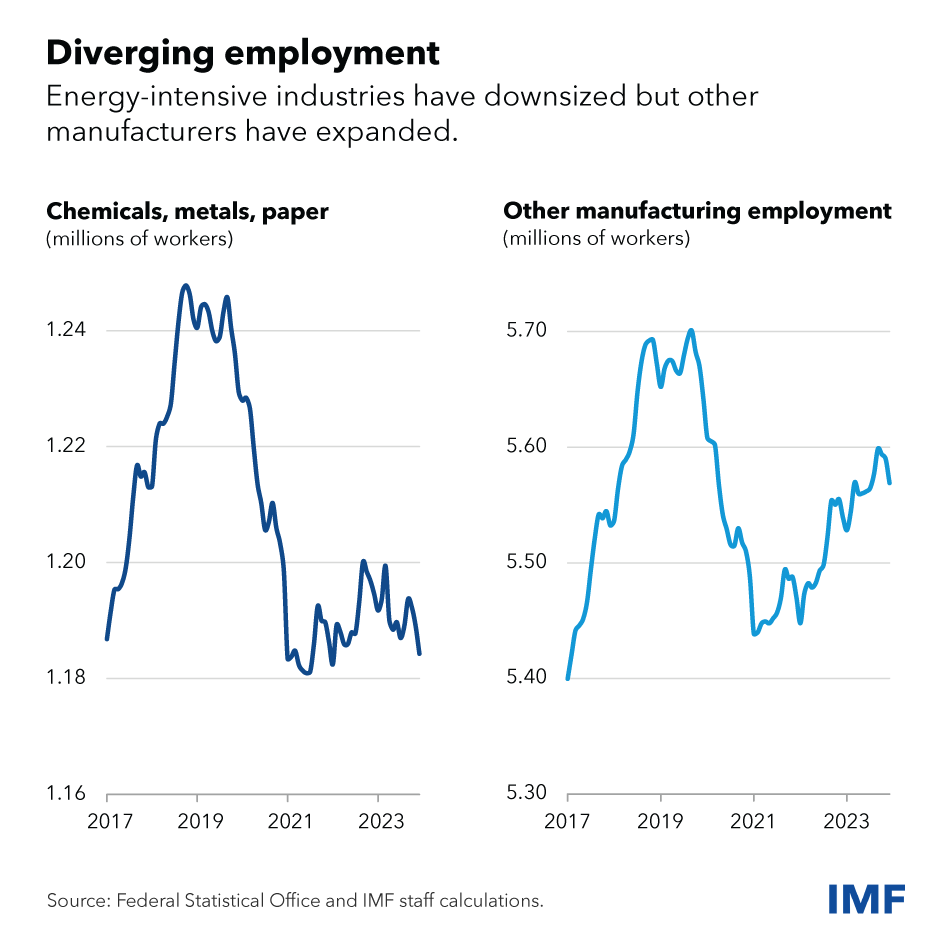

Concerns about widespread deindustrialization are similarly overstated. While the energy-intensive chemicals, metals, and paper industries have contracted, they only account for 4 percent of the economy. Auto production, by contrast, rose by 11 percent last year. Germany's electric-vehicle makers are embracing the green transition. In 2023, Germany’s electric vehicle exports increased by 60 percent. Two German manufacturers for which data are available, Volkswagen and BMW, alone account for over 10 percent of global electric vehicle sales.

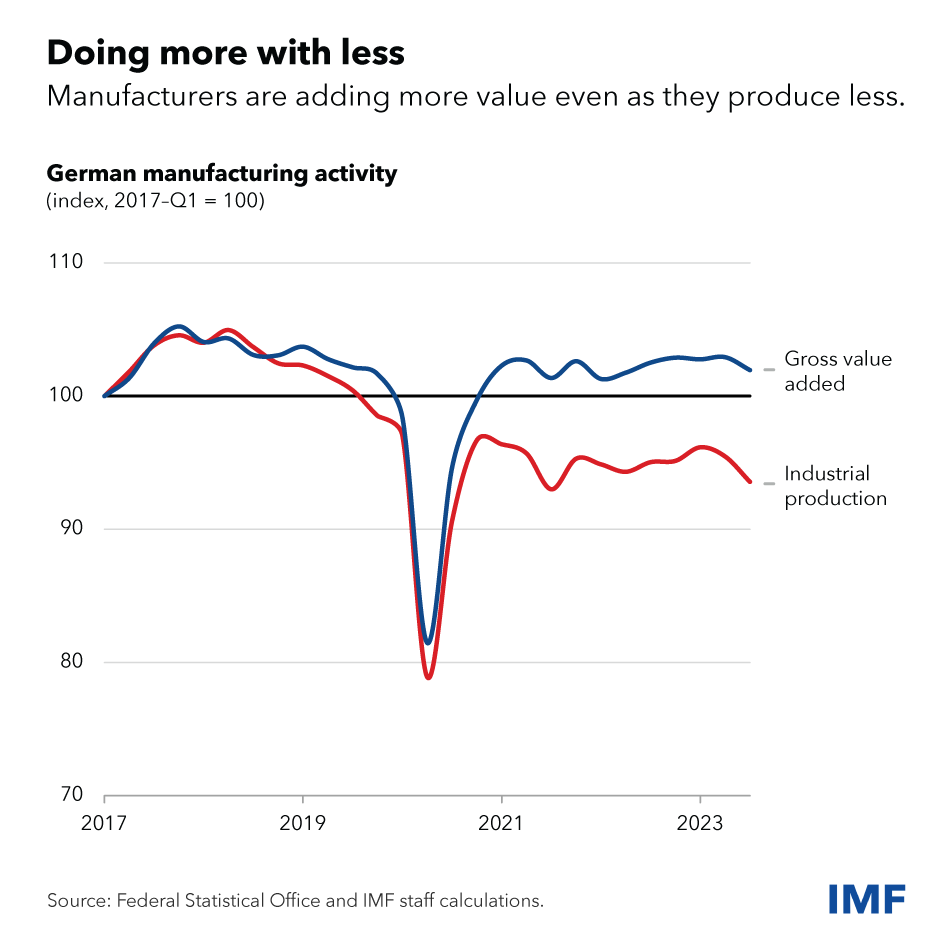

German manufacturers also adapted to the energy crisis and supply-chain disruptions by shifting into higher value-added products and using fewer intermediate inputs. As J.P. Morgan’s Greg Fuzesi and others have noted, this means that manufacturing value-added has remained steady even as industrial production has fallen. Industrial production, in other words, has become a less useful measure of the performance of the economy as a whole.

Why then has Germany’s economy been so weak? This reflects a combination of temporary factors and some more structural ones. On the temporary side, when inflation surged, consumers cut back on purchases. The European Central Bank also raised interest rates to prevent higher inflation from becoming entrenched, which in turn depressed housing construction and other interest-sensitive sectors. A post-pandemic rebalancing of global demand away from manufactured goods and back toward services was also unfavorable for Germany’s manufacturing-intensive economy.

The good news is that these temporary headwinds should gradually fade over the next year or two.

The bad news is that a more fundamental structural headwind—sluggish productivity growth—is likely to remain, absent reforms, while another—population aging—will accelerate sharply.

Making Germany More Productive

These fundamental headwinds are the main obstacles Germany faces in improving its medium-term growth prospects.

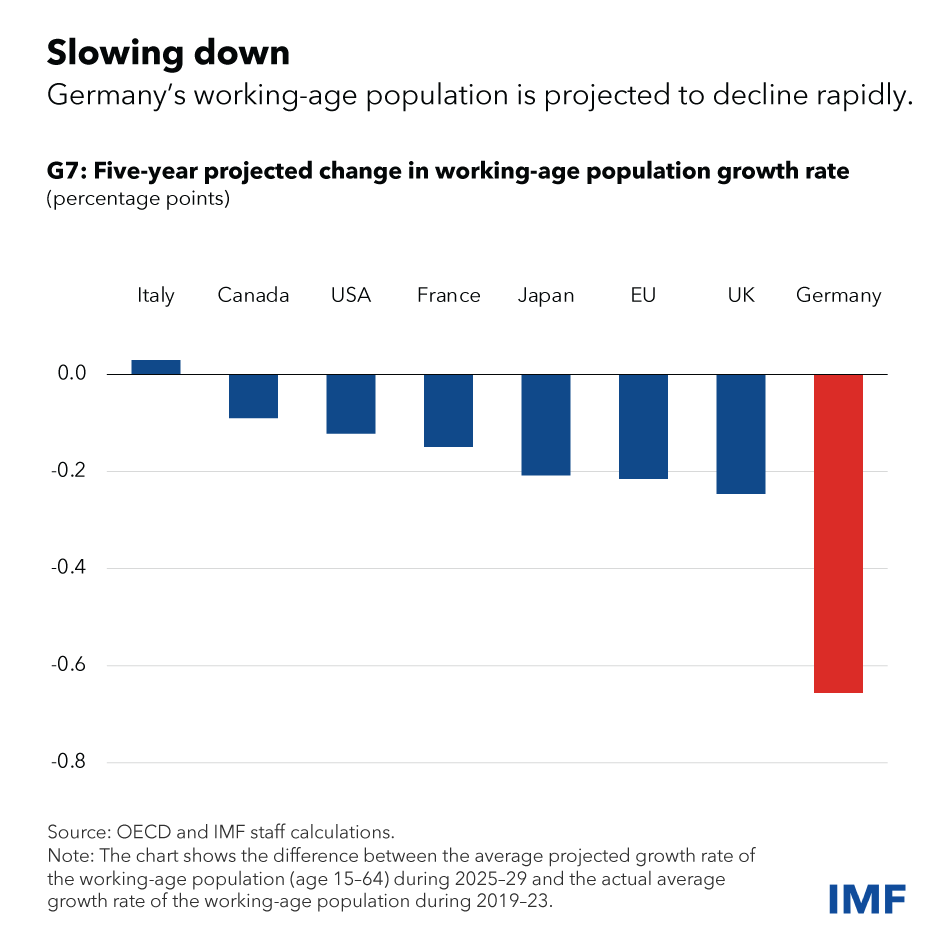

Germany’s working-age population has been buoyed over the last decade by migrants escaping regional conflicts. As this migrant wave ends and baby boomers retire over the next five years, the growth rate of Germany’s labor force will drop by more than in any other G7 country. This will put downward pressure on GDP per person because there will be fewer workers for each retiree. It will also lead to a combination of higher social security contributions and lower pensions, absent reforms. And a more elderly population will increase demand for healthcare services, drawing workers away from other industries. Labor shortages could also deter investment.

Greater immigration could be a powerful force to counter these factors. However, prospects for this are uncertain.

Germany could also increase its labor supply by making it easier for women to extend their working hours. There are 2.3 million fewer women working than men, and women are five times more likely to work part-time. Expanding access to reliable childcare and reducing taxes for secondary earners in married couples could help close these gaps.

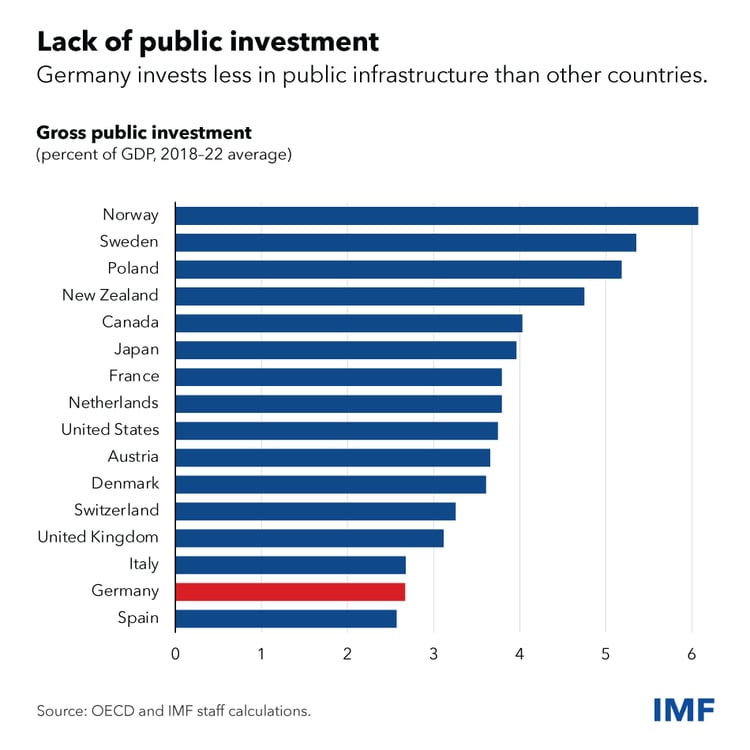

Another solution is to raise productivity, which has been dragged down by inadequate investment in public infrastructure. Public investment declined in the 1990s and, since then, has barely been enough to offset depreciation. This puts Germany near the bottom of advanced economies in public investment. Money that has been budgeted for investment is routinely underspent, often because of staff shortages in municipalities.

To boost public investment, Germany could expand municipalities’ planning capacity though consulting services programs like Partnerschaft Deutschland. Germany could increase financing for public investment by reforming other expenditures, mobilizing more revenue, or adjusting the debt brake limits on federal borrowing, as explained in our most recent staff report. The debt brake could be eased by around 1 percent of GDP while still allowing public debt to decline as a share of GDP.

Productivity could also be enhanced by cutting red tape, which is a barrier to both investment and starting new businesses. For example, it takes about five to six years to get permission to build an onshore wind farm. And it takes 120 days to obtain a business license, more than double the OECD average.

Digitalizing government services could also speed up processes. Germany lags behind other EU countries in offering online services to businesses, including registration and tax filing. For example, only 43 percent of government services pre-fill personal data on online forms compared with the EU average of 68 percent.

Germany faces important economic challenges, but it also possesses policy levers to overcome them and secure a brighter economic future. It’s time to use them.

****

Kevin Fletcher is an assistant director, and Harri Kemp and Galen Sher are economists in the IMF's European Department.