Everyone faces vulnerabilities during their lifetime

Isabel Ortiz

Countries across the world aim to provide social protection for all

citizens or residents, generally by a combination of public social

insurance and social assistance. Social protection, or social security,

includes cash and in-kind benefits provided for children, mothers, and

families; support for those sick and without jobs; and pensions for older

and disabled persons. These benefit schemes are not only for the poor, as

anyone may fall sick, lose a job, or have a child—and everyone inevitably

gets old. Governments recognize the existence of universal needs

among their citizens—reflecting vulnerabilities that all people are likely

to face at least once in their lifetime.

At an international level, the United Nations Sustainable Development

Goals, adopted by world leaders in 2015, commit countries to implementing

nationally appropriate social protection systems for all (universal),

including floors, for reducing and preventing poverty. This commitment

reaffirms the global agreement on the extension of social security achieved

by the International Labour Organization’s (ILO’s) 2012 Social Protection

Floors Recommendation, which was adopted by workers, employers, and

governments from all countries (see box).

Understanding different social protection policies

Universal Social Protection

is a policy objective anchored in global commitments such as Article 22 of

the Universal Declaration of Human Rights, which states that "everyone, as

a member of society, has the right to social security," and other

international commitments, including International Labour Organization

(ILO) standards and Sustainable Development Goal 1.3, part of the United

Nations Agenda 2030.

The Global Partnership Universal Social Protection (USP2030) was launched

at the United Nations in 2016, led by the World Bank Group and the ILO,

showcasing countries that had achieved universal social protection

coverage.

A social protection floor

is a policy and a standard consisting of a nationally defined set of basic

social security guarantees that should ensure, at a minimum, universal

access to essential health care and basic income security. It should ensure

adequate benefits for children, mothers with newborns, the poor, and the

jobless, as well as the sick, disabled, and elderly, through a combination

of contributory social insurance and tax-financed social assistance.

Guaranteed minimum income

is a means-tested scheme of social assistance generally implemented in

countries undergoing austerity or fiscal consolidation. It is not universal

but rather targeted to the poor.

Universal basic income

is an unconditional cash transfer to all residents in a country (a type of

social assistance). Proposals vary considerably in terms of benefit levels,

financing mechanisms, and the benefits and services offered; thus some

universal basic income proposals have positive social impacts while others

result in a net welfare loss. (See "Back to Basics: What Is Universal Basic

Income?" in this issue of F&D.)

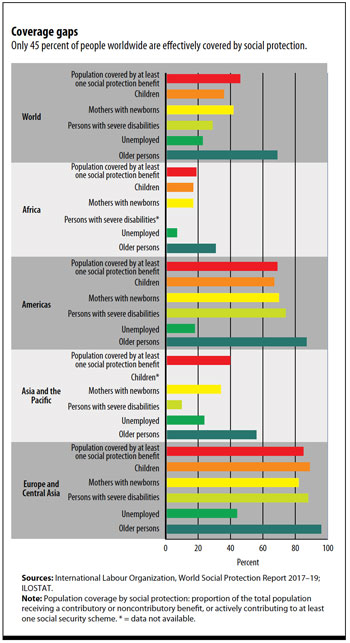

But despite significant progress in the extension of social protection in

many parts of the world, only 45 percent of the global population is

effectively covered by at least one social protection benefit, while the

remaining 55 percent—4 billion people—are left unprotected (see chart).

Coverage gaps are associated with significant underinvestment in social

protection, particularly in Africa, Asia, and the Arab states. In many

countries benefits are low, keeping people vulnerable. On the positive

side, many middle-income countries are advancing fast, and a significant

number of countries have achieved universal or near-universal coverage.

Universal social protection is a key element of national strategies to

promote human development, political stability, and inclusive growth.

Evidence shows that, in addition to reducing poverty and inequality,

well-designed social protection systems with adequate benefits

Contribute to inclusive growth:

They increase productivity and employability by enhancing human capital,

boosting domestic consumption and demand, and facilitating structural

transformation of the economy.

Promote human development:

Cash transfers facilitate access to nutrition, education, and healthcare;

encourage higher school enrollment rates; and bring about a decline in

child labor.

Protect people against losses due to shocks,

such as economic downturns or natural disasters.

Build political stability and social peace,

reducing social tensions and violent conflict.