Loading component...

Speech by IMF First Deputy Managing Director John Lipsky at the Die Zeit Conference

September 9, 2008

| Download the presentation (608 kb PDF) |

Introductory Remarks

Thank you, Mr. Chairman. It is indeed a pleasure to address this distinguished audience.

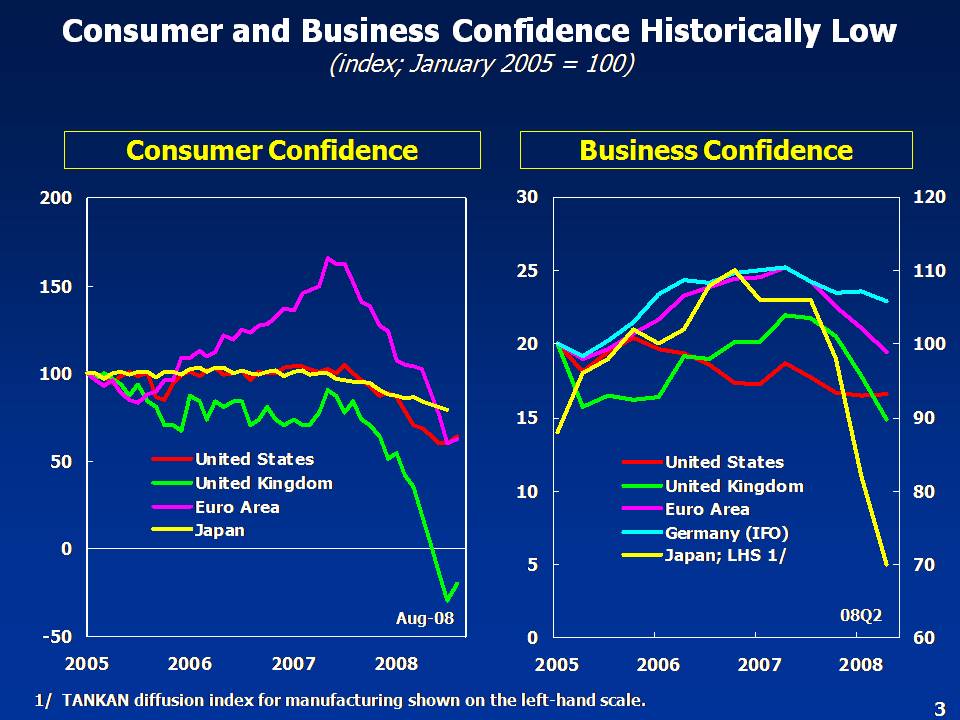

The global economy is facing its most difficult situation in many years as we grapple with the financial crisis that erupted last August together with the impact of high commodity prices. Global growth is slowing markedly, following more than four years of strong expansion, while inflation has risen to rates not seen in a decade, especially in emerging economies. Policymakers across the world are faced with the difficult challenge of nursing their economies through a period of tight credit conditions and higher inflation.

Against this backdrop, I will focus my remarks on a few major themes.

Finally, tackling the immediate challenges—supporting growth and restoring health to the financial system, while keeping inflation at bay—should be viewed against the backdrop of a rapidly changing global landscape, in which emerging economies are increasingly taking center stage. In other words, consistent policies will be needed in all the major economies, if we are to return to the solid growth and low inflation that characterized the best years of this decade.

I will begin with a brief overview of the global economic outlook. Then, I will focus on the continuing financial crisis, discussing what it implies for the world economy, and address the key policy challenges that we face.

Global Outlook

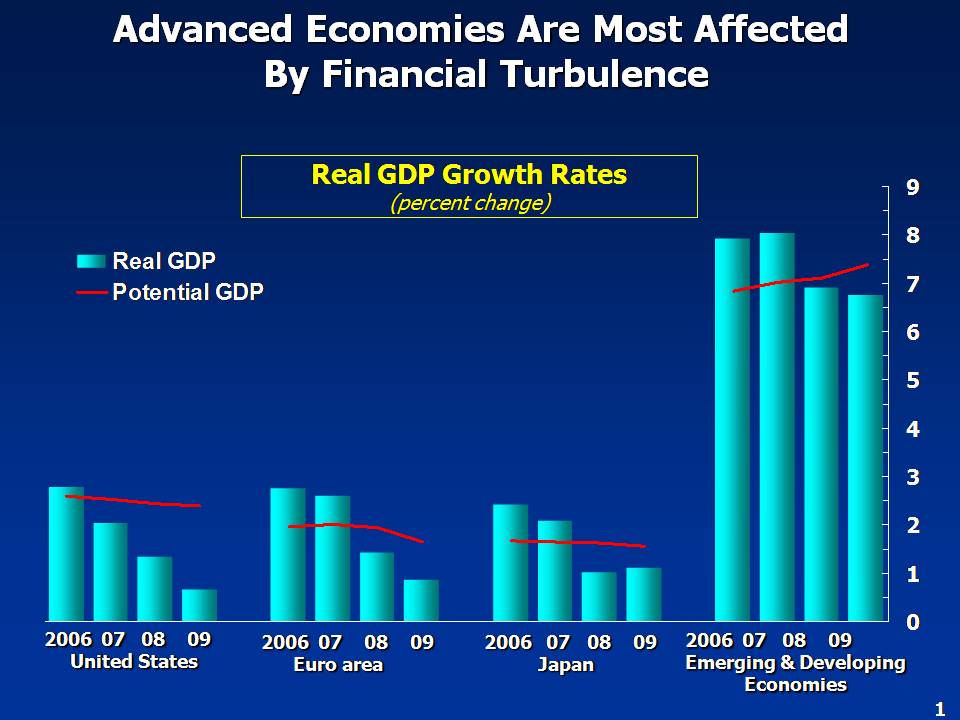

Against the backdrop of protracted financial strains and dramatic surges in commodity prices, the global economy is confronted with its most difficult set of circumstances in many years. Following a remarkable five-year span of strong expansion, global economic activity is decelerating markedly. The growth slowdown originated in the United States, and has clearly spread to Europe and Japan. And advanced economies, in general, face a spell of growth well below potential, as they grapple with ongoing strains from the financial crisis that began a year ago, as well as high oil prices and weaker external demand.

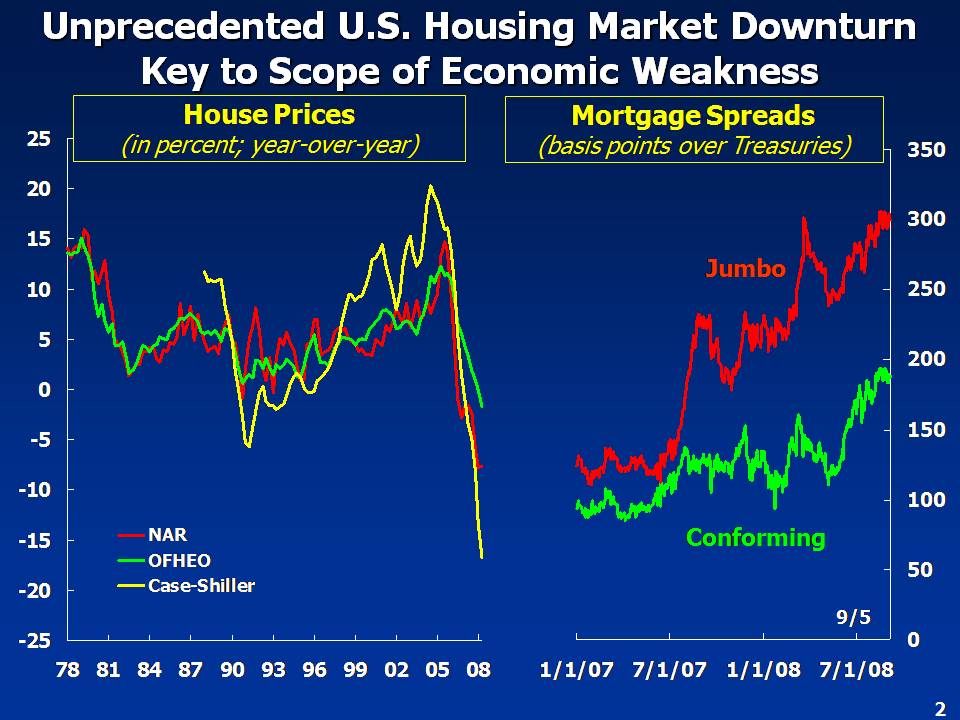

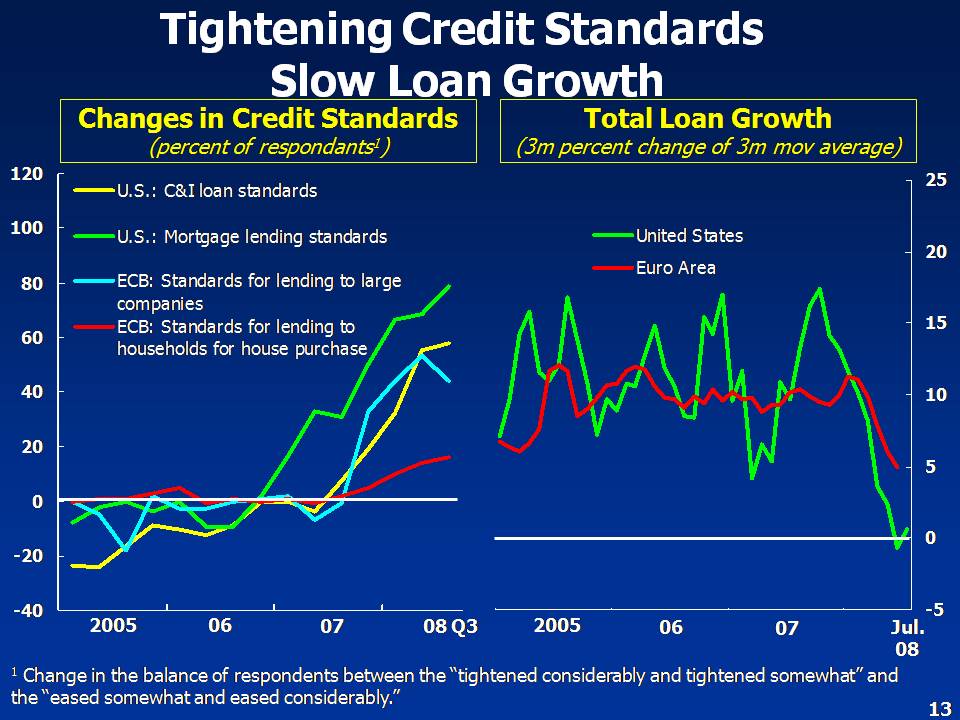

Housing and credit markets remain at the core of the U.S. slowdown. House prices, on a national basis, continue to decline and inventories of unsold homes remain high, and the sizeable drag on growth from residential investment is likely to continue albeit at a diminishing rate. In credit markets, relatively high mortgage rates and tighter lending standards still weigh on housing demand. At the same time, consumption—a key support of the U.S. economy until recently—is facing strong headwinds, such as tighter credit, falling asset prices for both residential real estate and corporate equity, as well as weaker labor markets and sluggish growth of disposable incomes. Under our baseline, U.S. growth on a fourth-quarter-on-fourth-quarter basis would slow to about 1 percent in 2008 and then recover gradually to about 1½ percent in 2009.

In Western Europe, growth is slowing amid weak business and consumer sentiment and softer industrial activity, reflecting terms of trade losses, weaker partner country growth, the impact of strong currencies on trade, and tighter credit conditions. High oil and food prices have cut into real disposable incomes, while financial strains and declining housing markets are increasingly a drag on domestic demand in several countries—including Spain, the United Kingdom, and Ireland. We project growth for the euro area on a fourth-quarter-on fourth-quarter basis at about ¾ percent in 2008 and about 1½ percent in 2009.

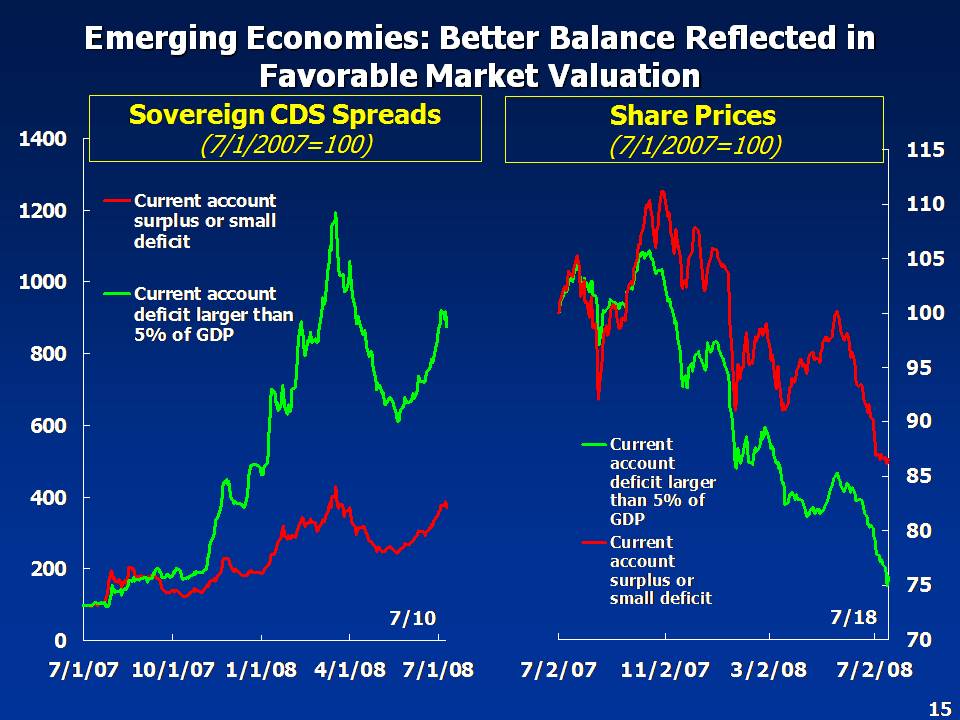

In contrast, notwithstanding some moderation, economic momentum has remained robust in emerging economies. Growth has moderated from more than 8 percent to just over 7 percent over the past year, largely reflecting slower export growth as a result of weaker demand from advanced economies. Nonetheless, growth in the largest emerging economies—Brazil, China, India, and Russia—continues to contribute about 40 percent to global GDP growth. While not at the center of the slowdown, emerging economies—where domestic demand has held up remarkably well—are being affected too, through both trade and financial channels.

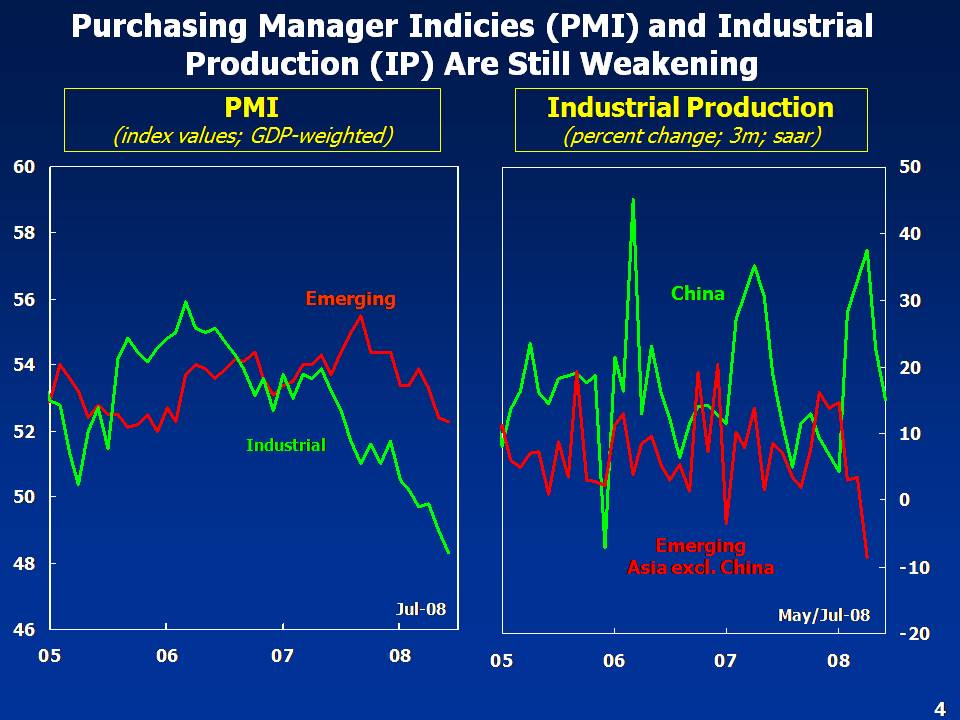

Going forward, growth momentum is likely to lose some steam in emerging economies, but the degree of deceleration would differ across regions. Signs of deceleration are most pronounced for several Emerging Asian economies that are tightly linked to the global manufacturing cycle, including the Philippines, Thailand, Malaysia, Taiwan PoC, Singapore, Hong Kong SAR, and—to a lesser extent—India. Headwinds to activity have also intensified for Emerging Europe and Latin America, owing to these regions' exposure to the euro area and the United States through trade and financial channels. Overall on a fourth-quarter-on-fourth-quarter basis, growth in emerging and developing economies is projected to ease from over 8 percent in 2007 to just over 6 percent in 2008, before reaccelerating to more than 7 percent in 2009.

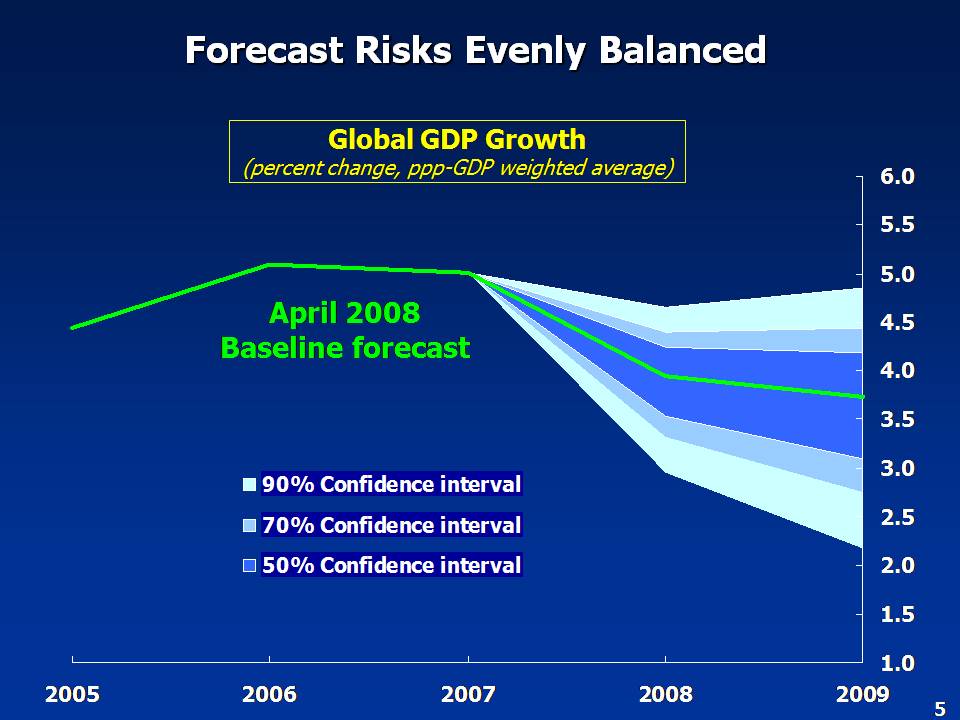

The global economy is projected to slow further in the second half of 2008, with a recovery gaining pace gradually in 2009. Global GDP growth would slow from 5 percent in 2007 to about 3 percent late in 2008 and reaccelerate toward 4 percent in the course of 2009. The specific figures are still under review and will be released in our World Economic Outlook next month. The recovery of global economic activity in 2009 would be driven by the unwinding of the effects of the more than 50 percent increase in oil prices in 2008 and the bottoming out of the U.S. housing sector. This would be supported by continued robust domestic demand in many emerging economies, which have benefited from rapid integration with the global economy and have been affected to a much smaller extent by the financial turmoil.

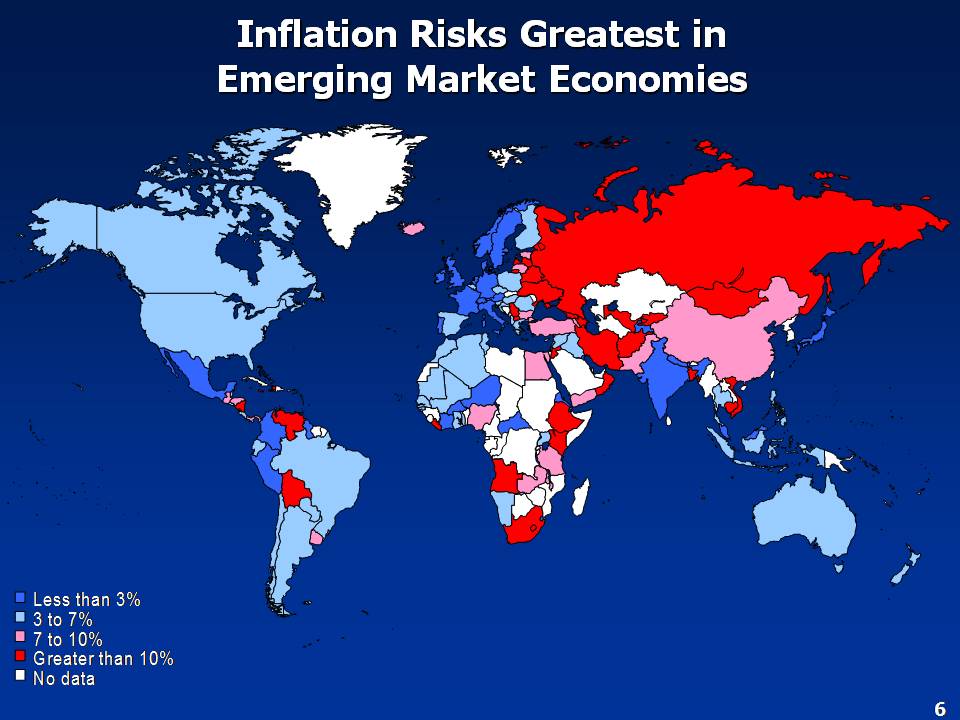

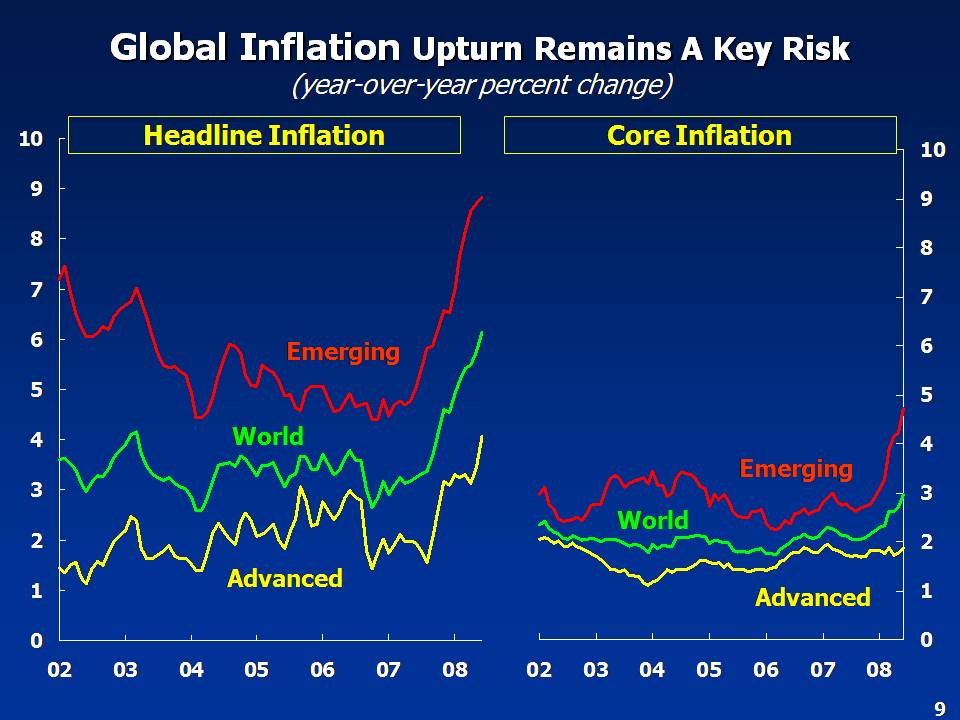

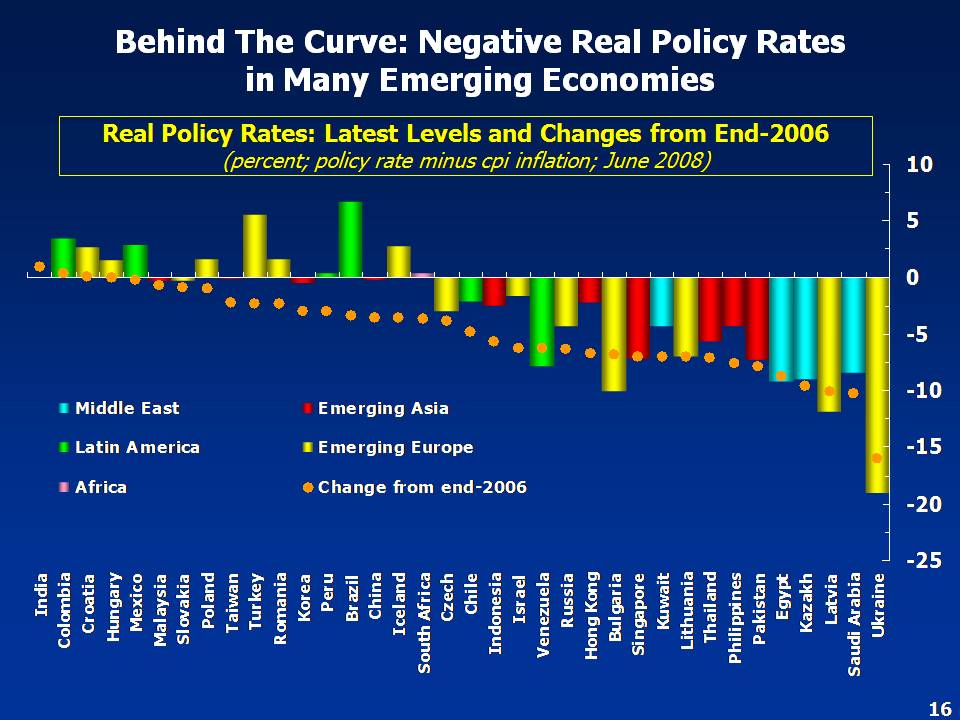

Notwithstanding slowing activity, headline inflation around the world has risen to its highest rate since the late 1990s, propelled by the surge in key commodity prices. In the advanced economies, headline inflation rose to around 4½ percent in July, underpinned by the rise in oil prices. The resurgence in inflation has gone much further in the emerging and developing countries where it rose to 9 percent in the aggregate in July, led largely by food price increases, with a wide swathe of countries experiencing double-digit inflation [shown in red in the map]. The recent declines in commodities prices may provide some respite, but nevertheless some increases still remain in the pipeline, since changes in international prices feed into local prices only with a lag.

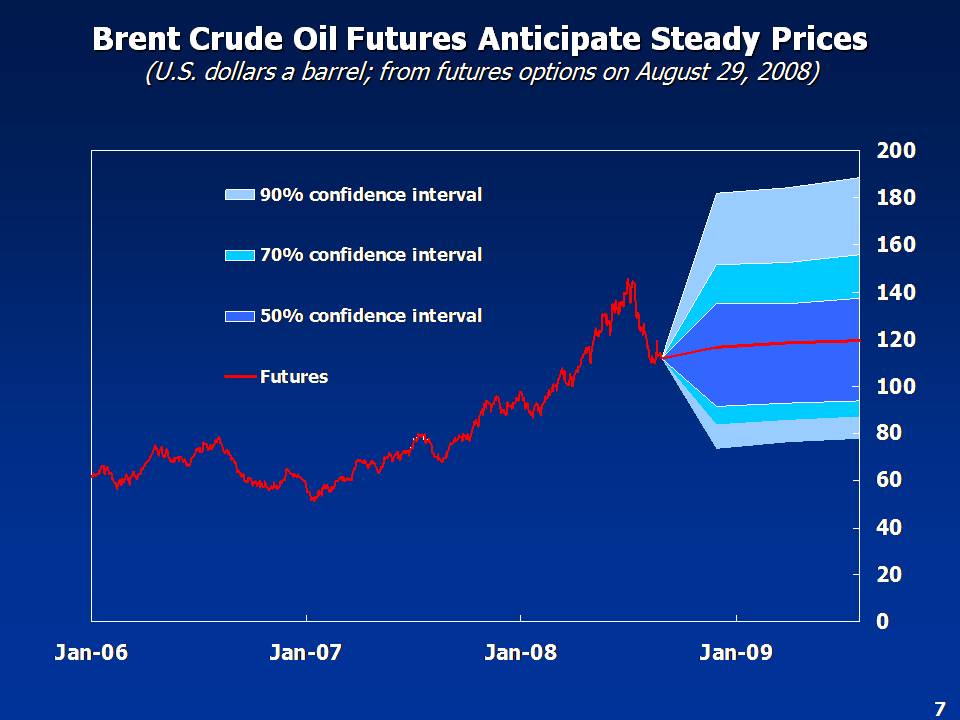

Oil prices have moderated recently, but they are still about 15 percent higher, on average, than at the beginning of 2008. In our view, high oil prices have largely reflected fundamental factors. Sustained strong demand growth—fueled by the acceleration of resource—intensive growth in emerging economies—a sluggish supply response, and declining inventories all contributed to the surge in prices. With weaker global growth and some demand response to higher oil prices, tight market balances between supply and demand in oil markets have eased some, allowing oil prices to recede from their peak.

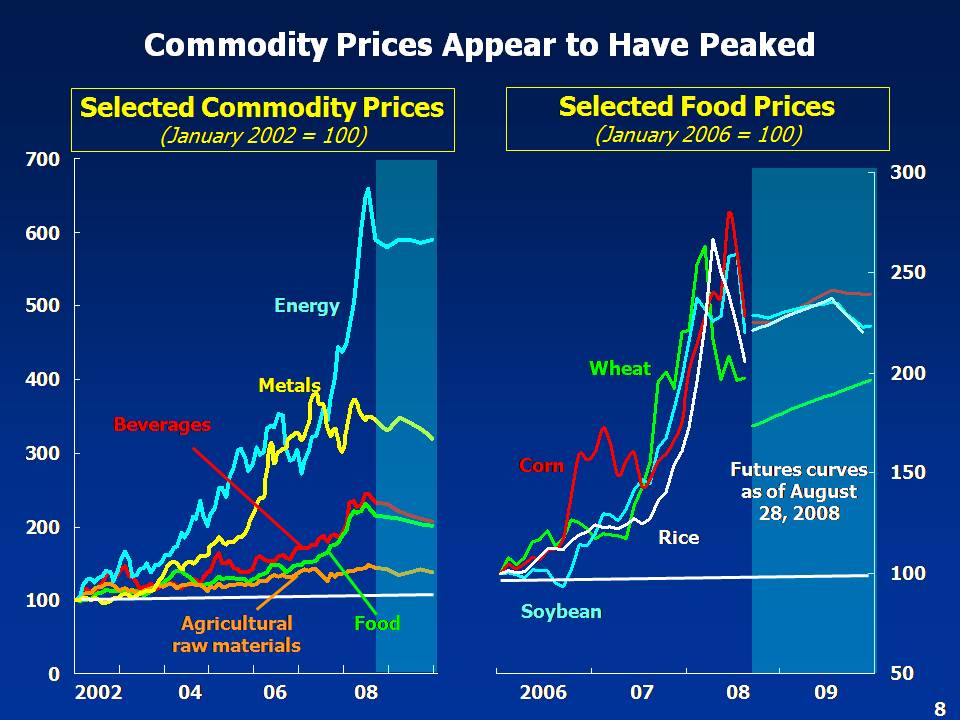

Similarly, prices of major food commodities rose by almost 70 percent in the year to June 2008, but have moderated more recently. Looking ahead, we see commodity prices likely to stay at much higher levels than previously in real terms and highly sensitive to views about demand and supply trends. As for "speculation", we have found little hard evidence thus far that this has been a driving factor, although it is quite possible that investor behavior can amplify short-term price fluctuations, and we will continue to examine the issue.

Core inflation in advanced economies has remained broadly contained, but has increased markedly in emerging economies. While the recent moderation of international commodity prices may ease some of the pressure, inflation risks in emerging economies remain serious since they are more vulnerable to second-round effects because of the greater weight of food in the consumption basket—typically in the range of 30-45 percent as opposed to 10-15 percent in the advanced economies—because inflation expectations are less well anchored by central bank credibility, and because fast growth has eroded margins of spare capacity.

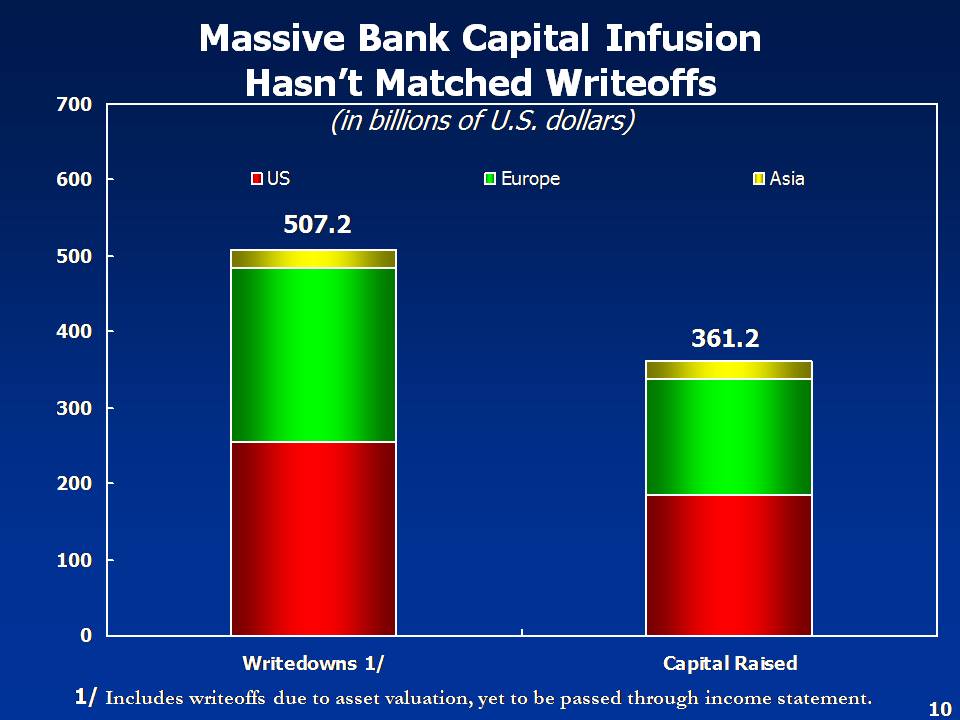

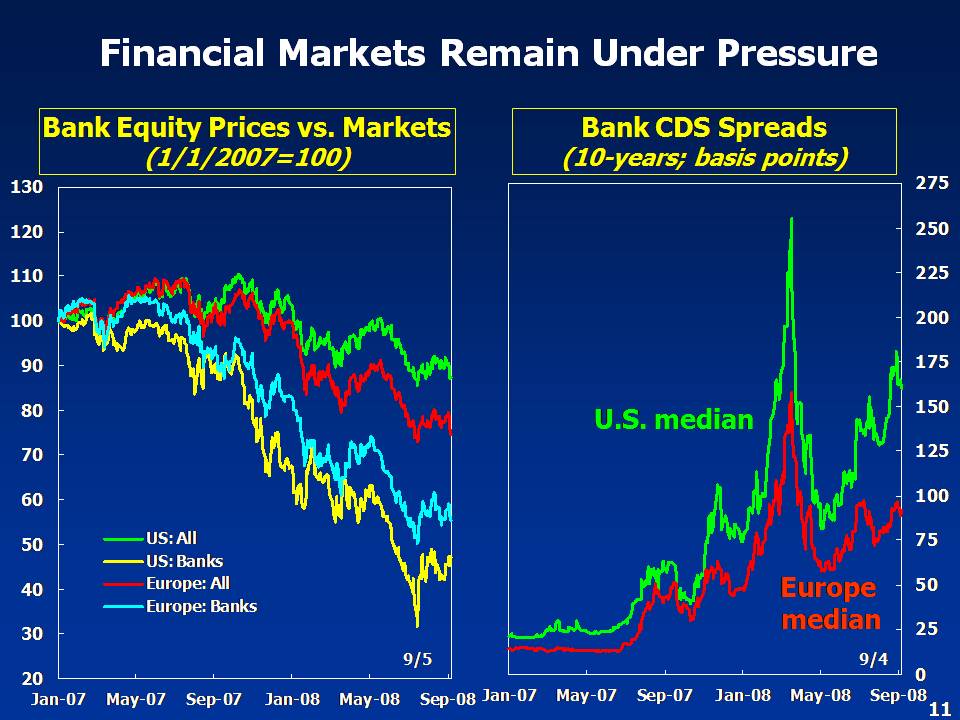

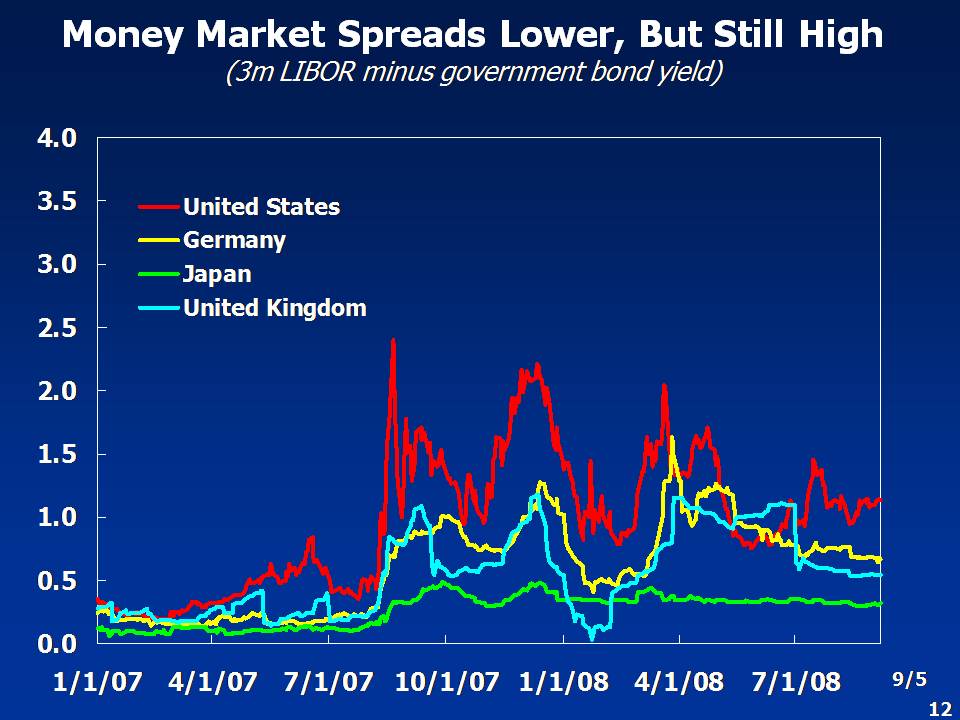

Global Financial Strains

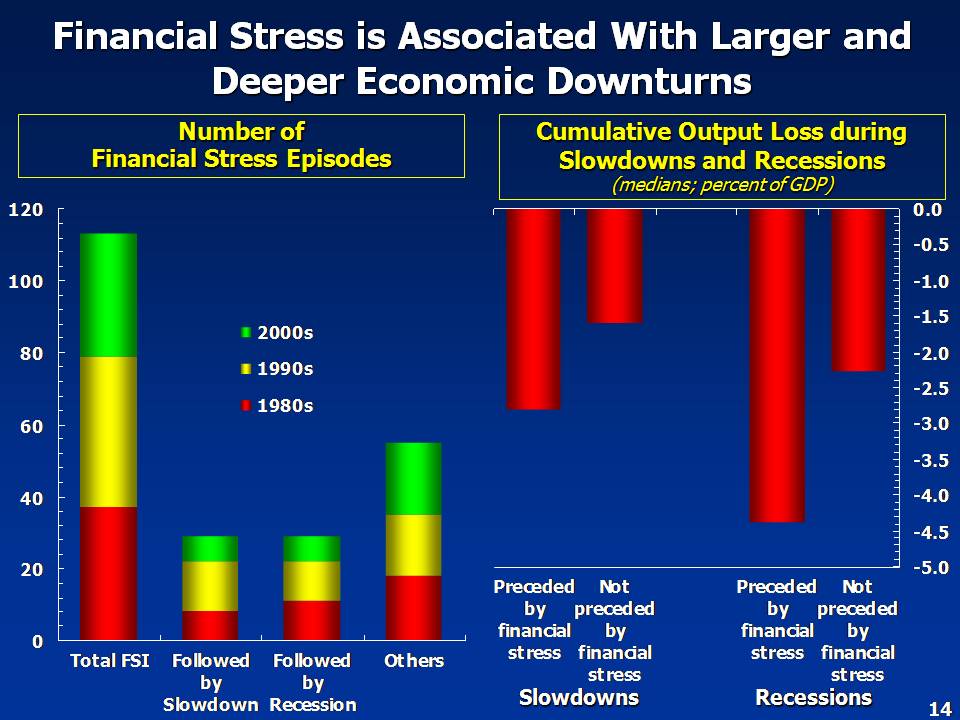

Let me now turn to financial markets in more detail. Risks in financial markets remain elevated and strains remain significant more than a year after signs of liquidity pressures first surfaced. Against this background, continued deleveraging in the financial sector is likely to act as a substantial constraint on the strength of the global economic recovery.

Policies

Many would conclude from the picture that I have just portrayed—slowing global growth, protracted financial strains, and higher inflation—that I am quite pessimistic about the immediate future. But I am not. The reason is that, in my view, there are positive aspects of the current situation that point toward recovery. Moreover, sound policy options are on offer to effectively address many of the tough problems that we face, but policy makers will need to avail themselves of that opportunity and take the right steps.

| Public Affairs | Media Relations | |||

|---|---|---|---|---|

| E-mail: | publicaffairs@imf.org | E-mail: | media@imf.org | |

| Fax: | 202-623-6220 | Phone: | 202-623-7100 | |