Role of trade

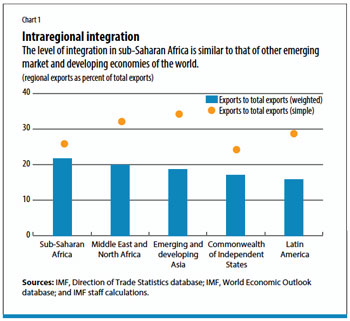

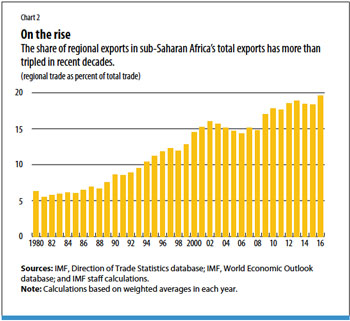

Integration across sub-Saharan Africa has been most notable through trade, steadily increasing in intensity over time: since the 1980s the share of regional exports in total exports has more than tripled (see Chart 2). Sub-Saharan Africa now has the highest share of intraregional trade integration among the world’s emerging market and developing economies, followed by the Middle East and North Africa and emerging and developing Asia.

This rising integration in recent decades is the result of the region’s higher economic growth relative to that of the world, its tariff reductions, and the strengthening of its institutions and policies. Although the direction has been favorable over time, compared with advanced economies, intraregional trade nonetheless remains relatively low, and the business environment continues to be challenging.

Growth has supported sub-Saharan Africa’s increasing integration, but the integration itself has also translated into important growth spillovers: our work finds that on average a 5 percentage point increase in the export-weighted growth rate of intraregional partners is associated with about a 0.5 percent increase in the growth of a typical sub-Saharan African country. Interestingly, and consistent with the region’s comparable shares of intraregional trade, trade channel spillovers seem to be similar to those of other emerging market and developing economies.

There are important caveats when it comes to optimism about sub-Saharan African integration, though—most of which indicate that the continent still has a long way to go to reach full integration.

Today, the bulk of intraregional trade is highly concentrated. Ten sub-Saharan countries represent 65 percent of total regional demand for intraregional exports, and as the destination market for most of the intraregional trade they have the potential to generate the largest regional spillovers. These include large economies such as South Africa and its neighboring countries, Côte d’Ivoire and the Democratic Republic of the Congo, but surprisingly exclude others, such as Angola and Nigeria, which mostly import from the rest of the world.

Throughout the continent there are other small pockets of intensive intraregional integration, though the import shares are relatively small compared with those of the big players and with total sub-Saharan African intraregional exports. Countries with intensive intraregional integration tend to be smaller and to import significant shares of their neighbors’ GDP, and can thus be a substantial source of spillovers at the subregional level. This is particularly true in the case of west African countries such as Burkina Faso, Ghana, and Mali, which are large destination markets for exports worth more than 1 percent of GDP for some of their trading partners.

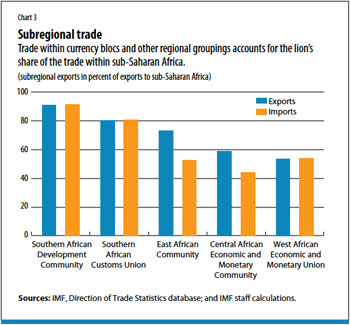

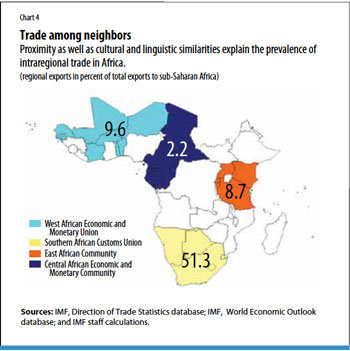

A closer look at the geographic distribution of trade in sub-Saharan Africa reveals significant subregional concentration. Trade within the Southern African Customs Union (SACU) alone represents half of total sub-Saharan African intraregional trade. Moreover, for the Southern African Development Community (SADC), the East African Community (EAC), and the SACU, trade within these regions represents more than 70 percent of their member countries’ intraregional trade. In the Central African Economic and Monetary Community (CEMAC) and the West African Economic and Monetary Union (WAEMU) regions, trade within the regions represents around 50 percent of their intraregional trade (see Chart 3). In absolute terms, the SADC and SACU account for more than 70 percent and 50 percent of total sub-Saharan African trade, respectively (see Chart 4).

The prevalence of trade among neighbors in sub-Saharan Africa is explained by the fact that bilateral trade is hindered by distance and sociocultural differences—that is, trade becomes increasingly difficult the greater the distance from a country’s subregion. In fact, although this is a global phenomenon, these barriers are even more pervasive in sub-Saharan Africa than in the rest of the world. Not surprisingly, then, the rise in trade among neighbors has been a significant driver of trade growth in the region. About half of the 1980–2016 growth in regional trade stems from this type of trade integration—a result that is particularly strong in the EAC and SADC.

The overall pattern of integration reflects not only geographic proximity, but also infrastructure constraints and the impact of regional trade agreements and lower nontariff barriers within subregions. Given that it is underdeveloped, trade between subregions holds the greatest potential for further integration. In this regard, the African Continental Free Trade Agreement, signed by countries from across the continent, could kickstart a new wave of even deeper integration.

There is another significant reason for the intraregional integration in sub-Saharan Africa: natural resource endowment. It turns out that the weight of a country’s exhaustible natural resources in the economy strongly affects its trading patterns.

Non-resource-intensive countries are highly exposed to regional demand: intraregional exports account for 7 percent of GDP, or 30 percent of total exports, on average. Non-oil-resource-intensive countries exhibit similar patterns, but to a slightly lesser degree.

Oil exporters, on the other hand, are different. And the difference is dramatic—exports from oil-producing countries to the rest of the world average 25 percent of GDP, while intraregional exports represent only 1.5 percent. These countries are thus sheltered from regional spillovers but are more exposed to global spillovers.