Pipeline running through Okrika community near Nigeria's oil hub city of Port Harcourt.

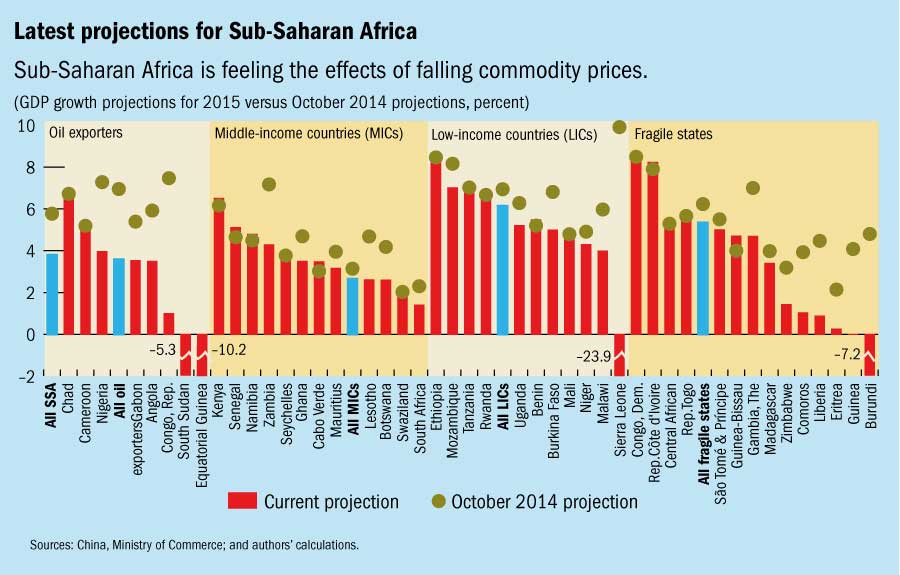

Falling oil prices have reduced export revenue for sub-Saharan Africa’s oil

producers, which account for about half of region’s GDP (Akintunde Akinleye/Reuters/Corbis)

REGIONAL ECONOMIC OUTLOOK

While the business and macroeconomic environment has improved considerably over

the past decade or so, other factors that underpinned strong growth—particularly

high commodity prices and accommodative financing conditions—have become less

supportive. The prices of many commodities exported by the region have fallen by

around 40-60 percent in the past two years, and borrowing costs have risen amid

a reassessment of global risk in anticipation of a U.S. interest rate hike. In addition,

larger external and fiscal deficits weigh on some countries.

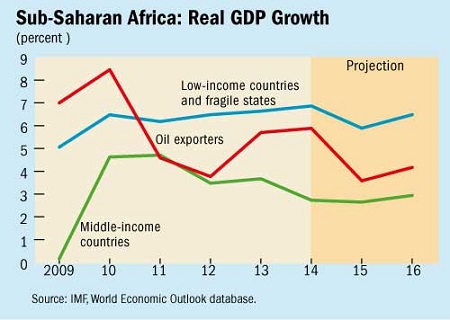

As a result, while growth in sub-Saharan Africa is still stronger than many other

regions, the IMF’s latest Regional Economic Outlook for Sub-Saharan Africa puts

growth at 3¾ percent this year, even lower than in 2009 in the aftermath

of the global financial crisis. The forecast for 2016 is slightly higher at 4¼

percent.

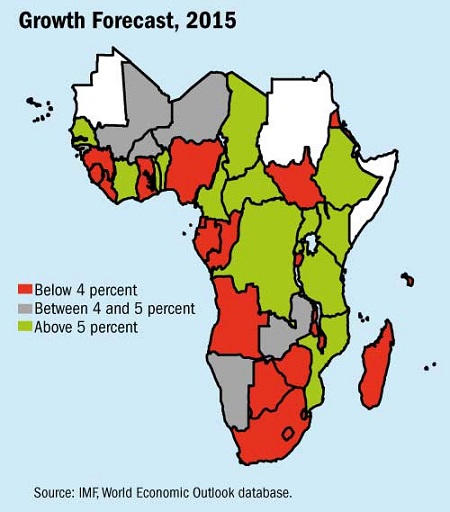

Variation across region

But despite the difficult overall picture, the report finds that there is considerable

variation across the region (see charts below). In most low-income countries, growth

is generally holding up, supported by infrastructure investment and private consumption.

Countries such as Cote d’Ivoire, Ethiopia, and Tanzania are expected to grow

at 7 percent or more this year and next. Other low-income countries, however are

feeling the pinch from commodity prices, even though cheaper oil has eased their

energy import bill.

Hardest hit are the region’s oil exporters as falling oil prices have drastically

reduced export revenue and forced a sharp fiscal adjustment. The oil producers account

for about half of the region’s GDP and include the largest producers, Nigeria

and Angola. Several middle-income countries, including Ghana, South Africa, and

Zambia, are also facing unfavorable conditions, ranging from weak commodity prices

to difficult financing conditions and electricity shortages.

Limited scope to counter drag on growth

Savings have been modest during the recent period of rapid growth, leaving limited

room to counter the drag on activity in the region or smooth the adjustment to the

recent shocks. Many countries now have weaker fiscal and external balances than

at the onset of the global financial crisis in 2008. And while in many cases this

situation reflects countries’ efforts to address large infrastructure needs,

it leaves them with fewer resources to contain the effects of the current downturn.

For oil exporters in particular, fiscal adjustment is unavoidable in the face of

a sharp and seemingly durable decline in oil prices. Fiscal policy in most other

countries needs to balance development needs and debt sustainability, which will

become increasingly difficult as higher interest rates and lower growth adds to

debt burdens.

On the monetary policy front, wherever the terms of trade have worsened sharply

and the currency is not pegged, the study recommends that exchange rate should be

allowed to depreciate to absorb part of the shock. Exchange rates have also come

under pressure in countries where commodity exports do not play such a large role.

Given the strong global forces behind these pressures, intervening here, too, would

risk depleting scarce foreign exchange reserves. Accordingly, central bank intervention

should focus on containing disorderly exchange rate movements. Monetary policy should

respond only to second-round effects of exchange rate depreciations on prices and

to other upward shocks to inflation.

Improving competitiveness, reducing inequality spurs growth

Beyond these more immediate challenges, the Regional Economic Outlook also

discusses, in two background studies, how longer-term growth in the region can be

supported by efforts to improve competitiveness and reduce inequality.

The first study suggests that the region’s recent period of high growth and

substantial trade integration, has also been accompanied by a widening of trade

imbalances and a weakening of competitiveness, especially among commodity exporters.

With some of the past sources of growth dissipating, the region needs to nurture

new sources by increasing the sophistication of its exports and integrating into

global value chains, which will only happen with greater competitiveness. The policy

actions to achieve this objective depend on specific country circumstances, but

progress can be facilitated by pursuing sound macroeconomic policies, investing

in infrastructure while keeping debt on a sustainable path, continuing to eliminate

trade barriers, and improving the business climate.

The second study considers the implications for sub-Saharan Africa of persistently

high income and gender inequality. The region has among the highest levels of inequality

in the world. With growing international evidence suggesting that persistent inequality

can impede macroeconomic stability, the study finds that policies aimed at reducing

inequalities to levels seen in some fast growing emerging Asian countries (for example

by expanding access to education and health care) could potentially increase growth

by one percentage point annually in sub-Saharan Africa. Carefully designed fiscal

and financial sector policies and the removal of gender-based legal restrictions

could also reduce inequality and improve long-term growth in the region, the study

says.