Typical street scene in Santa Ana, El Salvador. (Photo: iStock)

IMF Survey : Growth Slows in Emerging Markets, Picks Up in Advanced Economies

July 9, 2015

- Global growth forecast at 3.3 percent this year and 3.8 percent in 2016

- Improving recovery in advanced economies; slowdown in emerging markets

- Risks of financial market volatility persist

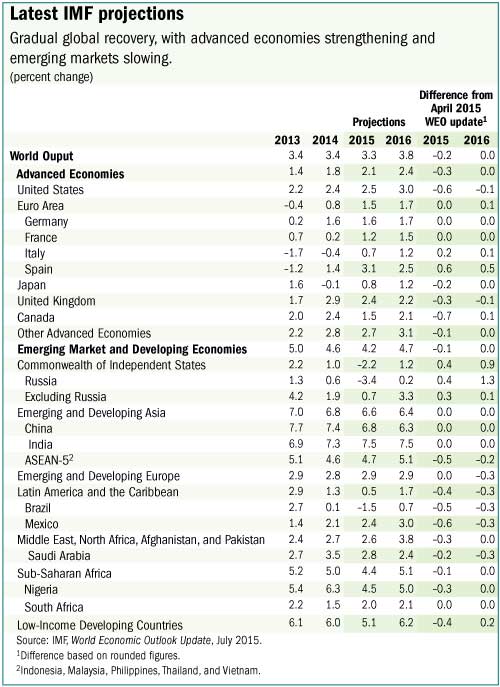

Moderate growth continues, with global growth forecast to be slightly down for 2015, reflecting an unexpected setback to economic activity in the first quarter of 2015, mostly in North America, says the IMF’s latest update on the World Economic Outlook.

A ship loaded with soybeans at Port of Santos, Brazil. Lower commodity prices are dampening growth in Latin America (photo: Paulo Whitaker/ Reuters / Corbis)

WORLD ECONOMIC OUTLOOK UPDATE

General evolutions are unfolding very much as forecast in April, said Olivier Blanchard, IMF Economic Counselor and Director of Research, “namely, an improving recovery in advanced economies and a slowdown in underlying growth in emerging markets and developing economies.” Forecasts for the world economy are for 3.3 percent this year, marginally lower than in 2014, and 3.8 percent next year (see table).

“As dramatic as the events in Greece are,” Blanchard said, “effects on the rest of the world economy from the further suffering of the Greek economy are likely to be limited.” Of course, he said, “we continue to hope for and work toward a positive solution by which Greece remains in the Eurozone.”

As for other developments, the WEO Update says that oil prices rebounded during the second quarter of 2015, the risk of deflation decreased, and financial conditions for corporate and household borrowers in most advanced economies remained broadly favorable.

Advanced economies are improving

The increase in global growth in 2015 will be driven by stronger growth in advanced economies. Growth in these economies is forecast to increase from 1.8 percent in 2014 to 2.1 percent in 2015 (falling about 0.3 percentage points short of the forecast in April), and 2.4 percent in 2016. The report notes that the unexpected weakness in North America in early 2015, which accounts for most of the growth forecast revision for 2015, will likely prove to be a temporary setback. The underlying drivers for consumption and investment in the United States—wage growth, labor market conditions, easy financial conditions, lower fuel prices, and a strengthening housing market—remain intact.

The economic recovery in the euro area is more solidly anchored, with signs of increase in both domestic demand and inflation. Growth projections were revised up for many euro area economies (e.g., Spain, Italy), but in Greece, unfolding developments are likely to take a much heavier toll on activity relative to previous expectations.

Japan saw a stronger than expected growth in the first quarter of 2015, but much of the surprise reflected inventory accumulation. With weaker underlying momentum in real wages and consumption, the pickup in growth in 2015 is now projected to be more modest.

Emerging and developing economies are slowing

Growth in emerging market and developing economies is projected to slow from 4.6 percent in 2014 to 4.2 percent in 2015. The slowdown reflects the dampening impact of lower commodity prices and tighter external financial conditions—particularly in Latin America (e.g., Brazil) and oil exporters.

Other factors include rebalancing in China, structural bottlenecks, and economic distress related to geopolitical factors—particularly in the Commonwealth of Independent States and some countries in the Middle East and North Africa.

In 2016, growth in emerging market and developing economies is expected to pick up to 4.7 percent, largely on account of the projected improvement in economic conditions in a number of distressed economies, including Russia and some economies in the Middle East and North Africa.

Risks to the outlook

Given the distribution of risks to the near-term outlook, global growth is more likely to fall short of expectations than to surprise on the upside. The boost from lower oil prices, especially in advanced economies, however, may still offer potential gains.

Developments in Greece have, so far, not produced strong ripples. And while timely policy action should help in managing potential contagion, some risks of a reemergence of financial stress remain.

More generally, disruptive shifts in asset prices and increased financial market volatility remain important risks, also because of the associated risks of capital flow reversals in emerging market economies. Furthermore, U.S. dollar appreciation poses balance sheet and funding risks for dollar debtors, especially in some emerging market economies.

Other risks include low medium-term growth or a slow return to full employment amid very low inflation and crisis legacies in advanced economies, a sharper-than-expected slowdown in China, and spillovers to economic activity from increased geopolitical tensions in Ukraine, the Middle East, or parts of Africa.

Preventing the low growth trap

In this setting, without the expected pickup in global growth, the IMF emphasizes that the economic policy priority must remain raising actual and potential output through a combination of demand support and structural reforms.

In many advanced economies, this means that accommodative monetary policy should continue to support economic activity and lift inflation back to target. There is also a strong case for increasing infrastructure investment in some economies and for implementing structural reforms—such as labor market reforms (to reduce youth unemployment for example) and product market reforms (such as removing barriers to entry) to tackle legacies of the crisis and boost potential output.

In many emerging market and developing economies fiscal policy can be a tool to boost demand and longer-run growth through tax reform and prioritizing spending. Structural reforms to raise productivity and remove bottlenecks to production are urgently needed in many economies.