Key findings

This new data set allows us, for the first time, to examine the historical

evolution of uncertainty around the globe. Several interesting stylized

facts emerge:

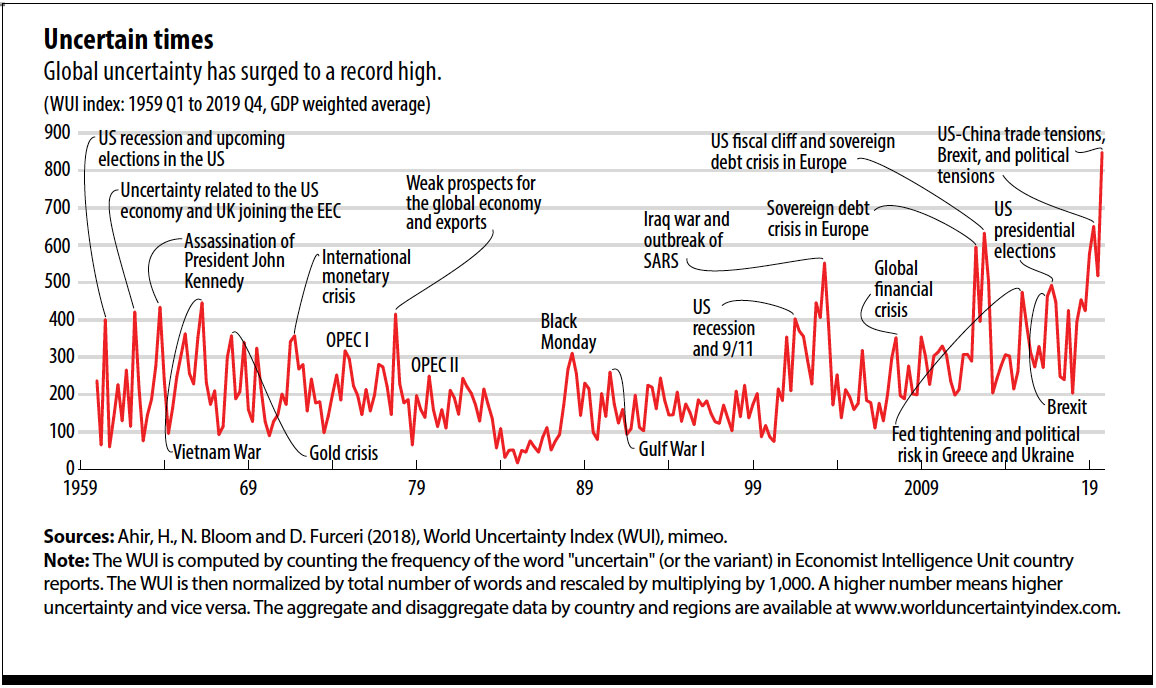

First, global uncertainty has increased significantly since 2012.

The latest data for the fourth quarter of 2019 show that, after dipping in

the third quarter of 2019, the aggregate index—a GDP-weighted average of

143 countries—is at an all-time high.

The recent levels of global uncertainty are also exceptional in a

historical context. Looking back at the past 60 years, we see few episodes

in which uncertainty has been at levels close to those observed in the past

decade. Other notable historical episodes include the assassination of US

President John F. Kennedy, the Vietnam War, the gold crisis in the late

1960s and the oil crises in the 1970s.

These global episodes, however, do not mean that levels of uncertainty are

historically high for all countries in the world. They reflect, to a large

extent, the increasing role of global factors in driving uncertainty across

the globe. For example, the current level of uncertainty in China is

significantly lower than the level recorded during the cultural revolution

in the late 1960s, a period when China was less connected to the rest of

the world.

Second, uncertainty spikes are more synchronized in advanced economies

than in emerging market and low-income economies.

Our analysis finds that uncertainty in emerging market and low-income

economies mostly follows the global average. This is because individual

country shocks are not synchronized, so they get averaged away. In

contrast, uncertainty in advanced economies spikes sharply, because these

countries tend to move together. Within advanced economies, uncertainty

synchronization is higher among euro area countries. In addition, we find

that stronger trade and financial linkages across countries lead to

stronger uncertainty synchronization.

Third, the average level of uncertainty is higher in low-income

economies than in emerging market and advanced economies.

One potential reason for this is that developing countries appear to have

more domestic political shocks like coups, revolutions, and wars; are more

susceptible to natural disasters like epidemics and floods; and their

economies are more volatile as they are more frequently hit by external

shocks and have more limited capacity to manage these shocks.

Fourth, there is an inverted U-shaped relationship between uncertainty

and democracy.

As countries move from a regime of autocracy and anocracy toward democracy,

uncertainty increases. As countries move from some degree of democracy to

full democracy, uncertainty declines.

Finally, increases in the index foreshadow significant output declines,

with the effect being larger in countries with weaker institutions.