Over the past decade, the implications of recent technological innovations

for future growth have become a subject of lively debate. Some claim that,

in the coming decades, the global economy will enjoy a surge in economic

growth driven by improvements in productivity thanks to new technologies

(Brynjolfsson and McAfee 2014; Mokyr 2018). Others caution that future

growth could stall, or even decline, because new technologies will likely

have a diminishing marginal impact on productivity and structural

challenges associated with aging and sluggish investment growth will cast a

pall on prospects (Gordon 2016).

It is difficult, if not impossible, to undertake a credible quantitative

analysis of the aggregate impact of new technologies on growth prospects.

However, long-term growth forecasts could provide a small window into this

debate. These forecasts could be expected to improve over time as new

technologies, such as machine learning, cloud computing, robotics, and

smartphones, spread. But is this borne out by the data? In our study, we

examine how long-range forecasts have evolved during a period of rapid

technological change in order to gauge what this might mean for future

growth (Kose, Ohnsorge, and Sugawara, forthcoming).

Our analysis is based on forecasts published by Consensus Economics, a firm

that surveys professional forecasters several times a year to generate its

long-term annual growth projections—the average forecast for 6–10 years

ahead. Forecasts by Consensus Economics reflect the perspectives of many

institutions that use a wide range of methodologies, so they tend to stand

up to potential uncertainty better than projections produced by a single

entity. Our sample includes long-term forecasts over 1998–2018 for 20

advanced economies and 18 emerging market and developing economies that

constitute roughly 90 percent of global GDP.

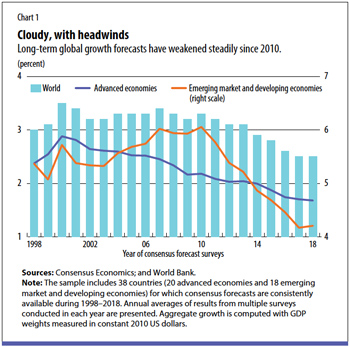

Increasingly pessimistic

Following the global financial crisis, long-term forecasts were steadily

downgraded. The global economy was projected in 2010 to grow at 3.3 percent

in 2020. By 2018, the long-term growth forecast had been reduced to 2.5

percent (see Chart 1). Long-term forecasts were downgraded for all

countries by an average 1.4 percentage points between 2007 and 2018. One

quick interpretation of these increasingly pessimistic expectations is that

forecasters hold a dim view of the opportunities offered by new

technologies for the next decade.

The global financial crisis marked a turning point in long-term global

growth expectations. Between 1998 and 2007, the average long-term forecast

rose from 3 percent to 3.4 percent and increased in almost half of the

economies studied. Emerging market and developing economies, in particular,

enjoyed improving growth prospects before the crisis, but advanced

economies’ forecasts were already being downgraded in the early 1990s.

After a brief period of upgrades in the late 1990s, long-term forecasts for

advanced economies resumed their gradual decline in the early 2000s. Since

the 2008–09 crisis, these forecasts have materially deteriorated for both

groups of countries. The postcrisis weakness in long-term growth

expectations is also evident, albeit at different speeds and intensities,

among alternative measures of activity, including growth rates of per

capita income, investment, and consumption.

The pattern of precrisis upgrades and postcrisis downgrades in long-term

forecasts is broadly shared by many large economies. For example, in 1998,

US growth was expected to be about 2.4 percent in 2008. But by 2008,

long-term growth forecasts had been revised upward by 0.3 percentage point.

Similarly, in 1998 growth in China was expected to be 7.5 percent over the

following decade, and by 2008, the long-term forecast had been raised 0.2

percentage point following the economy’s remarkably strong performance in

the previous decade. Although long-term forecasts for Brazil and India were

upgraded in 2008 relative to expectations a decade earlier, these upgrades

did not last. By 2018, these economies’ long-term growth forecasts had all

declined 0.3–2.4 percentage points below 1998 levels.

Roller-coaster ride

The evolution of long-term forecasts reflects the global economy’s

roller-coaster ride over the past two decades. Precrisis strength in growth

prospects coincided with unprecedented expansion of global trade and

financial flows, along with rapid growth in some major emerging market and

developing economies. During 2003–07, the global economy registered one of

its best growth records since the early 1970s. Tailwinds, however, turned

into headwinds during the 2009 global recession, which was followed by an

anemic recovery, especially in advanced economies. Over 2010–15, long-term

prospects were further impeded by the 2011–12 euro area debt crisis and by

a sharp slowdown in emerging market and developing economies, attributable

in part to a downturn in commodity prices.

The softening of long-term growth forecasts also reflects structural forces

associated with demographic changes, investment prospects, and productivity

trends. These forces have already been eroding global potential growth—the growth rate of the global economy at

full capacity and full employment. During 2013–17, global potential growth

was already roughly 1 percentage point lower than a decade earlier, as a

result of weak productivity growth, sluggish expansion of investment, and a

broadening slowdown in working-age-population growth.

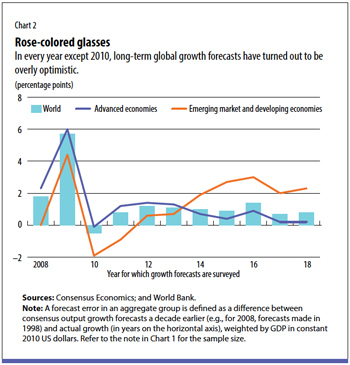

Long-term global growth forecasts made a decade earlier exceeded actual

outcomes in every year of the 2008–18 period except 2010 (see Chart 2). The

same was true for the majority of individual country forecasts. And even in

2010, forecasts were overly optimistic for about half of advanced economies

and a quarter of other economies.

The analysis here covers mainly the crisis and postcrisis periods that

witnessed an unusual series of negative growth shocks, but the optimism

bias of forecasts has been widely documented. Time and again, growth

forecasts have proved overly optimistic relative to outcomes (Ho and Mauro

2015). Moreover, the degree of optimism tends to increase as the time

horizon gets longer. On average, long-range forecasts overshot actual

growth by 1.2 percentage points, and three-year-ahead forecasts

overestimated growth by 0.7 percentage point over the period until 2018.

Since long-term growth expectations presumably abstract from cyclical

effects, they should reflect forecasters’ judgment about potential growth.

But do they? Long-term forecasts for global growth often exceed the

estimates of global potential growth over the decade that follows. These

observations suggest that long-term growth forecasts have remained

optimistic relative to eventual outcomes and potential growth estimates,

despite becoming more pessimistic during the postcrisis period.

Long-term forecasts tend to improve during periods of sustained strong

output growth. In other words, growth expectations generally rise if

productivity, employment, and investment growth increase for a prolonged

period.

Between hope and despondency

For now, forecasters appear to hold a cautious view of the growth boost

from new technologies over the next decade, more in line with the

technology pessimists than the technology optimists. Instead of a

technology-driven productivity boost, growth is expected to slide further.

This pessimism could reflect an awareness that weak productivity growth,

increasingly unfavorable demographic trends, and subdued investment

prospects are likely to weigh on global potential growth in the coming

years.

There could, of course, be other explanations for increasingly pessimistic

forecasts in an era of rapid technological change. First, forecasters may

benchmark their forecasts against recent low productivity growth—but this

indicator may be underestimated because of measurement error. Nobel

Prize–winning economist Robert Solow nicely summarized the issue of

measurement by saying, “You can see the computer age everywhere but in the

productivity statistics.”

Second, forecasters may be unable to project the impact of major

technological changes on productivity and output growth because these types

of changes, such as the mass use of electricity and cars, are rare and,

when they happen, their impact on aggregate growth and productivity is felt

only gradually. Moreover, a quantitative study of their implications for

growth prospects requires improvements in econometric tools and data that

are not available at the moment.

Both explanations attribute the decline largely to a lack of good

information.

A third explanation is less benign: structural headwinds from adverse

demographic trends, slowing investment growth, and stagnating productivity

as a result of existing widely used technologies may reduce growth

prospects to such an extent that even large productivity gains from new

technologies will not be able to deliver strong long-term growth. This

could mean that new technologies are still not mature enough to be widely

used for general business purposes, and that their diffusion requires long

and uncertain lags. It could also reflect obstacles to firms’ adoption of

new technologies, such as financing constraints and limited worker skills.

These explanations aside, if past performance is any guide, even these

increasingly pessimistic long-term forecasts may eventually turn out to be

optimistic as growth—yet again, as in the past two decades—disappoints. One

message is clear: a hopeful outlook about future global growth depends on a

significant pickup in measured productivity to offset the structural

impediments confronting the world economy.

Rapid technological change may eventually bring a new era of global

prosperity. However, rather than wait for that new era to arrive,

policymakers must act now with measures to enhance their economies’

potential growth. In the spirit of US President Dwight D. Eisenhower’s

dictum “Plans are worthless, but planning is everything,” governments

should prepare for the worst, even if the actual impact of new technologies

is still unknown. This implies an urgent need to press ahead with

initiatives to accelerate the realization of new technologies’ growth

benefits. These initiatives include raising investment in human capital and

expanding infrastructure investment to facilitate the use of new

technologies, as well as improving institutions and regulations to meet the

needs of technological change.