An older and a younger man sit in Tokyo’s Ginza district. By 2050 the number of aged dependents per worker will rise to about 75 percent, the highest of any country (photo: Friso Genrsch/picture alliance/Newscom)

Japan's Economic Outlook in Five Charts

November 28, 2018

Japan has had an extended period of strong economic growth. On the policy front, six years of “Abenomics” saw lower fiscal deficits, near-record unemployment, and higher female labor force participation. But inflation remains stubbornly low, and macroeconomic and financial sector challenges are set to grow as demographic headwinds—the aging and shrinking of Japan’s population—intensify.

Related Links

After a temporary soft patch earlier in the year, GDP growth is expected to remain above its estimated potential in 2018 at 1.1 percent. Inflation has gained momentum on the back of higher energy prices but—despite a very tight labor market—remains below the Bank of Japan’s (BoJ’s) 2 percent target. Financial conditions overall remain generally favorable.

Japan's parliament passed labor market legislation designed to set a legal cap on overtime work, ensure equal treatment for regular and nonregular workers, and exempt skilled professional workers from working-hour regulations, but the effectiveness of the new laws will hinge on implementation. Efforts to bring more workers into the labor force are meeting with success, with women, older workers, and inflows of foreign labor contributing to the gains. Corporate governance reforms have advanced, and the trade agenda has accelerated with two new trade agreements.

While economic growth is expected to remain solid, some downside risks exist. The planned consumption tax increase in 2019 could hinder near-term growth momentum. Weaker global growth and heightened uncertainty—from trade or geopolitical tensions—could also undermine growth, trigger yen appreciation and equity market shocks, and renew deflationary risks. The target date for a return to fiscal surplus was also reset from FY2020 to FY2025.

Below are five charts that shed light on Japan’s economic profile and policy priorities:

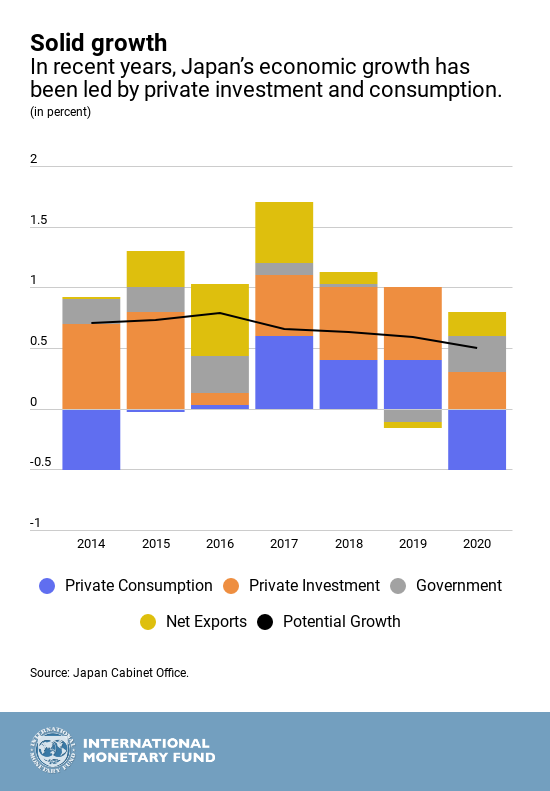

- Japan has experienced robust economic growth in recent years—driven by a mix of export growth, private investment, and consumption. As the external sector cools, however, GDP growth is expected to move back toward its long-run potential.

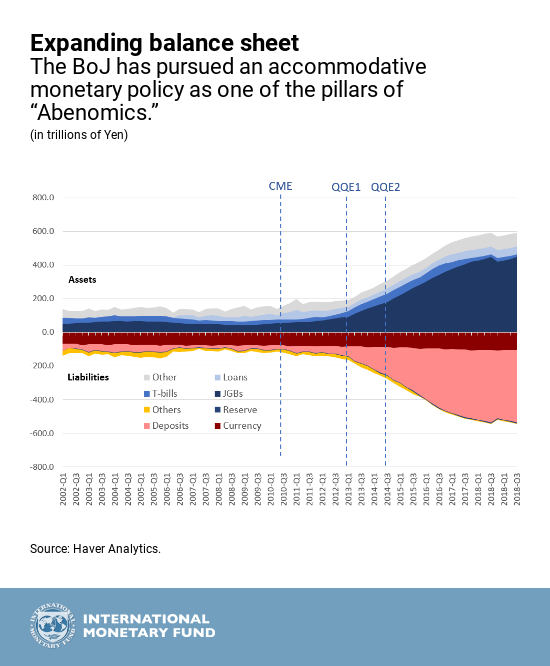

- The BoJ’s monetary policy includes a negative interest rate policy (for short-term rates), a yield curve control framework (targeting the 10-year Japanese Government Bond (JGB) yield at near zero), and a massive expansion of its balance sheet through purchases of JGBs, corporate bonds, real estate investment trusts, and exchange traded funds.

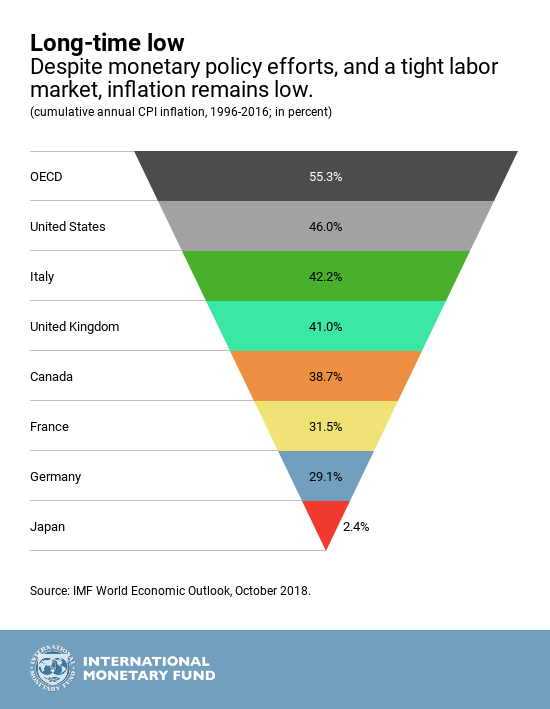

- Following a tax-induced spike in 2020, inflation will rise over the medium term, but likely remain below the BoJ’s 2 percent target. A part of the inflation inertia relates to Japan’s long experience with virtually no inflation, and that expectations of price increases in the future are closely linked to this lack of inflation experience.

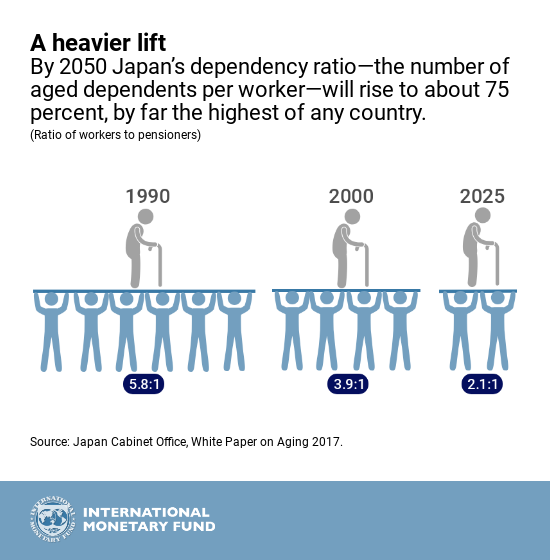

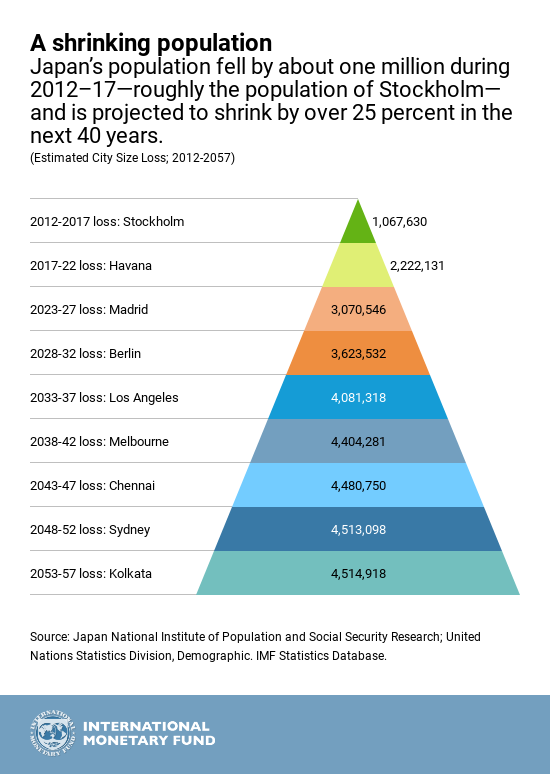

- The aging of Japan’s population and its shrinking workforce bring challenges. The Japanese population is also aging fast—over the next four decades the share of the population aged 65 years and older will rise from its current three-in-ten persons to almost four-in-ten persons. This will depress growth and productivity due to a shrinking and aging labor force and a shift toward consumption, while fiscal challenges will magnify with rising age-related government spending and a shrinking tax base.

- A solid plan for fiscal consolidation over the medium and long term is needed to address Japan’s demographic challenges and lessen debt sustainability risks. The planned increase in the consumption tax rate in 2019 will bring much-needed revenue. However, a concrete strategy is needed to stabilize and reduce the large public debt, over the medium and long-term—particularly given an aging population, labor force decline, and rising expenditures for healthcare and other social security programs.