Loading component...

Short-term Policy Responses to Geoeconomic Shocks in CESEE Countries

February 26, 2025

Loading component...

IMF Communications Department

MEDIA RELATIONS

PRESS OFFICER:

Phone: +1 202 623-7100Email: MEDIA@IMF.org

It is a great pleasure to open this session.

Let me begin by setting the stage for what I hope will be an insightful discussion on short-term policy responses to geoeconomic shocks. I will focus on the Central, Eastern, and South Eastern European (CESEE) countries.

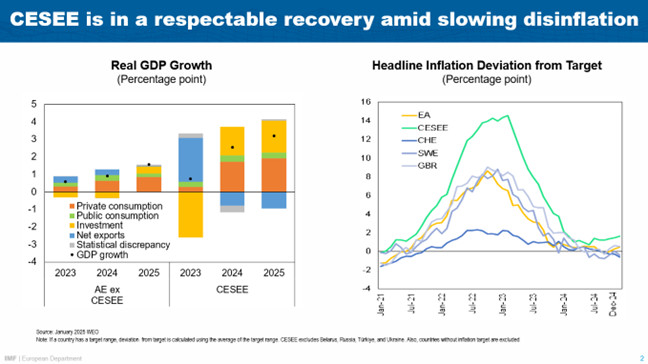

The CESEE region experienced a respectable recovery last year with growth accelerating from 0.8 percent in 2023 to 2.5 percent in 2024.

As expected, the composition of growth changed. Domestic demand (consumption and investment) rebounded, while net exports—which had been a key driver in 2023—turned into a drag.

Supportive fiscal policies at both the national and EU level played a role alongside a strong labor market and disinflation aided by tight monetary policy.

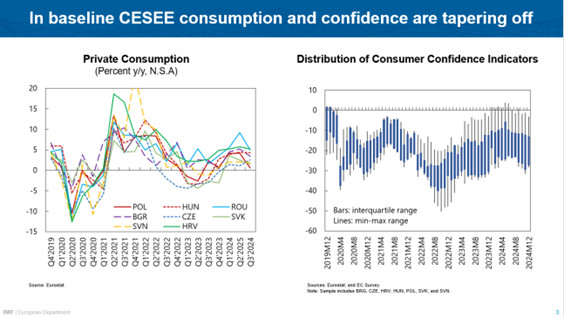

However, the growth momentum is weakening.

Geoeconomic fragmentation, linked to both Russia’s war in Ukraine and trade policy uncertainty, is weighing on demand.

In my remarks today, I will address three key questions:

Let me start with the first question.

How much can the CESEE region rely on domestic and external demand to support growth in 2025?

Our baseline forecast assumes moderate growth in 2025 at around 3 percent, supported by some remaining pent-up demand.

However, the cyclical recovery has largely run its course for three reasons.

Let me add two more observations:

Not all CESEE countries face the same challenges.

Albania, Croatia, Montenegro, Bosnia and Herzegovina, will continue to benefit from remittances, EU support, and tourism revenues, offering them some insulation from external risks.

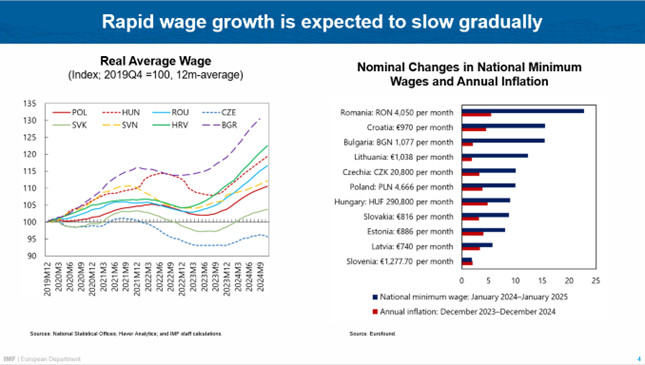

However, others will be impacted by the effects of the strong nominal wage growth over the last few years.

Taken together this means that with a few exceptions the region’s recovery momentum is weakening.

Let me now turn to the second question.

How well-prepared is the region to handle external demand challenges arising from geoeconomic fragmentation?

The region faces three key vulnerabilities in the face of geoeconomic fragmentation:

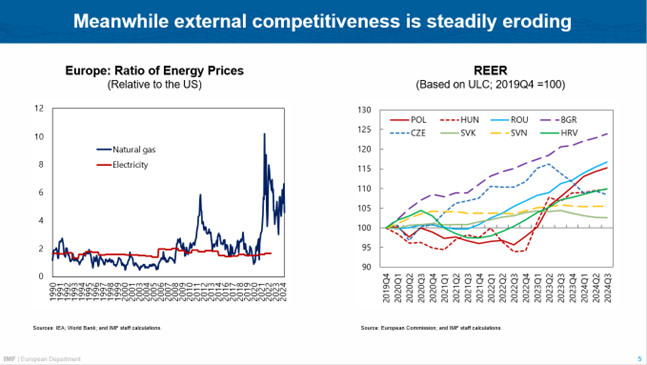

One, rising labor and high energy costs are eroding competitiveness.

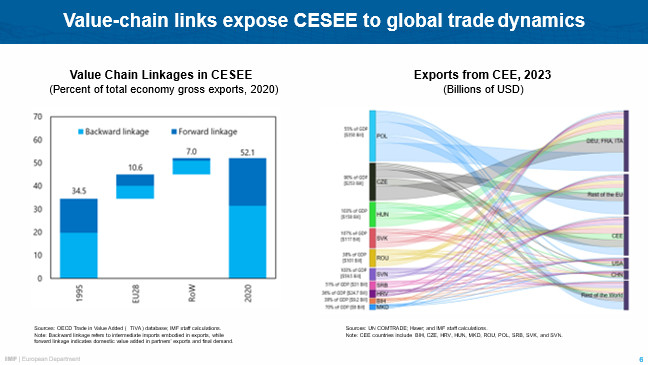

Two, high trade openness and deep integration into global value chains—once advantages during globalization—now heighten exposure to external demand shocks in times of de-globalization, and

Three, there is limited room from returning to accommodative macroeconomic policies.

Let me start with a word on cost competitiveness.

Export growth has stalled across the region with net exports subtracting about ½ percentage point from GDP growth last year.

Several adverse cost developments weigh now on CESEE’s competitiveness:

These cost pressures have significant economic implications. If the REER continues to appreciate by 2 percentage points per year, as observed over the past five years, export growth could be dampened by approximately 0.6-0.8 percentage points per year.

Beyond costs, the CESEE region’s integration into global value-chains and trade linkages create exposure to shifting trade dynamics.

A recent IMF study shows that Chinese EV imports could have very large GDP effects on CESEE countries through the supply chain.

For example, the estimated negative impact on Hungary and the Czech Republic from a shift to EVs is about 10 times larger than in advanced European economies, reducing GDP by 1.5 to 2.0 percent (cumulatively) over 5 years. For these countries and sectors to adjust, retaining cost competitiveness plays an important factor.

Now to the third question:

What can policymakers do in the short term?

After waves of external shocks, reducing uncertainty through clear communication is crucial. Governments should focus on reinforcing fundamentals, pursuing credible and sustainable macroeconomic policies, and building resilience.

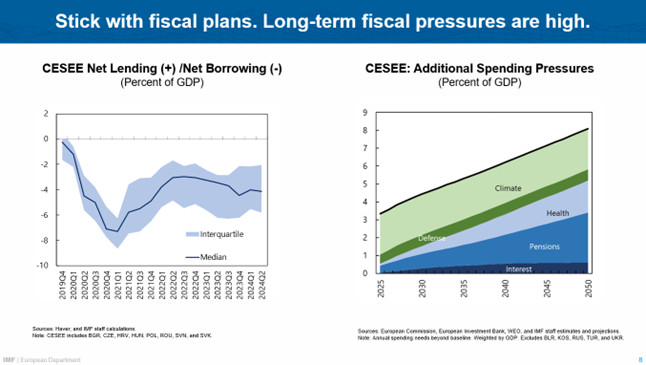

Fiscal consolidation is necessary, but it is not sufficient.

Despite the recovery, fiscal balances have not improved (LHS) and long-term fiscal spending needs remain high [RHS]. They are mostly aging-related (health and pensions), security related (defense) and climate-related.

An important discussion to be had is on the next EU budget, including on expenditures on European public goods, such as defense and the environment.

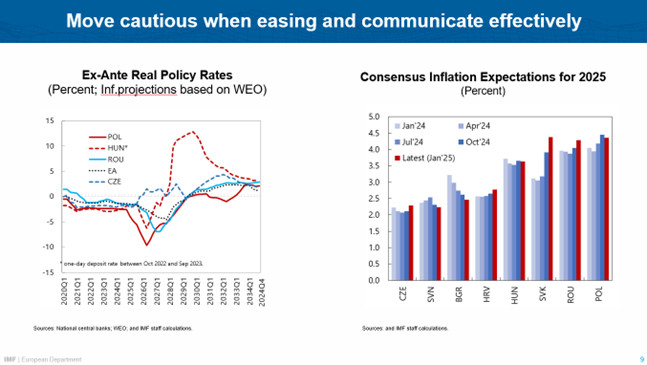

Monetary policy needs to move cautiously in removing its restrictive stance.

While weakening of external demand is likely to be disinflationary (barring sharp currency depreciations), inflation persistence remains a concern. This is especially the case in countries where inflation expectations remain above inflation targets (RHS) and where sustained wage growth is not supported by productivity gains.

Growth-oriented reforms and moderation in public sector wage raises—serving as signals to the private sector—are key.

Two observations on the role of central banks:

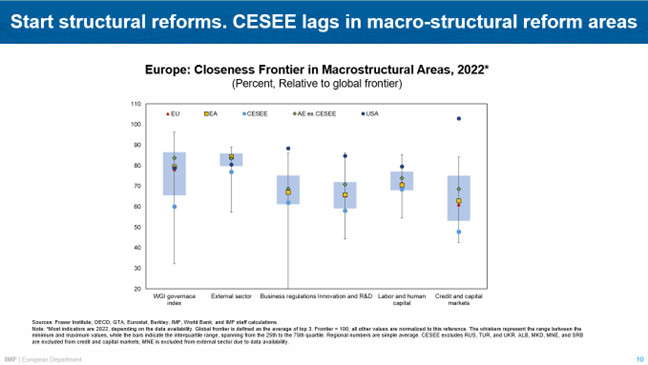

And last but not least in terms of policy priorities, countries need to accelerate structural reforms, to raise their growth potential and strengthen economic resilience.

We are currently undertaking new work on assessing national structural reform priorities across Europe. (This complements work on what can be done at the EU level).

This work finds that the CESEE region lags behind its European and global peers in almost all areas (see chart).

Governance and trade-related barriers are two areas where gaps are large. Similarly, credit and capital markets remain underdeveloped notwithstanding healthy banking sectors.

These gaps limit growth potential but can be addressed with limited fiscal costs. Targeted reforms could unlock investment and long-term competitiveness gains.

Thank you.