The economics of digital innovation

Although the pandemic will leave major economic damage and inequality in

its wake, it will help drive the adoption of digital technologies that

enable financial inclusion and economic opportunity. But these technologies

will not succeed on their own. To understand how digital technology and

policies can help, it is helpful to look first at the underlying economics.

At the heart of digital innovations stand a few technological enablers.

First are mobile phones and the internet, connecting individuals and

businesses with information and providers of financial services. A second

enabler is the storage and processing of large volumes of digital data.

Finally, advances like cloud computing, machine learning, distributed

ledger technology, and biometric technologies play a role.

But at the core of all these innovations is the ability to gather

information and reach users at a very low cost. Economists have assessed

the range of specific costs that decrease with digital technologies

(Goldfarb and Tucker 2019). Two economic features of digital technology

help show why these factors have been so powerful and what risks they pose.

First, digital platforms are highly scalable. Platforms can be thought of

as “matchmakers” that help different groups of users find one another. For

instance, a digital wallet provider like PayPal brings together merchants

and clients who want to make secure payments. The more clients use a

particular payment option, the more attractive it is for merchants to

accept it, and vice versa. This is an example of economies of scale, which

allow providers to grow quickly.

Similarly, Big Techs such as Amazon or China’s Alibaba can serve as

matchmakers to help buyers and sellers of goods find one another, but they

can also link merchants with providers of credit and other services.

Because of the range of services provided (including nonfinancial), they

have information that can be very valuable for their financial offerings.

This exemplifies economies of scope, which give the advantage to providers

with multiple business lines.

Second, digital technologies can improve risk assessment, benefiting from

the same data that are the natural by-product of their business. This is

particularly relevant for services such as lending, as well as investment

and insurance. Credit scores based on big data and machine learning can

often outperform traditional assessments, particularly for “thin-file”

borrowers, people or small businesses with little or no formal

documentation.

Research by BIS economists and coauthors shows that almost a third of

borrowers served by Mercado Libre, a Big Tech lender in Argentina, would

have been unable to access credit from a traditional bank (Frost and others

2019). Moreover, firms that borrowed from Mercado Libre enjoyed greater

sales and product offerings in the year after they borrowed. Research with

data from Ant Group suggests that, by relying on big data, Big Tech lenders

have less need for collateral (Gambacorta and others 2019). This can open

up access to lending for borrowers who have no house or other assets to

offer as collateral, and make loans less sensitive to asset price changes.

Such economies of scale and scope, together with improvements in predictive

power, can drive financial inclusion forward by leaps and bounds. Indeed,

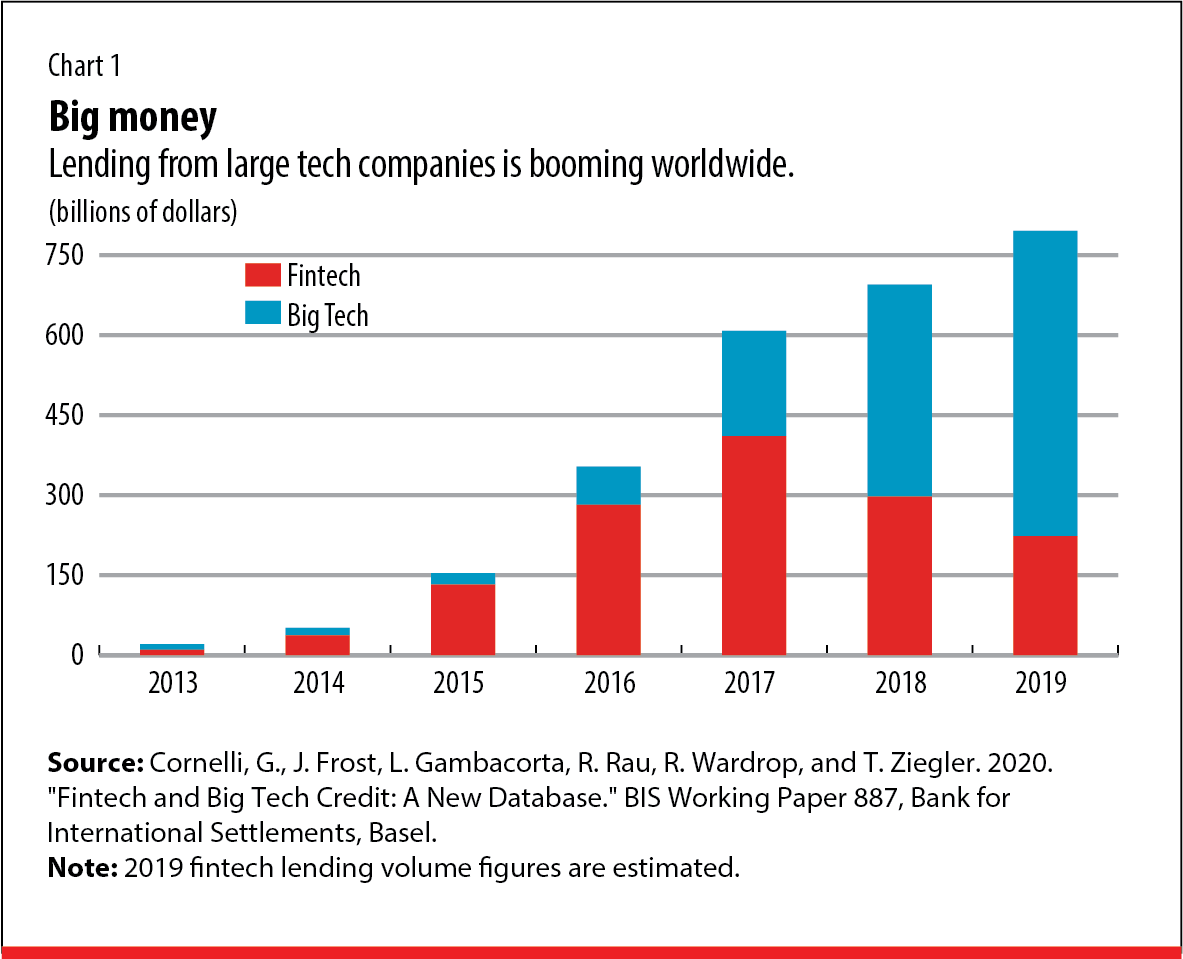

Big Tech credit has boomed worldwide in the past decade, rising to an

estimated $572 billion in 2019 (see Chart 1). Such lending is particularly

important in China, Kenya, and Indonesia, compared with traditional credit

markets. It is also growing rapidly elsewhere and may even have ticked up

during the pandemic as some Big Techs helped distribute government lending

to companies.

However, every silver lining has a cloud, and the advances made possible by

big data have drawbacks—in particular, the tendency toward monopolies. In

some economies, Big Tech payment providers and lenders have become

systemically important (“too big to fail”). The tendency to buy up

competitors may choke off innovation. Finally, there is a serious risk that

sensitive data will be misused and privacy violated. Smart public policies

are needed to mitigate these risks, while allowing the potential of digital

technologies to be fulfilled.