Supply and demand

Earlier this year, The Economics of Biodiversity: The Dasgupta Review, commissioned by

the UK Treasury, was published. In this study, I sought to show how

economics has overlooked Nature. Combining what we know about the biosphere

from earth sciences and ecology, the Review sets out a framework

for including Nature in our economic thinking and provides a guide for

change through three broad, interconnected transitions.

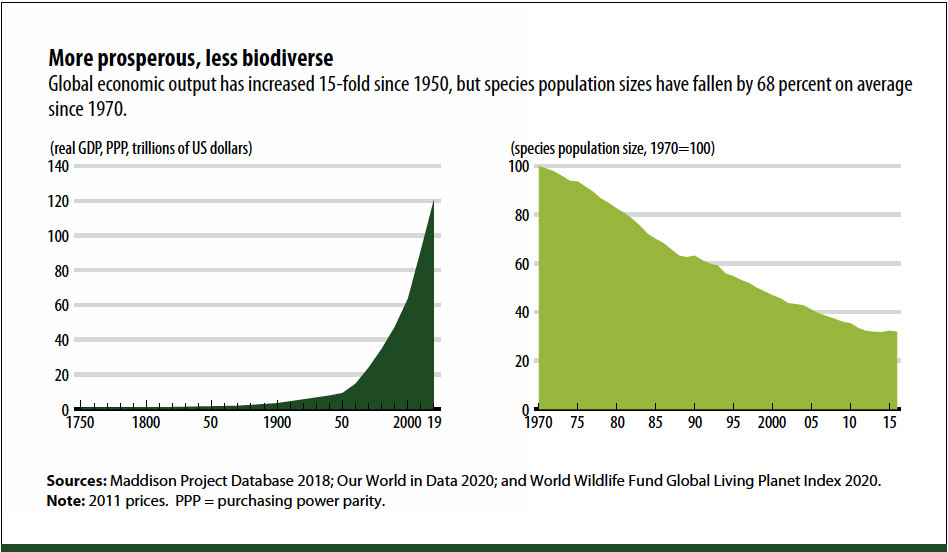

The first is to ensure that our demands on Nature do not exceed its supply.

What we demand of Nature (what some term our “ecological footprint”) has

for some decades far exceeded Nature’s ability to meet those demands on a

sustainable basis, with the result that the biosphere is being degraded at

an alarming rate.

This persistent demand overshoot is endangering the prosperity of current

and future generations, fueling significant risk for our economies and

well-being. Technological innovations—for example, those geared toward

sustainable food production—have an important role to play in ensuring that

our demands on Nature do not exceed its supply.

But if we are to avoid exceeding the limits of what Nature can provide

while meeting the needs of the human population, consumption and production

patterns must be fundamentally restructured as well. Policies that change

prices and behavioral norms—for example, by aligning environmental

objectives along entire supply chains and enforcing standards for reuse,

recycling, and sharing—can accelerate efforts to break the links between

damaging forms of consumption and production and the natural environment.

Human population growth has significant implications for our demands on

Nature, including for future patterns of global consumption. Support for

community-based family planning can shift preferences and behavior and

accelerate demographic transition, as can improving women’s access to

finance, information, and education.