The interwar period shows how a complex network of sovereign debt can aggravate financial crises

Mark De Broeck, Era Dabla-Norris, Nicolas End, and Marina Marinkov

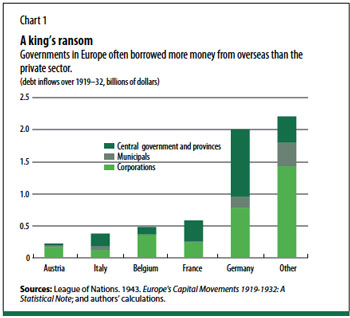

In the early 1930s, as the Great Depression took hold, the international capital flows that were critical to the functioning of the world economy dried up. The reasons are still debated: reckless behavior of speculators and banks, misguided monetary policies, and severe exchange rate misalignments are among the usual suspects. Few would argue that unsustainable fiscal policies and sovereign debt write-offs were the main reasons for the collapse of asset markets and global financial flows. Yet, in Europe in the 1920s and early 1930s, governments often received larger capital inflows than the private sector (see

Chart 1).

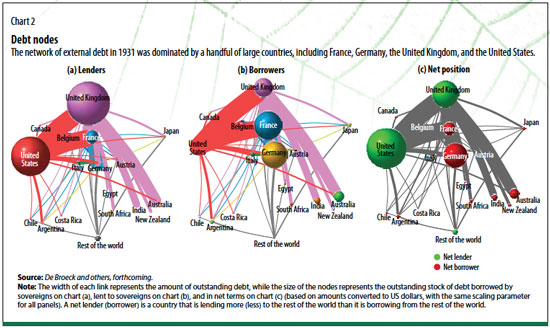

Using a unique new set of data compiled by the IMF that records sovereign debt at the instrument level, we took a close look at the web of debt—most of it incurred because of World War I—that linked the world’s major economies in the interwar period. We found that concerns among investors about the credibility of fiscal policies and sovereign debt service contributed to the severity and persistence of the financial disruptions associated with the Great Depression, even if they were not the trigger.

Our study of the interwar period shows how external sovereign debts can play an aggravating role in global financial cycles, especially when they represent the nodes of a complex financial web. As with the global crisis of 2008 and the euro area crisis of 2010, loss of investor confidence, sovereign debt market disruptions led by liquidity drought, and government intervention in the financial sector added to the external debt burden. Thus, the interwar period offers a telling lens not only for understanding the 2008 crisis, but also for identifying and interpreting present-day vulnerabilities.

In the years after World War I, countries faced very high levels of sovereign debt and an unforgiving macroeconomic environment. Most took steps to reduce deficits and spur growth. The United Kingdom pursued restrictive fiscal and monetary policies to bring down prices in support of the return to the gold standard at prewar parity. Austria and Germany, by contrast, initially failed to achieve fiscal and monetary reform and went down the road of hyperinflation. Italy, Japan, and to some extent, France experimented with capital controls and financial repression—government domination of banks or manipulation of money markets.

These strategies found parallels in the years following the 2008 crisis: Greece restructured its public debt, and Iceland and Cyprus adopted capital controls. Banks in Greece, Italy, Portugal, and Spain sharply increased holdings of their own governments’ debt. While such so-called home bias helps reduce government borrowing costs and provides fiscal breathing space in times of stress, it also obscures the pricing of risk, as it did during the interwar period.