Does globalization enhance resilience? Or does it have no effect? Or the opposite effect?

For the two major economic disruptions so far this century—the global financial crisis starting in 2008 and the COVID-19 pandemic starting in 2020—economists’ answers to those questions were largely wrong. As for the financial crisis, most of them underestimated the risks of financial globalization, and when it came to the pandemic, most overestimated the risks of sprawling, intricate production networks and trade globalization.

As the Russian invasion of Ukraine and the sweeping sanctions that followed now threaten to ignite a third great crisis, it’s important to understand where economic analysis goes wrong and the adjustments practitioners need to make to get things right. The flawed predictions about the financial crisis and the pandemic certainly reflected inadequate understanding of the workings of financial and trade markets. And they most likely also grew out of overreliance on imperfect economic modeling.

Before the financial crisis, most economists had a positive view of financial globalization’s effects on resilience. The thinking was that the growth of the financial sector, especially international finance, would allow economic agents and countries to diversify risk through financial instruments. New financial products would fill missing markets. The expectation was that cross-border financial integration would lead to more risk sharing.

There were significant caveats and voices of doubt. In 2005, former IMF Chief Economist Raghuram Rajan warned that “even though there are far more participants who are able to absorb risk today, the financial risks that are being created by the system are indeed greater. ... They may also create a greater (albeit still small) probability of a catastrophic meltdown.”

Overreliance on self-correcting financial markets

In fact, the US subprime mortgage crisis did spill over to global banks and across borders precisely because of those same links that were supposed to provide insurance and resilience. Two years after he left office as chairman of the Federal Reserve, Alan Greenspan finally conceded that he was in error about regulation, in congressional testimony on October 23, 2008. “A humbled Mr. Greenspan admitted that he had put too much faith in the self-correcting power of free markets and had failed to anticipate the self-destructive power of wanton mortgage lending,” The New York Times reported.

More broadly, a vast literature has focused on why global finance proved so fragile and led to the global financial crisis. Incomplete knowledge about networks, global imbalances, loose monetary policies that led to excessive risk-taking, improperly aligned incentives, and gaps in regulation, perhaps in part for political economy reasons—among many factors—have all been cited by researchers.

A crisis whose initial magnitude was estimated at less than $200 billion wreaked havoc on the global financial system to the tune of several trillion dollars, resulted in devastating unemployment and social costs around the globe, and set off the worst recession since the Great Depression.

Overestimating the pandemic’s damage

What happened during the COVID-19 crisis? As the pandemic began, world production and trade seemed highly vulnerable. Over the past few decades, both have increasingly relied on just-in-time global value chains. In this system, key materials and components are produced in different countries or regions based on comparative advantages. While these production networks and global value chains have enhanced efficiency, they have also led to new fragility. A single missing input can block entire production chains. To capture the idea of “critical inputs,” economists used models with low elasticities of substitution between different inputs.

This line of thought seemed to be vindicated by disruptions following natural disasters, including Hurricane Katrina and New Orleans in 2005 and the Great East Japan Earthquake of 2011. A 2021 study of the Japanese case found that “even if average firm-level effects are not necessarily large, the potential propagation of shocks over the economy’s production network can impact a significant fraction of firms, thus resulting in movements in macroeconomic aggregates.” Other researchers suggested that similar logic could apply to the transmission of shocks across borders.

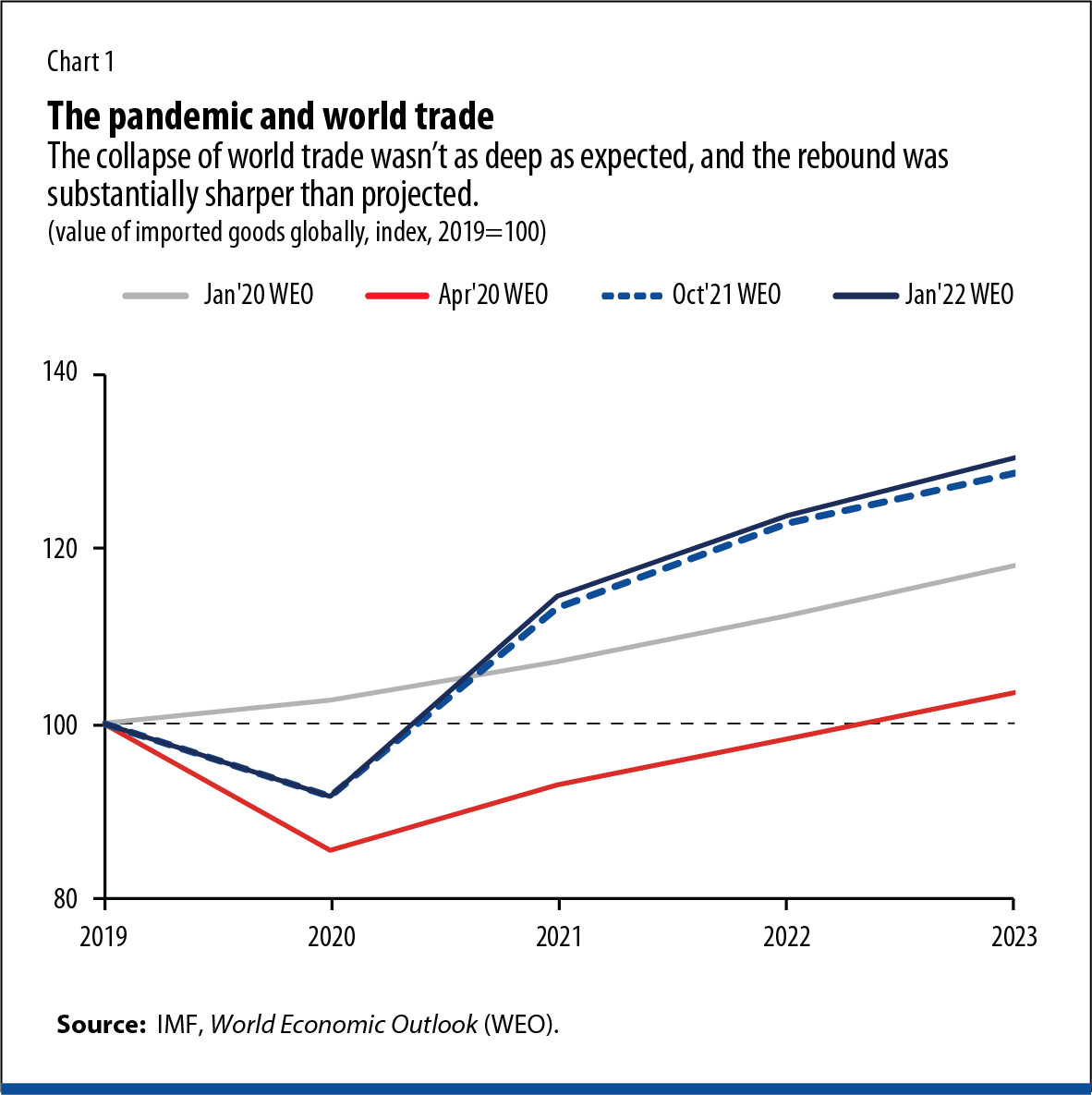

In the context of COVID-19, this implied that if the pandemic knocked out only one key country—or region within a country, or factory for that matter—it could break entire production chains. Given the diffusion of the pandemic around the world, trade could be particularly vulnerable. This view was not common only in academic circles. Emphasizing supply disruption, the World Trade Organization and several other groups warned that the pandemic would lead to a collapse in trade. Serious news outlets reported that such disruption was taking place, such as the Wall Street Journal in an August 2020 article, “Covid Crisis Drives Historic Drop in Global Trade.” Against this backdrop, it was expected that the pandemic would devastate global economies. For instance, the IMF’s World Economic Outlook (WEO) projections in April 2020 forecast a large drop in world trade, even as a share of world income.

What actually happened was quite different. Chart 1 shows the evolution of projections of world merchandise imports by value. World merchandise imports are commonly used as a measure of trade globalization. The advantage of this measure is that several vintages of projections are readily available.