Loading component...

Loading component...

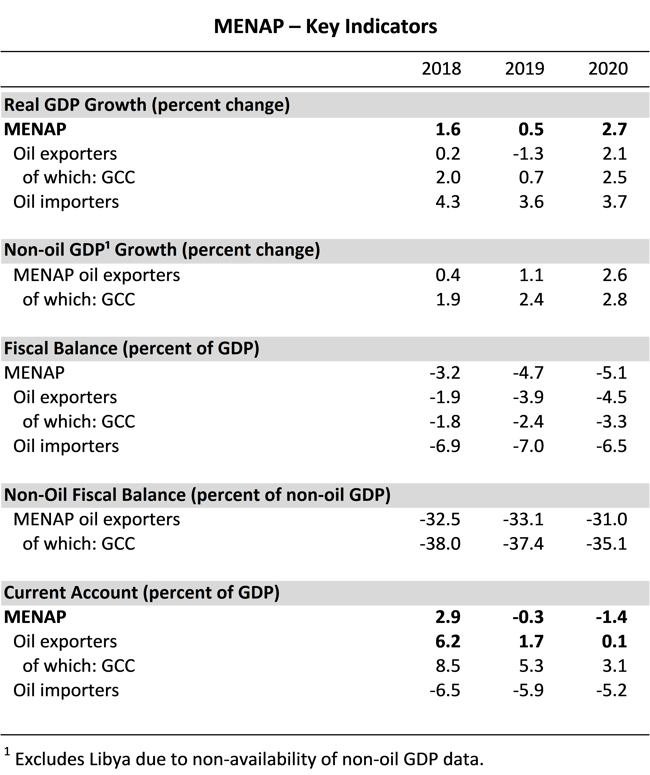

MENAP Summary

The impact on growth in the Middle East, North Africa, Afghanistan, and Pakistan (MENAP) region from global headwinds remains muted thus far. However, growth remains too low to meet the needs of growing populations, while risks to the outlook have increased. They include global trade uncertainties, volatile oil prices, geopolitical tensions, and domestic vulnerabilities in some countries.