More than 15 years after the global financial crisis, the banking and financial system looks safer. But it’s also evolving in ways that are reshaping who provides liquidity, how money moves, and risks to economic and financial stability. As a result, the next shock may begin not in a bank, but in the new infrastructure underpinning the system.

After 2008, regulators moved swiftly to raise capital standards and introduce new supervisory tools such as stress testing. Banks rebuilt their balance sheets and retreated from risky lending and arbitrage businesses. Asset managers were blamed for the financial turmoil at the onset of the pandemic, but not banks.

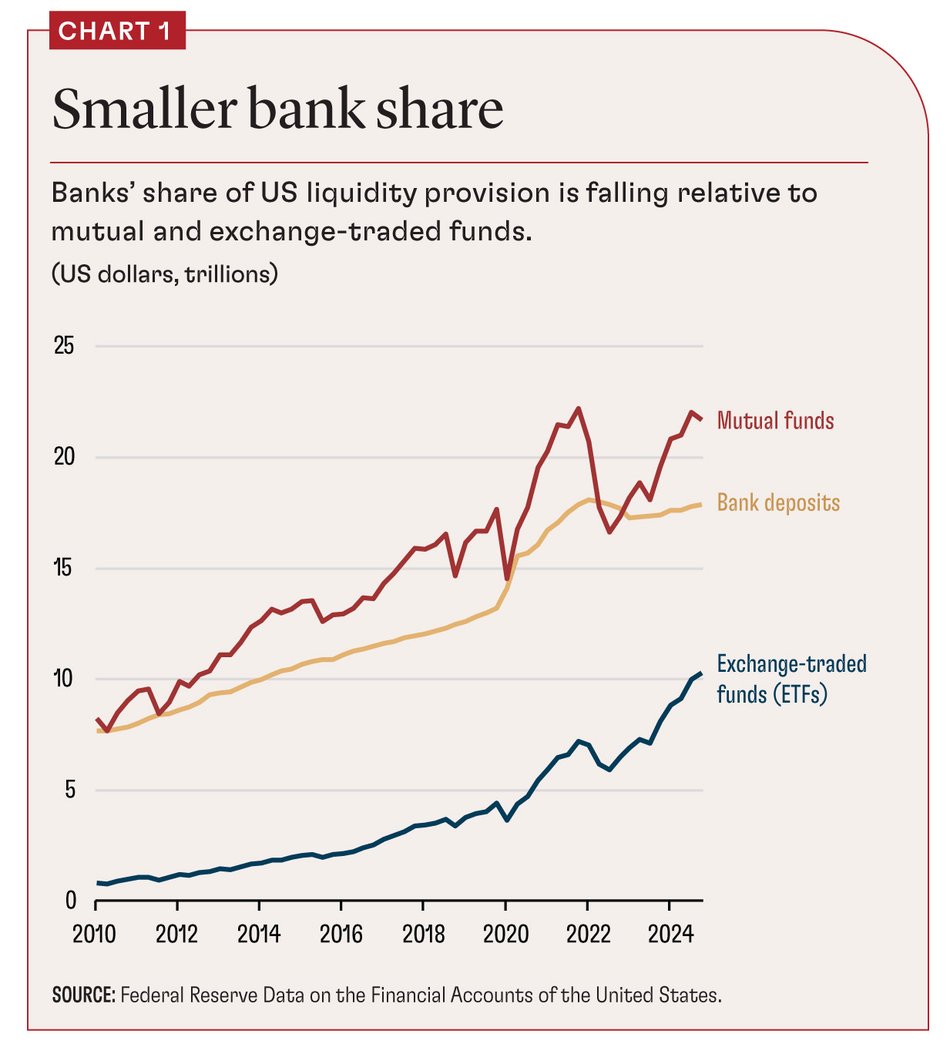

Yet even as regulators fortified banks, postcrisis innovations reshaped the financial landscape. Asset managers provided more liquidity as banks stepped back, nonbank start-ups built new risk assessment tools for institutional lenders, developers introduced a wider array of crypto assets, and central banks and governments established real-time payment systems.

These developments cut costs, broadened access, and accelerated transactions. Yet they also caused significant shifts in the structure of financial intermediation. Liquidity, credit, and payments—the core of the banking system—gravitated toward asset managers, tech platforms, and decentralized networks.

This reshaping of finance itself now raises big questions. What happens when critical finance functions lie outside the regulatory framework? How should we ensure stability in a faster, flatter, and more fragmented financial system?

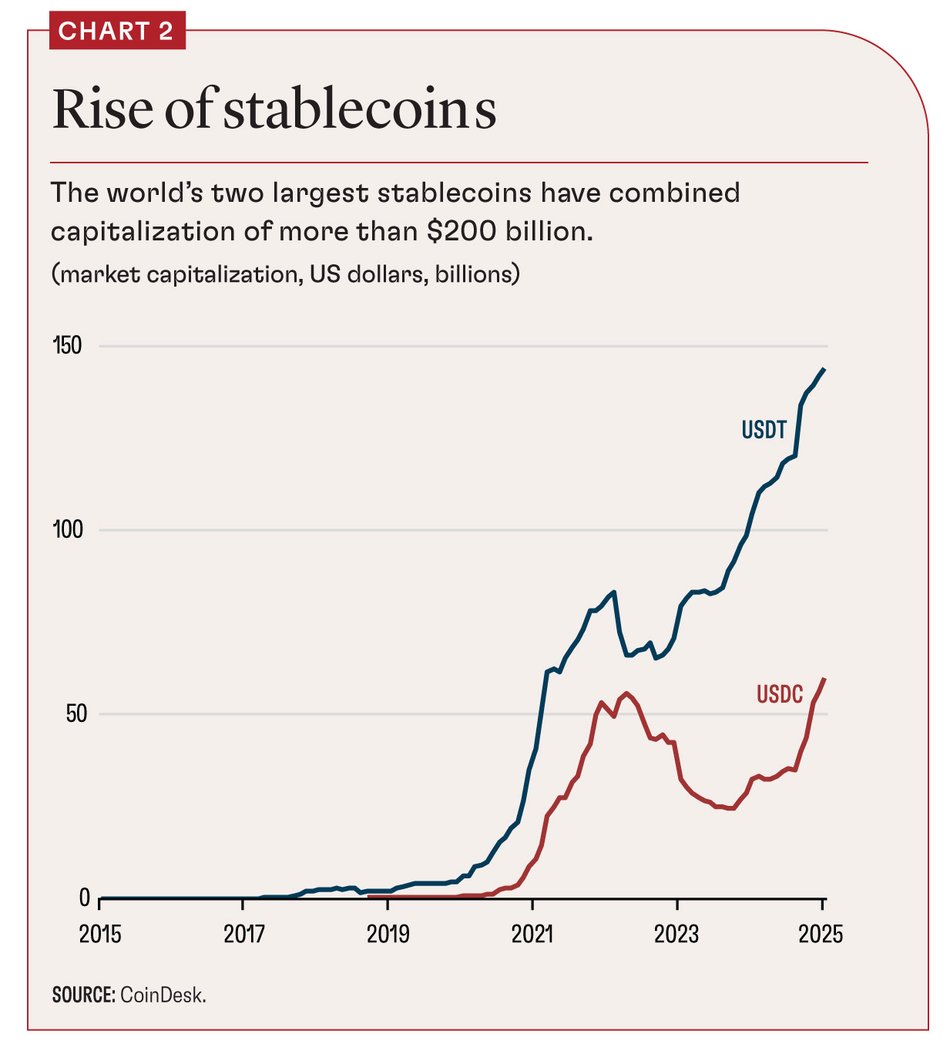

From banks to asset managers

Banks were once the protagonists of liquidity creation for financial markets. Yet today, it is nonbank asset management funds, not banks, that contribute a growing share of the system’s day-to-day liquidity to households and investors (Chart 1). Open-end mutual funds and exchange-traded funds (ETFs) let investors redeem money on demand, even though these funds hold assets such as corporate bonds that are anything but liquid. They promise daily liquidity but hold underlying assets that can’t always be sold—just as banks do, but without deposit insurance, capital buffers, or access to the central bank.

This isn’t theory. It’s happening. My research with Columbia University’s Yiming Ma and Kairong Xiao shows that bond mutual funds alone now supply sizable liquidity compared with the entire banking system, and this share is rising. Yet when markets turn volatile, mutual funds can be shock amplifiers rather than absorbers. They may be forced to sell illiquid assets in a falling market, deepening the stress.

ETFs add complexity. On paper, most ETFs are passive vehicles. More than 95 percent track an index, such as the S&P 500 or Bloomberg US Aggregate Bond Index. But in practice, many are surprisingly active. There are now more ETFs than underlying assets. For many asset classes, investors can choose among plain-vanilla trackers, sector-specific funds, smart beta strategies, and even thematic products like AI-, robotics-, and green-focused ETFs.

Behind the scenes, ETF sponsors must actively manage portfolios to meet investor flows and keep prices in line with the value of the underlying assets. Bond ETF managers frequently deviate from their stated benchmarks, as my work with Naz Koont of Stanford University, Lubos Pastor of the University of Chicago’s Booth School of Business, and Columbia’s Ma shows. Bond ETFs, especially, trade like liquid stocks but hold underlying illiquid bonds. They rely on a network of specialized intermediaries, called authorized participants, to arbitrage price discrepancies between ETFs and underlying assets.

These participants are also bond dealers and use the same balance sheets both in their role of managing ETFs and to serve their trading clients. When dealer balance sheets get tight, or when bond markets seize up, ETF arbitrage can break down. Prices drift, and liquidity thins. And investors who expected stock-like flexibility may be left holding something closer to a closed-end fund.

The new ecosystem of liquidity provision is more market based, broader, and potentially cheaper than the old one. After all, bankers face greater constraints in providing daily liquidity, and asset managers step in to fill the gap. But the new ecosystem plays by a different rule book, with different risks when markets freeze.

AI and big data

Lending, once the province of bankers and loan officers, increasingly relies on AI and big data. Nonbank fintech platforms use payment records and machine learning to cut search costs, bypass collateral requirements, speed loan approvals, and reach borrowers that traditional banks often overlook. Data, in turn, flows more freely between borrowers and lenders, training increasingly precise and adaptive machines. My research with the Indian Institute of Management’s Pulak Ghosh and Harvard’s Boris Vallee shows how this plays out in India. Small merchants who rely more on cashless payments with detailed and traceable paper trails get better access to working-capital loans. They pay lower interest rates and are less likely to default. In effect, digital footprints are the new credit scores.

This credit-data feedback loop has boosted the power of Big Tech. Platforms such as Alibaba’s Ant Group, Amazon, and Latin America’s Mercado Libre now bundle payments, e-commerce, and credit. The size of their consumer and small-business loan books now exceeds that of many banks. Scale delivers convenience, but also concentration: The platform that controls the checkout button can steer borrowers and merchants away from rival bank lenders, raising difficult questions about competition.

Size is not the only concern. Because Big Tech sits outside traditional safety nets, traditional capital, liquidity, and resolution rules do not yet apply. In 2024, Amazon abruptly discontinued its $140 billion in-house lending program to small businesses, illustrating how platform credit can vanish just when firms need it most. As AI- and data-driven lending pushes ever more credit through a few digital gateways, more questions crop up alongside the emergence of too-big-to-fail tech monopolies.