Artificial intelligence is often cast as intangible, a technology that lives in the cloud and thinks in code. The reality is more grounded. Behind every chatbot or image generator lie servers that draw electricity, cooling systems that consume water, chips that rely on fragile supply chains, and minerals dug from the earth.

That physical backbone is rapidly expanding. Data centers are multiplying in number and in size. The largest ones, “hyperscale” centers, have power needs in the tens of megawatts, at the scale of a small city. Amazon, Microsoft, Google, and Meta already run hundreds worldwide, but the next wave is far larger, with projects at gigawatt scale. In Abu Dhabi, OpenAI and its partners are planning a 5-gigawatt campus, matching the output of five nuclear reactors and sprawling across 10 square miles.

Economists debate when, if ever, these vast investments will pay off in productivity gains. Even so, governments are treating AI as the new frontier of industrial policy, with initiatives on a scale once reserved for aerospace or nuclear power. The United Arab Emirates appointed the world’s first minister for artificial intelligence in 2017. France has pledged more than €100 billion in AI spending. And in the two countries at the forefront of AI, the race is increasingly geopolitical: The United States has wielded export controls on advanced chips, while China has responded with curbs on sales of key minerals.

The contest in algorithms is just as much a competition for energy, land, water, semiconductors, and minerals. Supplies of electricity and chips will determine how fast the AI revolution moves and which countries and companies will control it.

A hungry industry

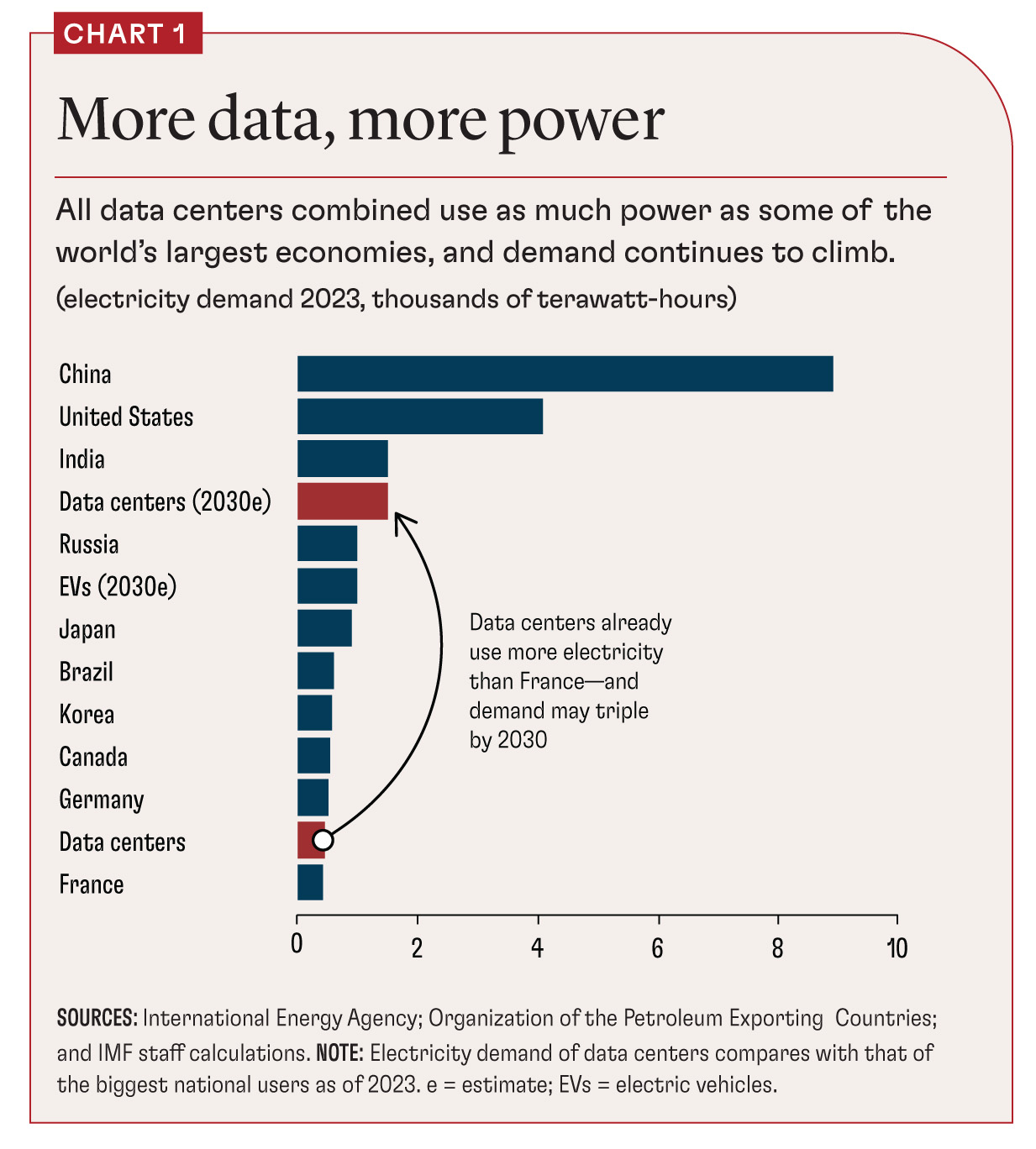

Artificial intelligence is devouring electricity. Data centers already use about 1.5 percent of global electricity supply, roughly the same as the United Kingdom. Only a portion of that demand comes from AI, but it is growing fast. Training an advanced model can consume as much power as thousands of households use in a year, and running it at scale multiplies the burden. The International Energy Agency (IEA) expects data center demand to more than double by 2030, with AI responsible for much of the increase.

Globally this surge is manageable: AI accounts for less than a tenth of added power demand this decade, far below that of electric vehicles or air-conditioning. But national balances tell a different story. In the US and Japan, data centers could account for nearly half of new demand by 2030. In Ireland, they already use more than a fifth of the country’s electricity, the highest share among advanced economies.

The local strains are sharper still. Unlike steel plants or mines, data centers cluster near big cities, can be built in months rather than years, and keep getting bigger. This combination makes them uniquely disruptive to local grids.

In northern Virginia, the world’s largest data hub, data centers already consume about one-quarter of the state’s power, forcing utilities to delay or cancel other connections. Rising electricity bills became a flash point in the state’s governor’s race. In Ireland, Dublin’s grid operator froze new projects in 2022, approving only those that could generate their own power. Singapore halted approvals altogether in 2019 and now allows facilities only under strict efficiency rules.

Big Tech turns to power

Technology companies are becoming power players themselves. The largest firms are now among the world’s biggest corporate buyers of renewable energy. Microsoft, Amazon, and Google have each signed multibillion-dollar power purchase agreements that rival those of traditional utilities. Their decisions about where to site data centers increasingly shape which solar and wind projects get built.

Some are adding on-site generation at data centers to cut reliance on the grid, or are betting directly on new technologies. Microsoft has explored nuclear, from small modular reactors to possible acquisitions of mothballed plants such as Three Mile Island in Pennsylvania. Google is backing advanced geothermal. Amazon is testing hydrogen for backup power. With President Donald Trump rolling back many of President Joe Biden’s climate policies, the AI power race has unexpectedly cast Big Tech as a lifeline for clean-energy investment.

Over time, Big Tech’s capital could help accelerate innovation in clean power, but it could also cement dependence on fossil fuels. While AI has boosted renewables in Europe, demand in the US—home to more than 40 percent of the world’s data centers—still leans heavily on natural gas, adding to emissions.

Smarter machines

Artificial intelligence is not only a voracious consumer of electricity, it can also help manage it, balancing power grids, forecasting renewable output, and optimizing energy use in buildings and industry. Some cities are even piping waste heat from server farms into district heating networks. These applications will not erase the sector’s footprint, but they can soften the strain.

Efficiency is improving too. New generations of chips, such as Nvidia’s Blackwell processors and Google’s tensor processing units (TPUs), are designed to deliver more operations per watt. On the software side, China’s DeepSeek, released in January 2025, was trained at a fraction of the cost and energy of what OpenAI and Google spent on comparably sized models.

Yet efficiency brings its own paradox. History suggests that cheaper computing power sparks more use, an effect known as the Jevons paradox. AI may indeed deliver smarter, leaner models, but the appetite for applications is likely to grow even faster.

If electricity is AI’s first constraint, semiconductors are the second. Training state-of-the-art models requires thousands of specialized chips, most designed by Nvidia and manufactured almost exclusively in Taiwan Province of China by the Taiwan Semiconductor Manufacturing Company (TSMC). That concentration has made chips the single most strategic choke point in the AI supply chain.

The geopolitical stakes are already clear. The US has restricted advanced chip exports to China while subsidizing domestic fabrication plants. Far from stifling progress in China, those curbs may have pushed its companies to innovate around them, as DeepSeek has shown. Beijing is racing to build its own domestic champions. Europe, Japan, and India are pouring billions into their own industries. Access to chips is now a litmus test of technological sovereignty.