The study, published in the IMF’s October 2016 World Economic Outlook, finds that low and falling inflation in the aftermath of the Great Recession is a broad-based phenomenon across countries, measures, and sectors.

This “disinflation” is more obvious when looking at the prices of tradable consumer goods—such as cars and TVs—rather than services—say, communications and financial services. Further, the decline in inflation has been mainly driven by persistent economic slack at home—given weak demand and growth conditions—and falling commodity prices. In addition, the study finds that industrial slack in large exporters may have contributed to lower inflation by depressing the global price of tradable goods.

But this is not the whole story. While expectations of the path of future prices, or inflation expectations, have not declined substantially so far, the study finds that the response of inflation expectations to unexpected changes in inflation—an indicator of how well “anchored” inflation expectations are—has increased in countries whose interest rates are close to or below zero.

This suggests that the perceived ability of monetary policy to combat persistent disinflation may be diminishing in these economies.

A broad-based decline in inflation

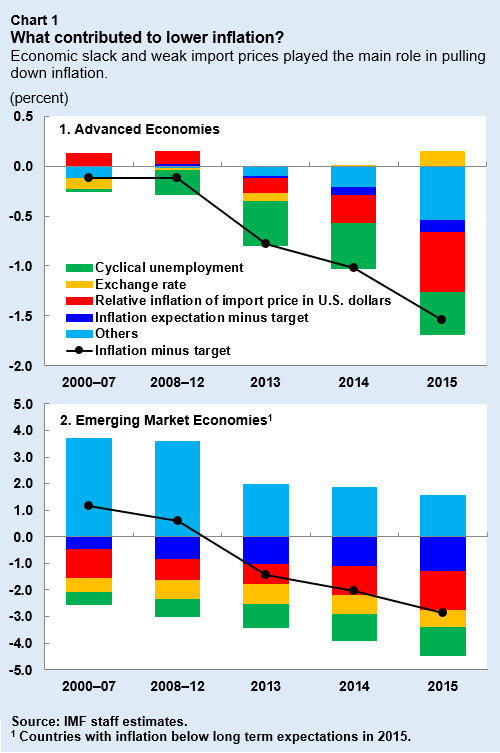

Disinflation has been taking place across a broad range of countries and regions. By 2015, inflation rates were below medium-term expectations in more than 85 percent of a broad sample of more than 120 economies—20 percent of which were actually experiencing outright deflation. The sharp drop in oil prices since 2014 is partly to blame but core inflation, which excludes food and oil prices, has also slipped below central banks’ inflation targets in most advanced economies and in many emerging market economies more recently. While inflation has softened in all sectors, the decline has been larger for manufacturing producer prices than those of services.

Recent drivers of disinflation

Weak demand and persistent economic slack have contributed to recent disinflation among advanced and several emerging market economies (Chart 1). But subdued import prices have also played a key role in bringing inflation down. This partly reflects the decline in oil and other commodity prices, but the study shows that the effect of weaker import prices on domestic inflation is also associated with industrial slack in key large economies.

Indeed, investment in tradable goods sectors in some large economies, notably China, grew strongly in the aftermath of the global financial crisis on the back of projections for global and domestic demand that ex post fell short of expectations. The resulting excess capacity in these economies put downward pressure on international prices of tradable goods, generally implying cheaper imports for the rest of the world.

Should we be concerned about disinflation?

In general, short-lived disinflation would not be something to worry about. A temporary fall in inflation due, for instance, to a supply driven decline in energy prices or productivity gains can be beneficial.

However, if repeated disinflation leads firms and households to revise down their beliefs about future prices, they may postpone spending and investment decisions, leading to a contraction in demand that would exacerbate the deflation pressures. Eventually, “persistent” disinflation can lead to costly deflationary cycles—as we have seen in Japan–where weak demand and deflation reinforce each other, and end up increasing debt burdens and hindering economic activity and job creation.

The role of inflation expectations

A key factor to consider, therefore, is people’s expectations about the path of future prices. A fall in prices today could be a factor when people form their expectations about what lies ahead. Here, the ability of central banks to anchor medium-term inflation expectations to their inflation objectives can help avoid costly disinflation.

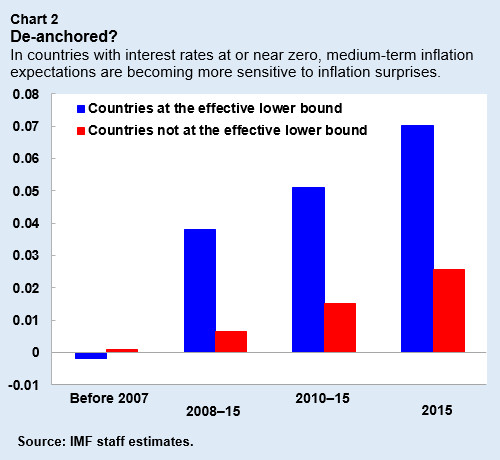

So far, most available measures of inflation expectations have not declined much. But the study shows that, for countries where interest rates are at or close to zero, central banks may be perceived as not having much room to boost activity and inflation. In fact, the study finds that the sensitivity of these expectations to unexpected changes in inflation, which would be expected to be zero if inflation expectations are perfectly anchored, has been recently increasing (Chart 2). This would imply that inflation expectations are becoming de-anchored from central banks’ targets in those countries.

While the economic magnitude of this “de-anchoring” is still relatively small, it does suggest that the perceived ability of monetary policy to combat persistent disinflation may be diminishing in some economies.

Policy actions to keep expectations anchored

Bold policy actions are needed to avoid the risk of chronically undershooting inflation targets and eroding the credibility of monetary policy, especially in advanced economies.

Given that policy space is limited in many economies, a comprehensive and coordinated approach across all available policy levers would be needed to boost demand and firm up inflation expectations in the current juncture. Broadly speaking, this involves complementing continued monetary accommodation with growth-friendly fiscal policies, income policies (in countries where wages are stagnant), and demand-supporting structural reforms, while addressing crisis legacies (debt overhangs and large non-performing bank loans).

The risk that current widespread disinflation would evolve into damaging deflation-trap situations is still small. But since it has proven very difficult to reverse deflationary dynamics once they set in, countries can’t afford to be complacent.