High vulnerability

Since 1950, 511 disasters worldwide have hit small states—that is, developing economies with populations of less than 1.5 million. Of these, 324 were in the Caribbean, home to a predominant share of small states, killing 250,000 people and affecting more than 24 million through injury and loss of homes and livelihoods.

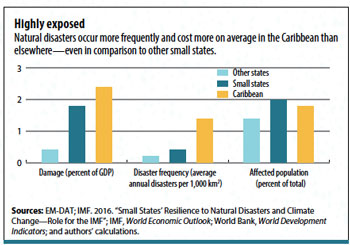

The Caribbean’s vulnerability is characteristic of small island states, but this region has typically suffered more damage than others. Average estimated disaster damage as a ratio to GDP was 4.5 times greater for small states than for larger ones, but six times higher for countries in the Caribbean. Moreover, the region is seven times more likely to be hit by natural disasters than larger states and twice as likely as other small states (see chart).

The economic cost of these disasters for the Caribbean is substantial, exceeding $22 billion (in constant 2009 dollars) between 1950 and 2016, compared with $58 billion for similar disasters globally. For some countries, the damage well exceeds the size of the economy: Hurricane Maria is estimated to have cost Dominica 225 percent of its GDP, while the hurricane damage for Grenada in 2004 was 200 percent of GDP, leaving huge reconstruction needs that can take years to fulfill.

Climate change is expected to compound the problem by making such disasters more frequent and severe. While the Caribbean accounts for a tiny part of greenhouse gas emissions globally, it is disproportionately more vulnerable to climate risks. Large shares of the region’s population live in high-risk areas with weak infrastructure. Moreover, their economies rely heavily on sectors sensitive to weather, such as tourism and agriculture, while capacity and resources to manage risk are limited. Recurrent floods, droughts, hurricanes, and rising sea levels pose a threat to agriculture and coastal areas and increase the risk of water and food insecurity. Climate-related disasters encourage migration, as noted by Michael Berlemann and Max Steinhardt in their 2017 paper “Climate Change, Natural Disasters, and Migration—A Survey of the Empirical Evidence.” This could become a significant policy concern for the Caribbean, where brain-drain poses a serious threat to growth.

Disasters have large and enduring economic effects that range from lost income to the destruction of physical and human capital, infrastructure, and property. Rebuilding provides a temporary boost, but indirect effects can spread throughout the economy and undermine investment, growth, and macroeconomic performance. Debt dynamics inevitably worsen as governments borrow to finance recovery and growth slows.

An analysis of 12 Caribbean countries with the largest damage costs relative to GDP since 1950 supports this view. Although most countries experienced reduced growth in the year of a disaster, they recovered in the subsequent year. But fiscal deficits increased in 7 of 12 countries, current accounts deteriorated, and debt-to-GDP ratios surged. In some, debt continued to rise, suggesting that exposure to frequent disasters interrupts efforts to sustain strong growth and improve public finances.

If these countries could reduce disaster damage, they might generate significant growth dividends and find their way out of the vicious cycle of high debt and low growth in which many are currently trapped.