WHAT IS THE IMF?

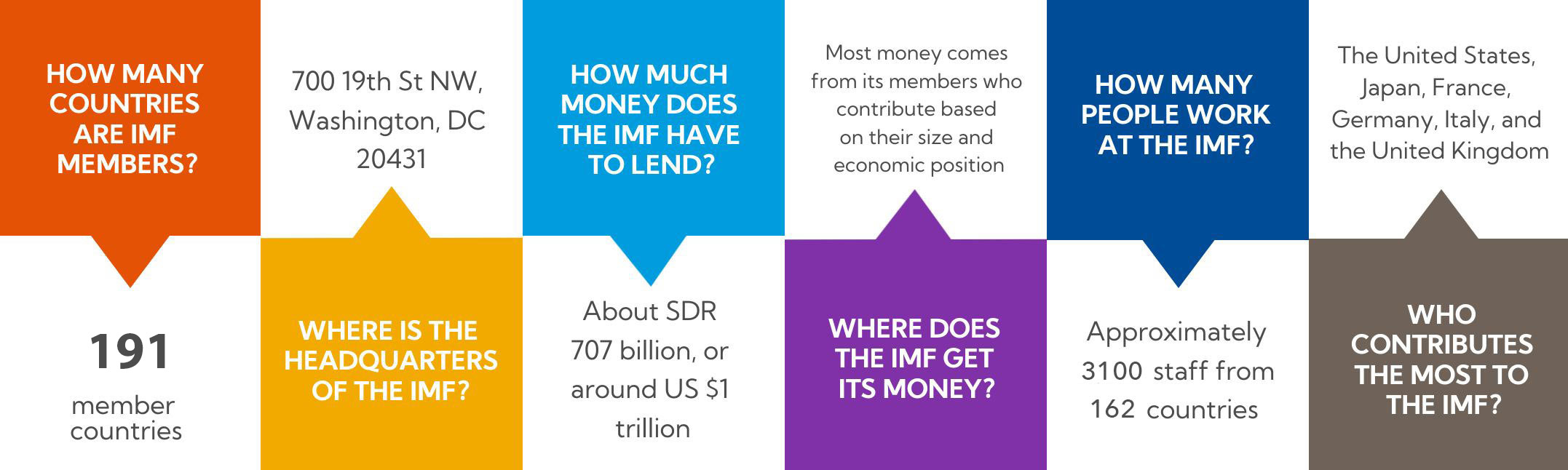

The International Monetary Fund (IMF) works to achieve sustainable growth and prosperity for all of its 191 member countries. It does so by supporting economic policies that promote financial stability and monetary cooperation, which are essential to increase productivity, job creation, and economic well-being. The IMF is governed by and accountable to its member countries.

The IMF has three critical missions: furthering international monetary cooperation, encouraging the expansion of trade and economic growth, and discouraging policies that would harm prosperity. To fulfill these missions, IMF member countries work collaboratively with each other and with other international bodies.

Loading component...

Loading component...

Loading component...

Loading component...

Loading component...

Loading component...

Loading component...

Loading component...

Loading component...

Frequently Asked Questions

Loading component...

Loading component...

Loading component...

Loading component...

This page was last updated in April 2025