Pumping oil in California, United States. Over the last decade, the world has been using oil more efficiently (photo: Lowell Georgia/Corbis)

ENERGY ANALYSIS

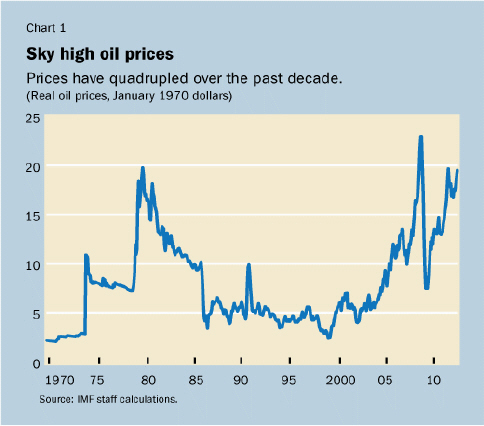

During the current economic downturn, the price of oil hit over $100 a barrel, and prices rose close to levels only seen in the 1970s. But the increases have not triggered global recessions as they did in the 1970s and 80s.

In new research, IMF economists attribute this resilience to five underlying factors:

1. Stronger demand

The reason for the current price hikes differs from the past. Increases in the 1970s and 1980s were caused largely by sharp disruptions to world supply. In contrast, a prime reason for the increases since 2000 has been stronger-than-expected demand from emerging market economies.

The strong growth of emerging markets has benefited both them and the global economy: raising living standards and increasing their demand for products made abroad.

A side-effect of this may have been an increase in oil prices, but this has not derailed the benefits of increased growth.

2. Central bank policies

Central banks and economies have become more adept at dealing with price shocks. In the 1970s and 1980s, oil price rises triggered fears of inflation, and workers would try to protect themselves by demanding higher nominal wage increases. This had the effect of setting off wage-price spirals.

Now, greater awareness of the impact of high wage increases—including lost employment and reforms to labor markets—have led to more job-friendly wage setting. Central banks have become more adept at convincing workers that oil price increases will not feed through into inflation.

Today, headline inflation temporarily increases after an oil price increase, but nominal wages hardly respond. Workers have grown to expect this rise in headline inflation, and anticipate that it will be temporary.

Given the experience of the past, more recently many oil-importing economies with strong central banks have experienced little impact on core inflation and wage increases, despite oil price rises.

This has allowed central banks to be more supportive of promoting recovery in the economy after an oil price increase, rather than having to raise interest rates to dampen inflationary expectations.

3. Recycling the benefits of oil profits

The revenues from oil exports are flowing back to oil-importing economies. This helps bring down interest rates for households and firms, and so supports investment and growth in these economies.

4. Greater efficiency

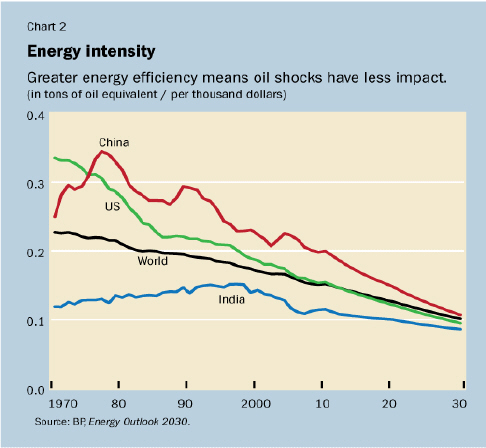

Oil price shocks do not have the same impact as in the past because economies have become more efficient in the use of energy. The amount of energy it takes to produce a dollar of income has been steadily declining for 40 years. This decline in energy intensity is expected to continue.

Major emerging markets are also becoming more efficient in the use of energy, and they are expected to continue to make efficiency gains. By 2030, the major regions of the world—the United States, China, and India—are projected to have the same energy intensity.

5. Diversification

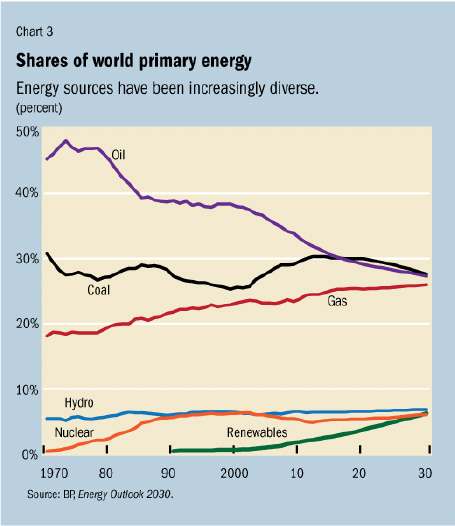

Countries have increasingly diversified their energy sources over recent decades. They import energy from many more places than in the 1970s. They also use more varied forms of energy. This makes them less vulnerable to disruptions from any one supplier or source of energy.

The United States, for example, buys crude oil and gasoline from more than 40 countries and jet fuel from more than 25 countries.

Countries have also increased their use of natural gas, and are importing it from many more countries. Norway has continued to grow in importance as an exporter of natural gas, and several new producers have emerged, including Qatar, Turkmenistan, Nigeria, Egypt, and Australia.

By 2030, it is expected that energy use will be even more diversified. Oil, coal, and gas are predicted to each have a 30 percent world market share, with hydro, nuclear and renewables accounting for the remaining 10 percent.

Oil supplies remain a concern

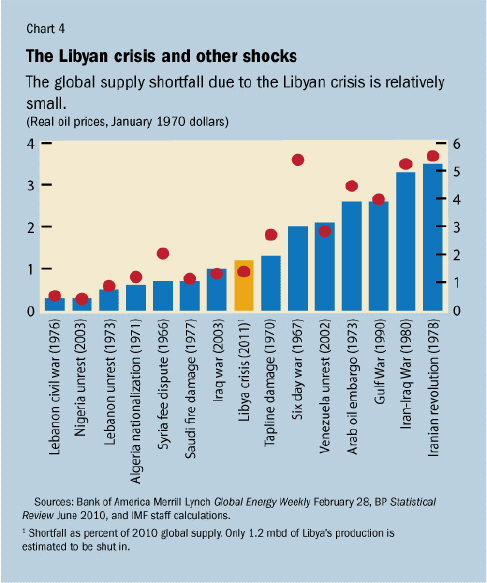

Despite the reduced impact of high oil prices in recent years, large, abrupt price changes remain difficult to absorb, particularly if they come from supply disruptions. Recent geopolitical developments offer plenty of examples of such disruptions.

Recent supply shortfalls have been smaller than in the 1970s, but the potential for larger disruptions cannot be ruled out.

Over the short term, concerns center on Iran, the fifth largest world producer and third largest exporter. Supply from Iran is expected to drop during the second half of this year, in response to international sanctions.

It is unclear how this will affect oil prices, but it is likely that market prices may anticipate the impending drop in supply to some extent, while other producers may react by increasing output. Saudi Arabia has already increased production to a 30-year high in response to recent disruptions.

The impact of supply disruptions

The effects of major supply disruptions can be particularly damaging under current conditions because there is limited spare capacity to increase oil production, and inventory levels in importing countries are low.

This will compound the difficulties facing many households already reeling from the financial crisis, with higher prices for gasoline and heating oil adding to the pain inflicted by high unemployment and low wages.

Fears of oil scarcity—the worry that the world will simply run out of oil—also loom large in the minds of many. A recent IMF Working Paper suggested that some of the gyrations in oil prices in recent years have come about because market participants appear to give some credence to this geological view of binding constraints on oil supplies.

Future supply disruptions may turn out to be costly not just because of the immediate loss of oil supplies, but because of the fears they trigger about a more permanent loss.

Response of oil suppliers

The response by oil suppliers to higher prices has been slow despite many years of rising and high prices. Bringing additional oil capacity to the market remains a challenge for various reasons including geology, geography, technology, and regulation.

But, provided oil prices increase fairly gradually in response to scarcity, the developments of the past decade suggest that the global economy should be able to cope without major output losses, as noted in the April 2012 World Economic Outlook.

Higher oil prices will raise the cost of fertilizers, and thus the cost of food. This effect has already taken place over the past decade. It raises special challenges for the poorest economies.

Some of these economies have become major oil exporters and have less need to worry. But others may require help. Most of these economies will need to build up their social safety nets so that they can reach those most in need.

Liquidity trap?

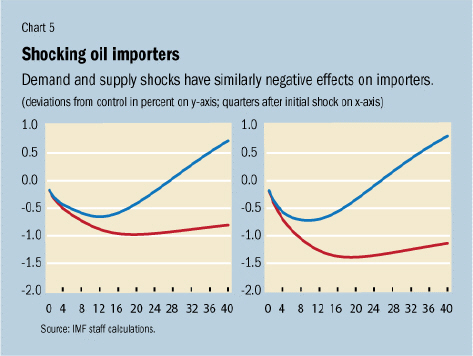

Simulations of the IMF’s large-scale models show that oil supply disruptions would reduce growth in the United States and Europe, an unwelcome prospect given already weak conditions in those economies.

An additional worry is that even oil price increases due to stronger demand from emerging markets may have negative, short-run effects in the current climate as the increased incomes and savings of oil exporters from the higher prices are not recycled immediately or fully into increased demand for goods produced by oil-importing countries.

Under normal conditions, the higher savings in oil exporters would also tend to lower global interest rates, in turn boosting the interest-sensitive components of demand in the oil-importing countries.

But in the current situation, where global interest rates are low, increased global savings are of little help, and oil price spikes would be even more unwelcome. The recycling of oil revenues does not work as well as before.

But many oil exporters are spending an unusually large amount of their revenues on imports of goods and services to improve social conditions in their countries, helping themselves and the global economy.