Workers crossing bridge at transportation center construction site in Anaheim, California, United States; the IMF predicts an environment of low real rates and cost of capital (photo: Bruce Chambers/ZUMA/Corbis)

World Economic Outlook Research

Continued low real interest rates—the rate paid by borrowers minus the expected rate of inflation—will ease the burden of debt for borrowers but can also tie the hands of policymakers. A low real interest rate environment also enhances the chances that in the future the nominal policy rate may hit the lower bound (that is, zero), thereby losing a key monetary policy tool: lowering interest rates to stimulate growth. Because there is a risk that advanced economies will encounter continued very low growth, this limitation may materialize.

Any increase in current real interest rates is expected to be modest because the main factors contributing to the decline in real rates are unlikely to be reversed:

• Saving: emerging market economies’ saving rate increased significantly between 2000 and 2007, driving down interest rates. This increase is expected to be only partly reversed.

• Portfolios: since the financial crisis, demand for safe assets has increased—bonds over the increasingly risky stocks and other equity. This was also driven by reserve accumulation in emerging market economies. Unless there is a major unexpected change in policy, this trend is likely to continue.

• Investment: the decline in investment rates in advanced economies as a result of the global financial crisis is likely to persist.

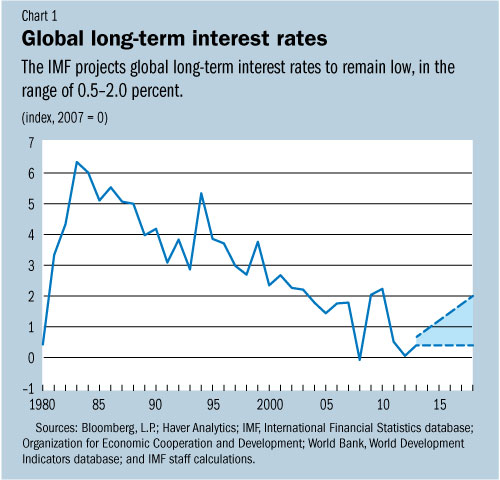

Since the early 1980s, interest rates, or yields, on assets of all maturities have declined worldwide, well beyond the decline in inflation expectations. This means that real interest rates—the rates paid by borrowers corrected for expected inflation—have declined. Ten-year real interest rates across countries fell from an average of 5½ percent in the 1980s to 3½ percent in the 1990s, 2 percent over 2001–08, and 0.33 percent between 2008 and 2012 (Chart 1).

With increased global economic and financial integration over the past three decades, real rates are now largely determined by common global factors, especially at longer maturities.

While monetary policy dominated the evolution of real rates in the 1980s and early 1990s, improved fiscal policy in advanced economies was the main factor underlying the decline in real interest rates during the rest of the 1990s. More recently, however, the factors mentioned above have played a crucial role.

In our study we construct a new data set of real interest rates for a wide set of countries to examine these factors in detail and predict the future of real interest rates and, more generally, the cost of capital.

Saving glut and investors’ preferences

The decline in real interest rates in the mid-2000s has often been attributed to two factors:

• a glut of saving stemming from emerging markets economies, especially China; and

• a shift in investors’ preferences toward fixed income assets—such as bonds—rather than equity, such as stocks.

Both these factors put downward pressure on real interest rates globally while the expected return to invest in equities increased.

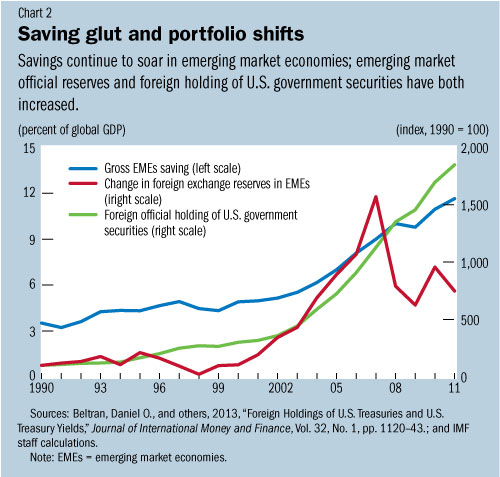

The substantial increase in saving in emerging market economies, especially China, in the middle of the first decade of the 21st century was responsible for more than half of the decline in real rates (Chart 2). This was only partly offset by the reduction in saving in advanced economies. High-income growth in emerging market economies during this period seems to have been the most important factor driving the increase in savings.

More than half of the reduction in real rates in the first decade of the 21st century can be attributed to an increase in the relative demand for bonds. This shift reflected an increase in the riskiness of equity combined with higher demand for safe assets among emerging market economies to increase official foreign reserves accumulation. In the aftermath of the global crisis, both reasons have continued to contribute to the decline in real rates, albeit more moderately now.

What to expect

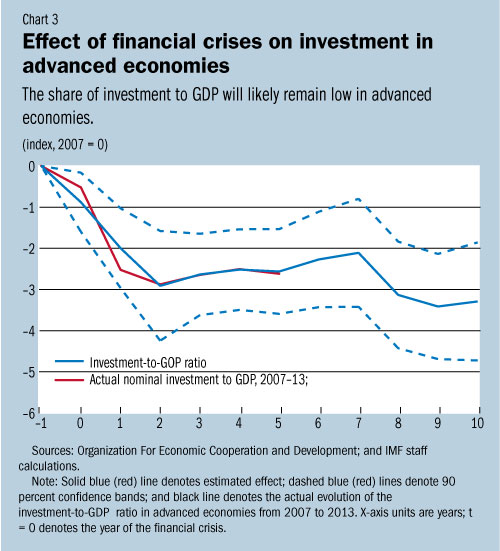

Scars from the global financial crisis resulted in a sharp and persistent decline in investment in advanced economies. This too contributed significantly to the recent decline in interest rates. The effects of the crisis on saving have been more muted. Our study finds that the effects of the global financial crisis will likely persist over the next 5 years, with investment-GDP ratios in many advanced economies unlikely to shift back to precrisis levels (Chart 3).

Part of the reason for the moderate expected increase in real interest rates and the cost of capital is cyclical: the extremely low real rates of recent years reflect a large shortfall between actual and potential output in advanced economies. The study suggests, however, that real rates and the cost of capital are likely to remain relatively low even when such gaps disappear.

In terms of policy, if real interest rates are lower than real GDP growth rates, increasing public investment may not lead to increases in public debt-to-GDP ratio in the medium term: higher growth would be financing the burden of the extra debt.

In relation to monetary policy, a period of continued low real interest rates could mean that the neutral policy rate (that is, a rate consistent with potential growth) will be lower than it was in the 1990s or the early 2000s. It could also increase the probability that the nominal interest rate will hit the zero lower bound in the event of adverse shocks to demand with inflation targets of around 2 percent. This, in turn, could have implications for monetary policy.

Finally, an environment of continued low real (and nominal) interest rates may induce financial institutions to search for higher real (and nominal) yields by taking on more risk. This, in turn, may increase systemic financial sector risks and appropriate macro- and micro-prudential oversight will be critical for maintaining financial stability.

â– The IMF will publish its global forecasts from the World Economic Outlook on April 8.