Loading component...

Fields in the Dnepropetrovsk region, Ukraine. Inefficiently managed resources, including agricultural land, remain a drag on growth (photo: Roman Kharlamov)

Ukraine Receives IMF Support But Must Accelerate Reforms

April 4, 2017

Fields in the Dnepropetrovsk region, Ukraine. Inefficiently managed resources, including agricultural land, remain a drag on growth (photo: Roman Kharlamov)

April 4, 2017

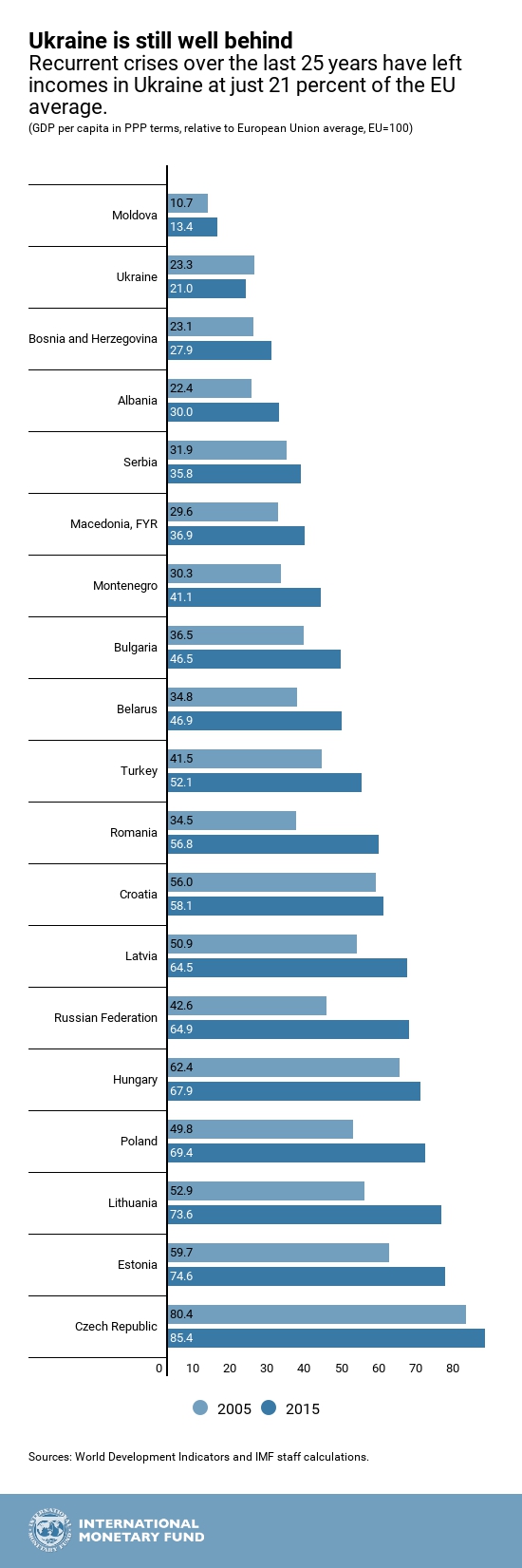

Ukraine receives a $1 billion installment of its $17.5 billion financial support for the reform program of the government, following the IMF’s review of the state of the country's economy. While the economy is slowly recovering after a severe crisis in 2014-2015, the country must still break with a legacy of weak governance and stop-and-go reforms to generate the sustainable growth it needs for higher incomes and better social conditions.

“The economic and social costs of the crisis have been high,” said the IMF mission chief for Ukraine, Ron van Rooden. “The government has undertaken important reforms under very difficult circumstances, but it has to do much more to recover the lost ground, to bring incomes closer to those in the neighboring states, to improve social conditions, and to build a modern market economy.”

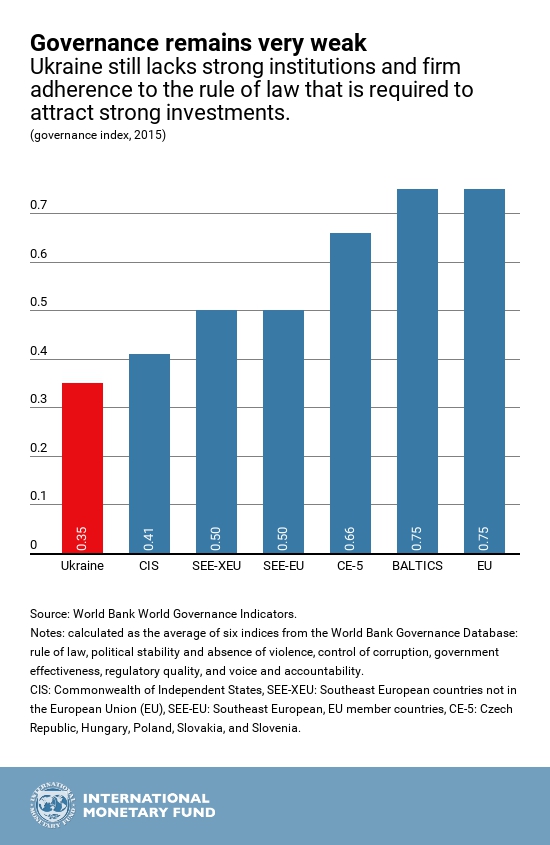

The IMF staff report notes that the pace of structural and governance reforms must accelerate. “Without this, it is hard to see the country achieving the stronger economic growth it needs. The government should work on building the necessary support from society for these important reforms,” said van Rooden.

The worst is over …

An independent central bank has successfully brought down inflation from its peak of 60 percent and has allowed the local currency to move in line with market forces. Meanwhile, the government has made great strides to reduce the economic vulnerability of the country and has implemented some important structural measures:

… but reforms must accelerate

To speed up growth that will allow Ukraine to catch up, the government has to act on the following challenges:

The IMF therefore urges reform and transparent privatization of state-owned enterprises, agricultural land reform to lift the moratorium on land sales, a comprehensive pension reform, including an increase in the effective retirement age to ensure the viability of Ukraine’s pension system and the ability to provide adequate pensions over time, and accelerated efforts in fighting corruption to achieve concrete results.

Background

Ukraine’s relatively weak economic performance is a legacy of an incomplete transition to a market economy after the break-up of the Soviet Union and a poor business climate. In addition, underlying macroeconomic problems, political upheaval, and the military conflict in the east led to a severe economic and financial downturn in 2014-2015, with output contracting by one quarter in a timeframe of twelve months. In April 2014, the IMF approved a two-year program, which was converted into a four-year program in March 2015, with a credit line totaling $17.5 billion, to help steer Ukraine back onto a sustainable and inclusive growth path. The government, on its part, took tough measures to stabilize the economy, but progress in structural reforms has been mixed. The current comprehensive economic health check conducted by the IMF is the first since 2013.

| Main Indicators of Ukraine |

|||||

|

|

2014 |

2015 |

2016 |

2017 |

2018 |

|

GDP growth (percent change) |

-6.6 |

-9.8 |

2.3 |

2.0 |

3.2 |

|

Inflation |

24.9 |

43.3 |

12.4 |

10.0 |

7.0 |

|

Public debt (percent of GDP) |

70.3 |

79.7 |

81.2 |

89.8 |

85.3 |

|

Current account balance (percent of GDP) |

-4.2 |

-0.3 |

-3.6 |

-3.7 |

-3.0 |