Europe's Economic Outlook in Six Charts

November 8, 2018

Europe’s economy continued to expand in the first half of 2018, although at a slower-than-expected pace, specifically in advanced Europe. Driven by domestic demand, economic activity continued to expand in the first half of 2018, the IMF said in its latest health check of Europe’s economy. But the outlook is less favorable, with several forces likely to hamper economic growth.

Here are six charts which tell the story of Europe’s economic health and its prospects for the near- and medium-term.

Related Links

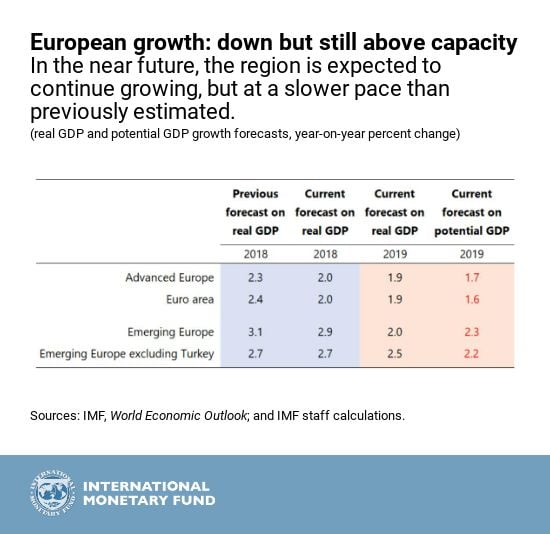

- Unmet growth expectations. Europe has seen strong growth over the past couple of years as many risks did not materialize. The region continues to enjoy respectable growth fueled by domestic demand, supported by high employment and wages. Still, the economy expanded at a slower pace than originally predicted. The region’s economy is now forecast to slow from 2.8 percent in 2017, to 2.3 percent in 2018, and 1.9 percent in 2019.

-

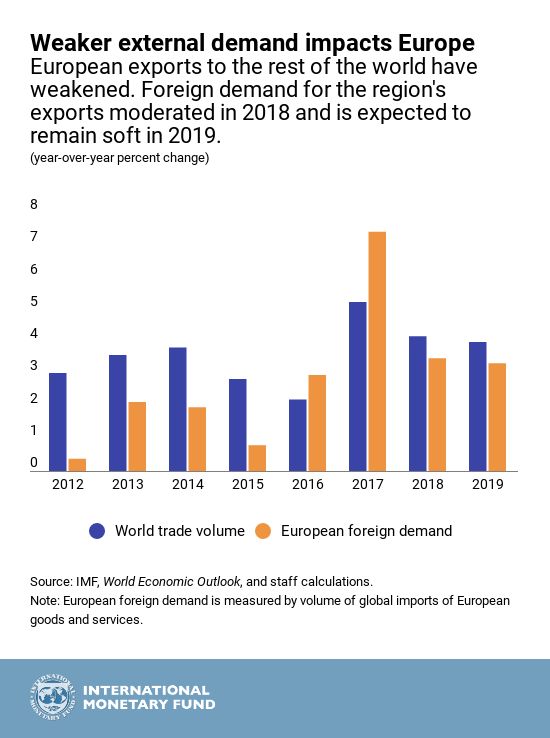

The environment has become less supportive for growth. There are several trends hampering growth. First, external demand (especially for goods) has dropped. Second, higher oil prices have dampened incomes. And third, production capacity constraints and labor shortages are becoming more pressing. These conditions are expected to persist. Also, risks to economic activity have increased.

-

Higher oil prices have dampened incomes: Over the last year, energy prices, including that of oil, have climbed. Commodity prices have increased 7 percent since the spring of 2018, while oil prices climbed to around $80 a barrel in September 2018. As a result, real disposable incomes fell, on average, by 0.5 percentage points of GDP in most of Europe. Oil producers, Norway and Russia, however, benefited from these developments.

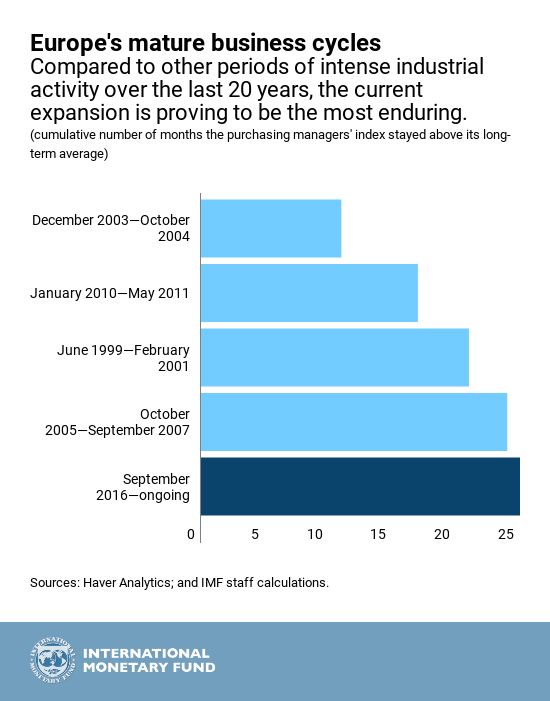

- A long period of manufacturing expansion. Europe’s manufacturing sector has enjoyed one of the longest periods of expansion over the last two decades. But against the background of a maturing business cycle, production capacity constraints, and labor shortages are constricting growth, especially in emerging Europe. Capacity utilization has now climbed to levels last seen before the global financial crisis.

- Outlook: Compared with the previous forecast by the International Monetary Fund, growth has been revised downward in about half of the countries in Europe. The downward revisions reflect weaker external demand and higher energy prices. Nevertheless, growth is expected to remain above potential in most countries in the region.

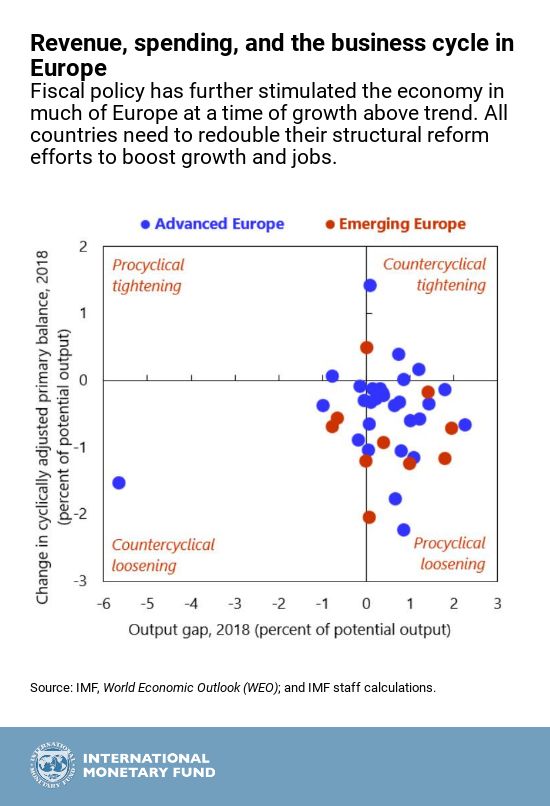

- Tax and Spending. Authorities in the region have largely chosen fiscal policies that are further stimulating the economy during the current period of economic expansion above trend. Consequently, deficits have remained relatively large despite years of strong growth. Policymakers should seize the opportunity offered by continued growth and low unemployment to advance growth-friendly policies to reduce high levels of public debt and rebuild resources for future rainy days, suggests the IMF. It is time for vulnerable countries to reduce their deficits and lower their debt. All countries need to redouble their structural reform efforts to boost growth and jobs.