The Brandenburg Gate in Berlin, capital of Germany. The country’s economy slowed in 2018 but is expected to return to trend in 2019. (photo: Ralph Hirshberger/Newscom)

Five Takeaways from Germany's Economic Outlook

July 10, 2019

Germany’s economic performance has been strong for the past decade, with the unemployment rate currently at a record low, and healthy public and private balance sheets. But the export-dependent economy has been hit hard by the slowdown in global demand, while structural challenges are looming in the medium term. At the same time, external imbalances remain large, partly reflecting the uneven distribution of the gains from growth.

Related Links

Here are five key takeaways from the latest staff report on Germany, summarizing the economic context and outlook, as well as the IMF's main policy recommendations.

-

Growth: After several years of real GDP growth averaging over 2 percent annually, Germany’s economy slowed sharply in the second half of 2018. This reflected a mixture of weak external demand and special circumstances affecting the auto and chemical industries. Solid investment in construction and equipment is projected to gradually bring output back to trend by the end of this year, resulting in 0.7 percent growth in 2019 and 1.7 percent in 2020.

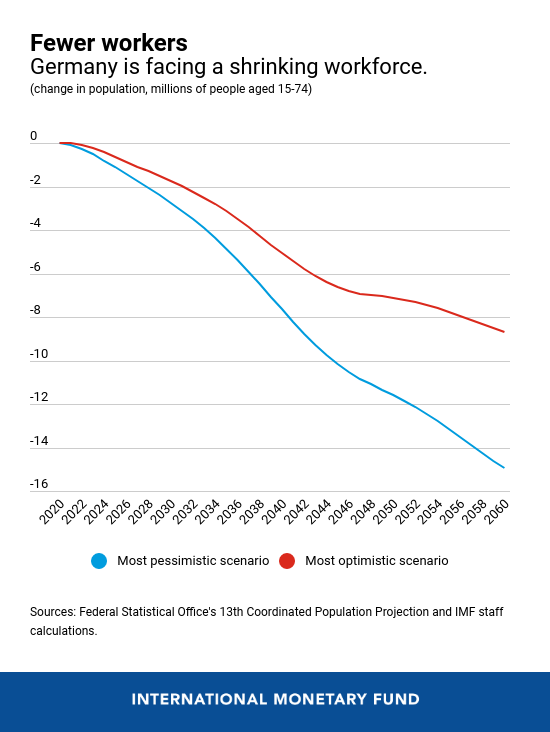

Looking ahead, structural challenges are weighing on Germany’s potential output. Soon, the labor force is expected to shrink as the population ages, while productivity growth remains low. Adaptation to technological change and digitalization is slow, while the energy transition poses important uncertainties for business investment.

-

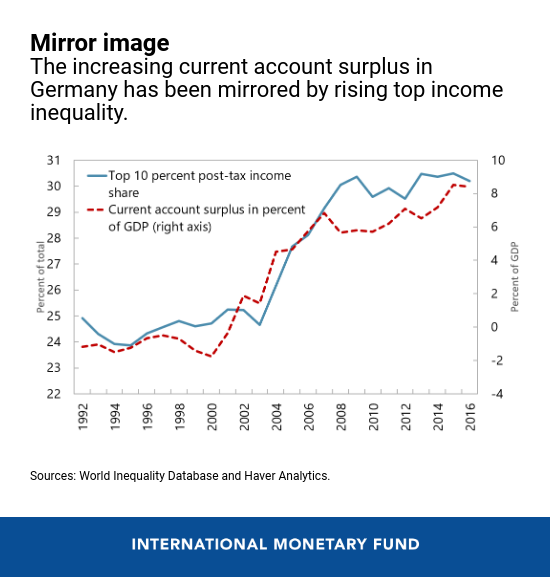

Current Account: Rising saving by firms, together with fiscal consolidation after 2011, fueled the rise in Germany’s current account surplus. For much of the past two decades, as unemployment fell, and exports surged, wage growth lagged behind and household purchasing power stagnated, particularly among the lower paid.

Reflecting this, a rising share of national income took the form of profits retained by firms, whose ownership is highly concentrated among the wealthiest households. As these households tend to save a larger share of their income, private saving increased and the current account surplus surged.

-

Fiscal policy: With many consecutive years of large fiscal surpluses, and the public debt ratio on a declining path, Germany’s fiscal space is substantial. This fiscal space should be used fully to support potential growth through public investment in physical and human capital, and to provide further tax relief for low-income households which, along with stronger wage growth, would restore their purchasing power. These policies would boost potential growth, and help reduce external imbalances.

-

Structural reforms: With the working-age population set to decline and widespread labor shortages, reforms to raise productivity and domestic investment are key to sustaining growth going forward. The focus should be on upgrading coverage of nationwide high-speed internet, rolling out the e-Government platform, supporting venture capital, and reducing uncertainties around the strategy for an ambitious energy transition program.

-

Financial sector: Amid the “low-for-long” interest rate environment, the German banking system needs to accelerate measures to shore up profitability, which has been persistently under pressure from high costs and slow progress with restructuring. Faster restructuring should be accompanied by an expanded macroprudential toolkit and enhanced data availability to address rising macro-financial risks.