As prepared for delivery:

Thank you for the introduction. It is a great honor to participate in this event, hosted by the National Bank of Romania. Governor, on behalf of my IMF colleagues, let me thank you and your colleagues for the hospitality, and not only for this event but also during many years of close collaboration.

In my remarks, I will discuss our latest outlook for Europe and highlight the key policy priorities for 2021.

Last year the pandemic caused the worst peacetime global contraction since the Great Depression. The crisis had a huge impact on lives and livelihoods. With a new wave of infections since the fall, with mutations of the virus becoming more prevalent, and with renewed, necessary lockdowns across Europe, it is clear that we are still in the middle of the crisis. The situation remains challenging and highly uncertain. There is light at the end of the tunnel, though, with a growing number of highly effective vaccines developed, production increasing, and vaccinations of populations accelerating. However, it will remain an uncertain race between vaccinations and the virus.

An exceptionally strong economic policy response has played a crucial role in cushioning the pandemic’s impact thus far. The policy strategy was appropriately geared towards preserving the structure of the economy and the fabric of society. This strategy was aimed at creating a bridge to the post-pandemic recovery and preventing long term damage to the economies. This was the right thing to do: People, jobs, and businesses were protected. And we already got a preview at how this policy strategy is to work—when economic activity bounced back vigorously in the third quarter of 2020 after the first wave of infections.

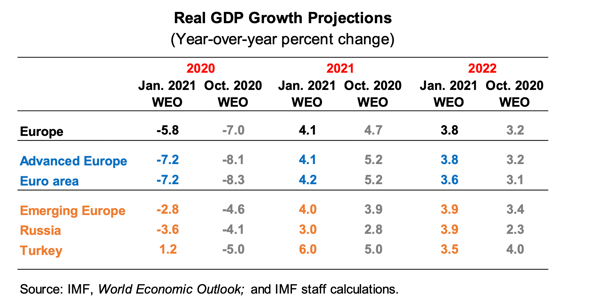

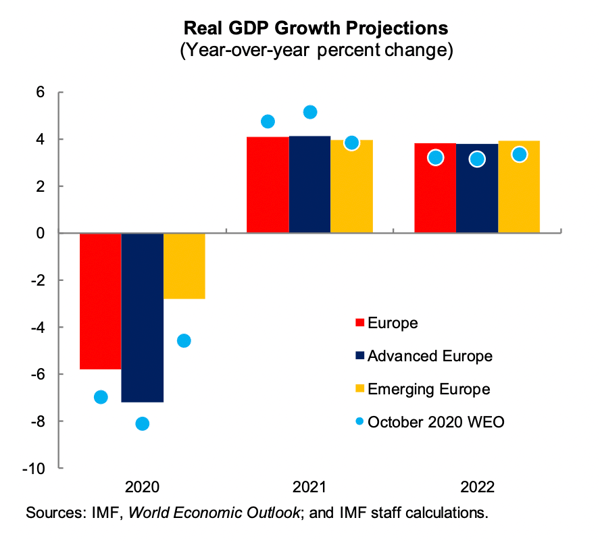

Indeed, the rebound in the third quarter of last year exceeded our expectations significantly. We thus upgraded our 2020 growth estimate for Europe in the January WEO Update. We estimate that activity in Europe contracted by about 6 percent in 2020, a contraction that is 1 percentage point smaller than previously projected. For emerging Europe, GDP contraction in 2020 is now estimated at 2.8 percent, almost 2 percentage points smaller than in the previous forecast.

For 2021, we expect a strong economic recovery in Europe, albeit uneven and partial. Growth is projected at 4.1 percent for Europe and 4.0 percent for emerging Europe. For Romania we project that after contracting by about 5 percent in 2020, it will expand by a bit more than the emerging-Europe average.

Surging infections in late 2020, including from new variants of the virus, proved however worse than expected. While emerging Europe had a relatively light blow from the first wave, the pandemic’s health and economic impact have become more similar across Europe since the second half of 2020. Even though recent data show more resilience of economic activity to lockdowns than in the spring—as people and the economy have adapted—our GDP growth projection for 2021 was revised down by 0.6 percentage point relative to the October forecast, reflecting in part this winter’s widespread lockdowns. Nevertheless, the output level at end-2021 is still projected to be higher than in the October WEO projections, because of the better outturn in 2020.

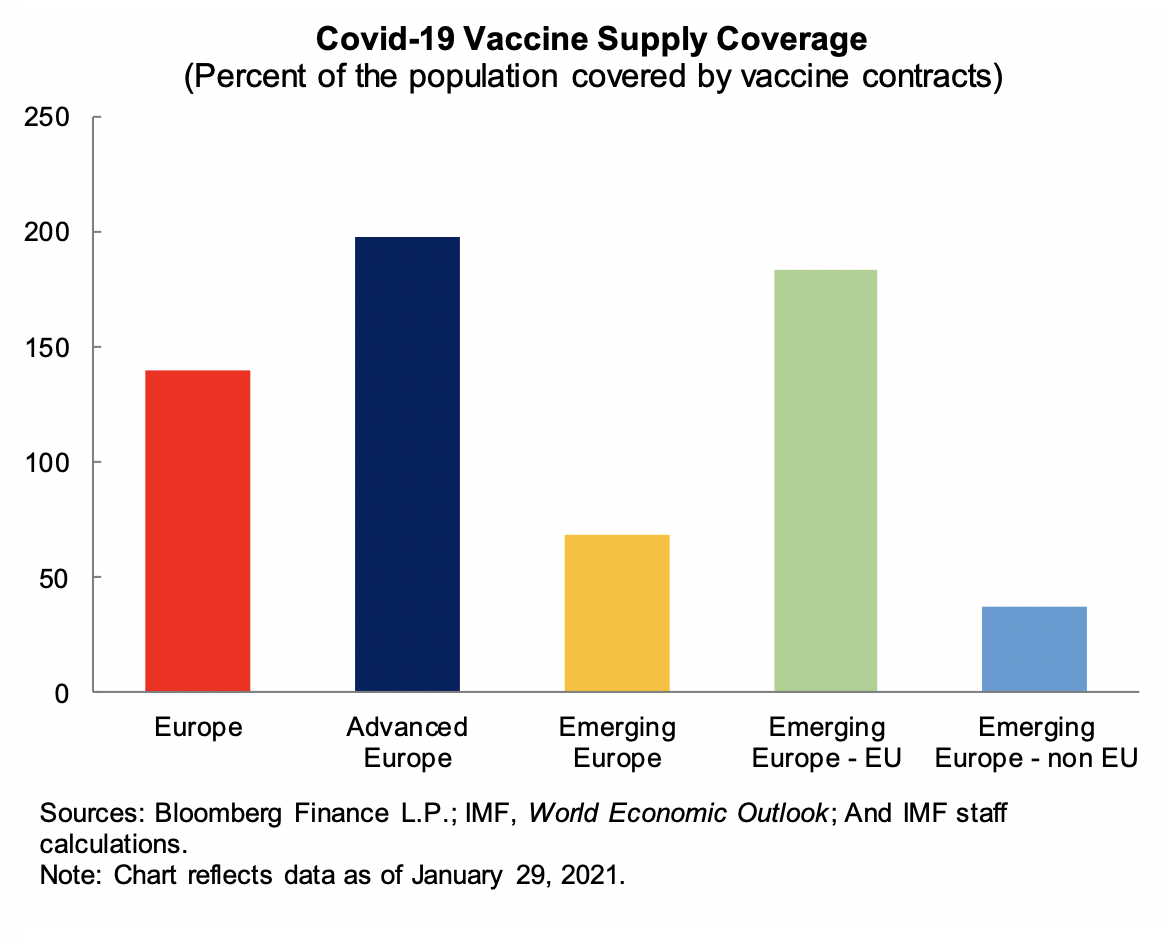

As I pointed out, the game changer for 2021 are vaccines. Consistent with announced plans of the EU and other countries, we assume broad vaccine availability in advanced economies and several emerging economies by the summer of 2021. For many other emerging economies, including in Europe, making vaccines broadly available will take longer.

While we are currently seeing inevitable start-up problems in the production and rollout of vaccines, a key concern is the particularly large divergence of non-EU emerging economies. While vaccination in some non-EU countries is progressing at the average EU speed or even faster, others are facing a significant challenge with securing vaccine supply of an adequate amount. They could benefit from a more effective global coordination to accelerate the vaccine production and its distribution. Let me note here that Romania’s vaccination rate has been one of the highest in Europe lately.

Now let me move to the policy priorities for 2021. We see three:

First, given the race between a mutating virus and vaccinations, a clear priority for this year is to scale up the production of vaccines and accelerate their rollout globally.

Second, we need to maintain economic policy support and thereby continue to bridge economies until widespread vaccinations and herd immunity allow the return to a new normal. It is thus critical to continue supporting people and businesses strongly affected by the pandemic. Emerging Europe should build on its robust policy support in 2020, which in some areas approached the level of advanced Europe, albeit after a slow start. For the fiscal policy response, we estimate that in 2020 discretionary policies and automatic stabilizers provided support of about 8 percent of GDP in advanced European economies and 6 percent of GDP in emerging Europe excluding Turkey and Russia.

And third, once the recovery becomes entrenched, policies will need to transition from providing general lifelines to supporting those firms with good post-pandemic viability prospects, and help the transition of workers from sectors that may permanently decline in the aftermath of the pandemic to those that will expand.

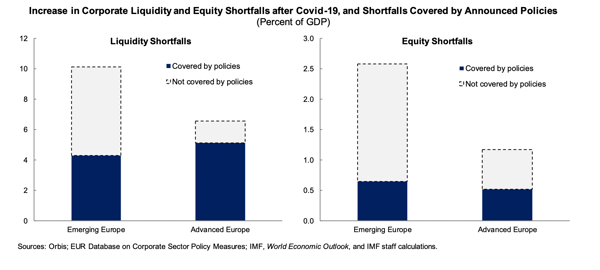

Corporate sector policies, the theme of today’s conference, have played a critical role and will play a critical role in the transition. Without the already deployed policy measures, a large share of firms—accounting for 15 percent of employment and about 25 percent of value added of the corporate sector—would have been unable to cover expenses, with liquidity pressures pushing many into bankruptcy.

But more needs to be done to help firms, especially in emerging Europe. Support for the corporate sector has been more effective in covering liquidity shortfalls, while additional equity support is necessary to stabilize viable firms—including during a prolonged recovery phase. We estimate equity gaps in Europe at around 2½ percent of GDP.

With this, I now look forward to our discussion on how to improve the scale and effectiveness of policies to support the corporate sector.