Luxembourg - Staff Concluding Statement of the 2021 Article IV Mission

March 15, 2021

A Concluding Statement describes the preliminary findings of IMF staff at the end of an official staff visit (or ‘mission’), in most cases to a member country. Missions are undertaken as part of regular (usually annual) consultations under Article IV of the IMF's Articles of Agreement, in the context of a request to use IMF resources (borrow from the IMF), as part of discussions of staff monitored programs, or as part of other staff monitoring of economic developments.

The authorities have consented to the publication of this statement. The views expressed in this statement are those of the IMF staff and do not necessarily represent the views of the IMF’s Executive Board. Based on the preliminary findings of this mission, staff will prepare a report that, subject to management approval, will be presented to the IMF Executive Board for discussion and decision.

Washington, DC: Luxembourg has weathered the pandemic relatively well, thanks to the unprecedented policy support, both domestically and globally, and a quick adjustment to teleworking given the structure of the economy. To support the economy, the government implemented a large and multi-pronged policy package in 2020, followed by more targeted stimulus in 2021. IMF staff project a rebound in output this year, with risks tilted to the downside, including due to the virus dynamics. Accordingly, fiscal policy should remain supportive and become more targeted towards the most vulnerable as the recovery gains speed to avoid an increase in inequality. As pandemic-related measures are unwound, and taking advantage of the ample fiscal space, policy support should increasingly pivot towards greening the economy while maintaining high levels of public investment to close infrastructure gaps. The welcome steps to consolidate Luxembourg’s position as a sustainable finance hub should continue. Rising risks in the financial sector, while manageable, should be further closely monitored and addressed in line with the 2017 FSAP recommendations. Structural policies should focus on reducing scarring effects in the labor market and improving inclusiveness in the housing market.

Context

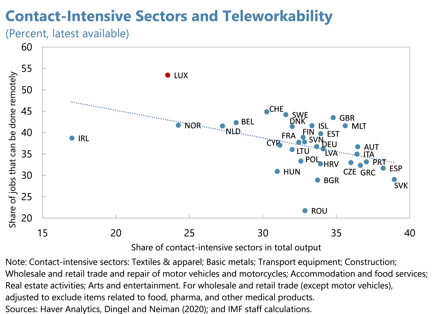

Luxembourg has managed the COVID-19 pandemic relatively well thanks to a vigorous policy response. The economy, dominated by financial services, adapted quickly to teleworking. Sizeable and flexible policy support and quick reopening of the economy—underpinned by a large-scale testing and tracking strategy—helped attenuate the economic fallout from the pandemic. While the economy has fared much better than the euro area, it still contracted last year driven by weak domestic demand.

Utilizing accumulated fiscal space, the government response was decisive, with measures rapidly adjusted as the situation evolved. At the onset of the pandemic, the government implemented a large package of emergency measures focused on solidarity to provide critical support to households and firms. This was followed by a stimulus package appropriately consisting, among others, of more targeted measures to the most affected sectors. These measures, together with the unprecedented global policy support, underpinned a sharp economic rebound in the second half of 2020, keeping unemployment down and resulting in lower uptake of the key measures for the year.

The outlook is for a recovery with risks tilted to the downside. Following a mild GDP contraction of 1.3 percent in 2020, IMF staff anticipate a rebound in 2021, with GDP increasing around 4½ percent amid continuing targeted policy support and accommodative global financial conditions. Over the medium term, output is forecast to remain slightly below the pre-crisis trend, partly reflecting some impairment in corporate balance sheets and scarring in the labor market. Risks to the outlook are skewed to the downside and are dominated by the virus dynamics in the near term. On the upside, quicker containment of the infection could bring back activity significantly faster. On the downside, a prolongation of the health crisis into 2021 could delay the recovery. Broader risks, such as tightening of financial conditions, the acceleration of de-globalization, and potentially non-negligible revenue loss from changes in international taxation, could weigh on economic prospects.

Fiscal policy: Supporting a strong, sustainable, and greener recovery

Fiscal policy should remain supportive until a firm recovery is underway, increasingly focusing on the most vulnerable as the recovery gains speed. The fiscal stance remained adequately flexible, with key policy measures extended until mid-2021 and targeted more towards the most impacted. Given the unprecedented nature of the crisis and the exceptional uncertainty, fiscal policy should continue to be supportive and well communicated. Fiscal normalization should be state contingent and start only when output has broadly recovered to its pre-COVID level. The unwinding of the policy support should be carefully calibrated against the evolution of the pandemic and economic conditions. Subsequent measures should continue to be targeted to the most vulnerable, including lower-income households and firms in the most affected sectors. Luxembourg’s well-developed safety nets have proved instrumental in protecting the most vulnerable during the pandemic. Accordingly, allowing automatic stabilizers to fully operate would continue to support those groups, while unwinding the extraordinary policy measures.

Drawing on its fiscal space, Luxembourg should proceed with greening the economy and maintain high levels of public investment to close infrastructure gaps. Luxembourg should move forward with its National Energy and Climate Plan, building on the welcome steps taken in the 2021 budget. These include the introduction of a carbon tax, accompanied with a tax credit to mitigate the impact on the most vulnerable, the reduction of the subscription tax for sustainable investment funds, and the provision of additional incentives for green investments. Leveraging its status as a global financial center, Luxembourg has taken welcome steps to consolidate its position as a sustainable finance hub. Luxembourg should continue the transition to a data-driven economy by accelerating the digitalization of public services and further incentivizing business investment. It should also continue to close physical infrastructure gaps (such as in transportation) by maintaining a high level of public investment spending in line with the government’s multi-year spending plan.

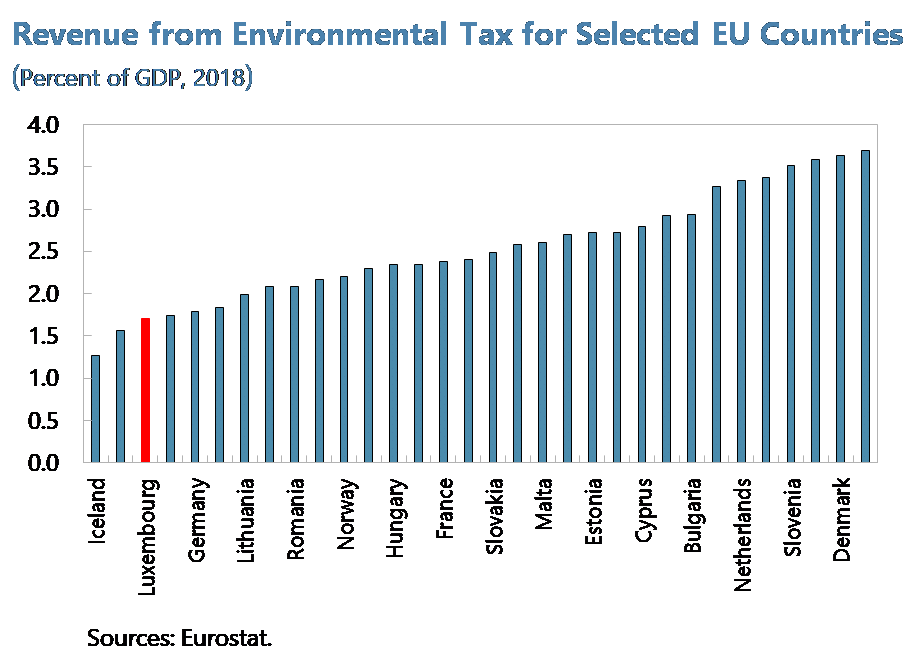

Given non-negligible fiscal risks, Luxembourg should preserve comfortable buffers, explore options to diversify revenues, and improve public investment efficiency. The welcome steps taken by Luxembourg to comply with the EU and international transparency and anti-tax avoidance initiatives could help strengthen the corporate tax base. However, there are signs that these initiatives—along with revisions in the U.S. tax system—are affecting large multinational enterprises in a way that may reduce tax revenues in Luxembourg. Efforts needed to meet climate change mitigation targets, especially for road transportation, may also pose potentially non-negligible revenue loss due to lower sales of fuel and complementary goods. Against this background, Luxembourg should continue exploring ways to diversify revenues. These include increasing environmental levies (such as the low transport taxes) and housing taxation (such as outdated property valuations). To safeguard public resources, efforts to enhance public investment management should continue, including the introduction of independent and systematic ex-post project evaluations. Staff welcome the authorities’ readiness to further strengthen the effectiveness of the public procurement framework, including of COVID-related spending. To this end, staff encourage the collection and publication of information on beneficial ownership of winners of public tenders.

Financial sector policies: Addressing rising vulnerabilities and risks

While firms and households were shielded by the unprecedented policy support in 2020, the pandemic could weigh on their balance sheets. Liquidity support measures—especially the short-time work scheme—together with favorable lending conditions helped alleviate potentially costly vulnerabilities concentrated in the sectors most exposed to the pandemic (notably wholesale, retail, and hospitality). Going forward, liquidity pressures could intensify and may turn into insolvencies should state support be withdrawn prematurely or recovery delayed. Emergency policies also helped preserve employment and cushion the income shortfall for households in 2020. However, in the event of a significant rise in unemployment due to a sustained economic slowdown, household debt repayment capacity could weaken. Lower-income households who exhibit higher indebtedness and lower liquid asset holdings are the most vulnerable to cliff-edge risks from a premature ending of government support.

Rising risks in the banking sector, while manageable, should continue to be closely monitored and addressed in line with the 2017 FSAP recommendations. The sector remained well capitalized and liquid overall. While solvency risks have not materialized so far, higher provisions are weighing on bank profitability, but will alleviate the impact of potential credit losses. Staff analysis suggests that, overall, the domestically oriented banks would remain resilient even in an adverse scenario, but results vary among banks. Accordingly, continued vigilance is required as asset quality deterioration could weigh on already weak bank profitability, especially if the health crisis persists. The existing structural profitability issues in certain segments of the banking sector (such as high reliance on capital market developments and relatively low cost-efficiency) should continue to be monitored.

The pandemic illustrated the investment fund sector’s growing vulnerabilities, warranting a further deepening of the sector’s macroprudential-based surveillance and regulation. The investment fund sector weathered the crisis well thanks to decisive global policy action and robust oversight. Faced with large price corrections and an increase, albeit limited, in redemptions during the March 2020 market turmoil, overall, Luxembourg funds increased their holdings of cash and liquid assets, which led to a procyclical selling of assets. After the March turmoil, underpinned by a renewed search for yield, investment funds reverted to their pre-pandemic trend of increasing liquidity, maturity, and currency mismatches, as in other jurisdictions. As a result, investment funds—especially open-ended ones—remain prone to widespread outflows and procyclical selling of less liquid assets in a market downturn, warranting continued action in line with the 2017 FSAP recommendations. Building on welcome efforts to step up the oversight of the sector from a system-wide perspective, the authorities involved in macroprudential policy should move forward with developing internal methodologies for system-wide liquidity stress testing. Also, they should remain proactive in international fora to push forward the macroprudential reform agenda.

Notwithstanding the pandemic, the authorities rightly tightened somewhat the macroprudential stance as risks in the real estate market continued to rise. The introduction of differentiated loan-to-value (LTV) limits to curb the increasing household indebtedness, amid fast-growing house prices and mortgages, is a step in the right direction. If household indebtedness continues to increase, the current LTV setup should be revisited, and/or other tools provided in the legal framework for borrower-based measures explored. The authorities also appropriately maintained the counter-cyclical buffer unchanged, given the current credit cycle position. As the recovery firms and should credit market pressures reemerge, partly due to the lower-for-longer interest rates, some tightening of the macroprudential stance may help alleviate these pressures.

Structural policies: Mitigating scarring effects and ensuring inclusive recovery.

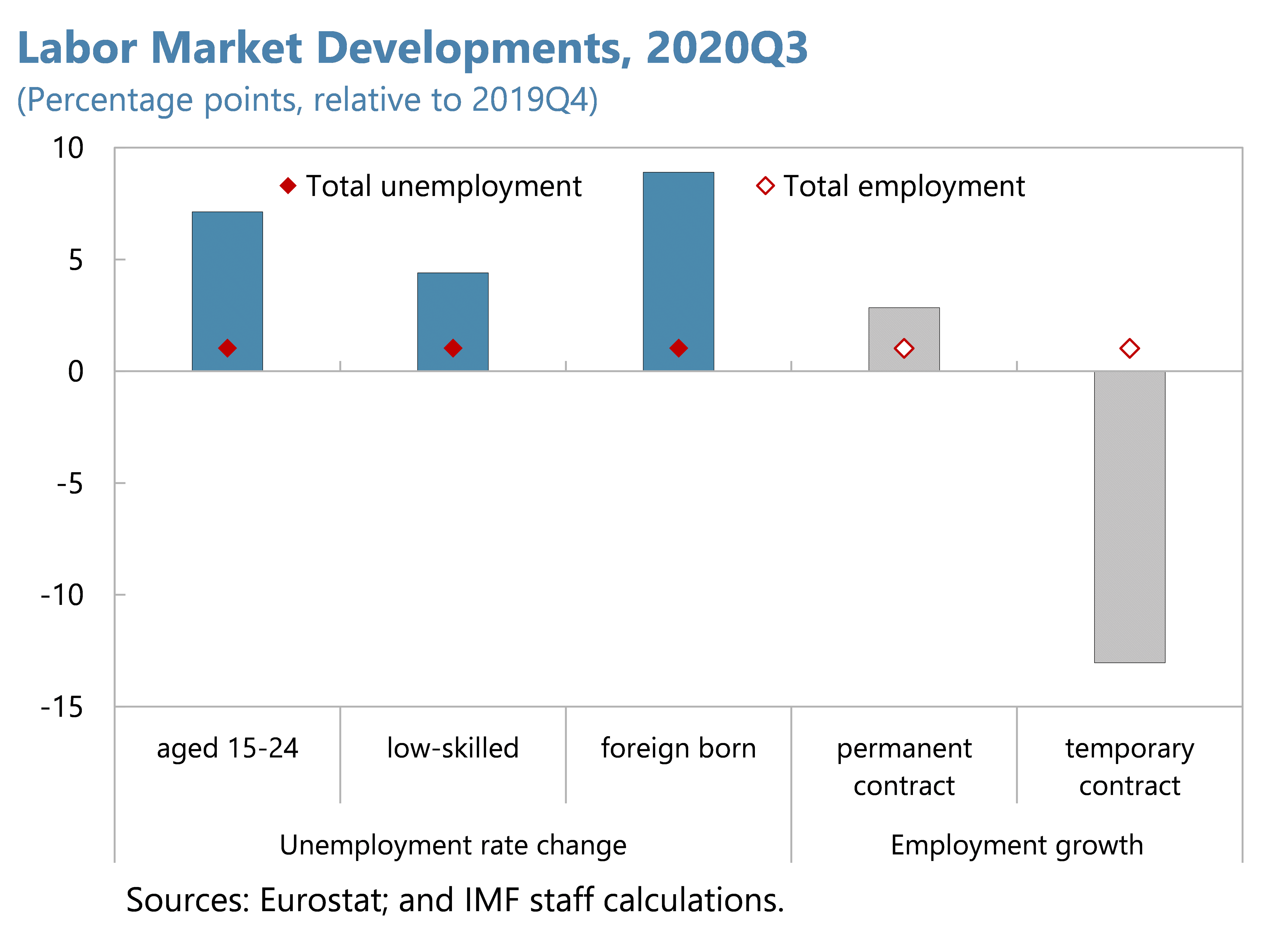

As the recovery firms up, policies should shift from preserving jobs to helping workers, especially among the most vulnerable groups, to facilitate labor reallocation. Based on Eurostat data, the pandemic seems to have disproportionately affected vulnerable workers, and led to rising unemployment among the youth, low-skilled, and foreign born who already struggled to integrate into the labor market prior to the crisis. The extension of the expanded short-time work scheme until mid-2021 is welcome and will partly address a possible increase in inequality. Once the recovery is firm, labor mobility within and across sectors should be promoted through hiring subsidies for viable firms—such as subsidies for employer-sponsored apprenticeships—to facilitate the reallocation of workers from shrinking to expanding firms and sectors. Building on recent initiatives such as Future Skills, Luxembourg should continue to support training programs to upgrade skills and promote the reintegration of the crisis-hit workers into the labor market.

Steps taken in 2020 to improve housing supply are welcome and should be followed up with further actions to improve inclusiveness in the housing market. The disproportionate impact of the pandemic on vulnerable groups, in conjunction with rising house prices, make the availability of affordable housing supply even more pressing. In 2020, the government rightly took steps to improve the supply of affordable housing. For example, the Pacte Logement 2.0 will, among others, link subsidies allocated to municipalities to the amount of social housing built. In addition, the 2021 budget includes welcome measures intended to discourage speculation in the real estate market and support rental supply (such as by lowering the depreciation rate for rented properties). These efforts should continue, including modernizing the rigid urban zoning/planning and updating the communal development legislation to increase the supply of buildable land.

The IMF team would like to thank Luxembourg authorities and other interlocutors for constructive and insightful discussions.

IMF Communications Department

MEDIA RELATIONS

PRESS OFFICER: Wafa Amr

Phone: +1 202 623-7100Email: MEDIA@IMF.org