The Evolving Role of Central Banks in Africa

June 7, 2024

Good Morning!

I am truly honored to address you all today, especially on this special occasion commemorating the 60th Anniversary of the National Bank of Rwanda.

Isabukuru nziza yimyaka mirongo itandatu kuri Banki nkuru yu Rwanda!

As something of an observer of recent African economic history, I will explore the transformative journey of African central banks over the past six decades. I will try and avoid making this just an academic exercise but rather use it to glean insights from our past to navigate the complexities of our current challenges. And given the time limitation, in covering this expansive topic, I will sacrifice depth for breadth

Central Bank’s Mandate in the African Context

Broadly, the core mandates of central banks around the world are twofold: maintaining price stability and oversight of the financial system. There are nuances of course. Famously, the US Fed, for example, also has the responsibility to promote maximum employment, in addition to price stability. But in the broadest of terms, the two objectives that I highlight here are by far the most common.

In the context of our countries, by and large, the formal and core mandate of central banks as outlined in central bank laws are very similar. For example, in the case of BNR its mandate is “maintain price stability, enhance and maintain a stable and competitive financial system, and support the government's general economic policies.” This is very typical for the region.

But operating as they do in a hugely complex and dynamic environment, central banks in our countries also have at least two more factors—even if informally—that they consider as they fulfill their core mandates:

- Fostering financial sector development—going well beyond the typical role of central banks, as elsewhere, needing to supervise and regulating banks and financial markets. In most African countries, financial deepening remains a major challenge. For one, access to banking services remains far from universal, even with the advent of fin tech for which the region has been doing rather well on in recent years. And beyond basic banking services financial intermediation still has ways to go.

- Central banks in the region are also implicated in governments’ quest for financing, both internally and externally. The extent of this varies from country to country, of course. But with domestic financial markets rather shallow in most of the region, some governments borrow directly from central banks. And even where that is not the case, in the region rare is the central bank that does not keep a keen eye on the cost of financing its fiscal authority is facing.

To be very clear, I am not arguing that these two considerations are the responsibility, much less part of central banks’ mandates in the region. Rather, inevitably and unavoidably, they feature prominently as central banks pursue their core functions in most developing countries.

How then have central banks fared in the pursuit of these responsibilities over the years?

Increasing Price Stability over Time

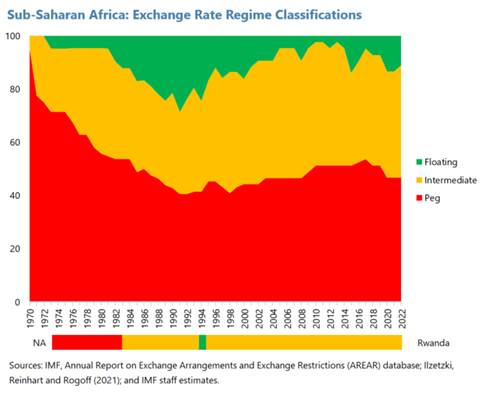

The journey of central banking in Sub-Saharan Africa has been one marked by resilience and transformation. Emerging from the shadows of colonial legacy, central banks in Sub-Saharan Africa started their journey in the early post-colonial era rigid fixed exchange rate and rule-based regimes, including currency boards. Through the course of the 1970s and early 1980s though, countries found themselves facing severe oil price shocks, floating exchange rates internationally, tight financing conditions and considerable political turmoil. Central banks were struggling to achieve multiple objectives. This included the onerous task of financing government deficits, precipitating rampant inflation and economic instability.

The 1990s heralded a new era of reforms geared towards more discretionary arrangements. Many countries initiated bold reforms to shift towards more flexible exchange rate systems and to reduce dependence on central bank financing of fiscal deficits. This pivotal shift wasn’t just about new monetary policies to curb deficit financing; it was about reshaping the economic landscape and laying the groundwork for stability and growth.

During this period and into the 2000s, financial sector reforms took center stage, with many countries modernizing and liberalizing their banking systems. Market-based interest rates were introduced, and independent regulatory agencies established. Moreover, regional integration initiatives, such as ECOWAS, EAC, and SADC, spurred efforts to harmonize financial regulations and promoted cross-border banking supervision.

The National Bank of Rwanda’s trajectory mirrors the evolution observed in much the rest of Africa. Since its inception in 1964, the BNR transformed from direct control measures to embracing market-based policies. From 1997, it shifted focus on price stability through innovative monetary targeting strategies, embracing flexible reserve programs and advanced forecasting techniques. By championing transparency, capacity-building, and market development, the BNR paved the way for its current forward-looking, interest rate-based monetary policy.

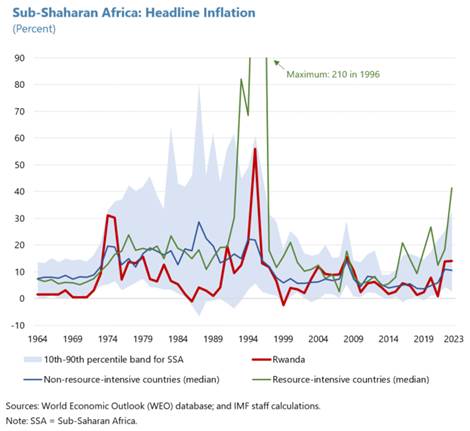

By the turn of the millennium, we began to witness the tangible benefits of central banking reforms across the SSA. Countries like Ghana, Uganda, Kenya, and Rwanda experienced sustained economic growth coupled with low and stable inflation, a testament to the efficacy of modernized monetary policy frameworks. More generally, inflation rates in sub-Saharan Africa have become less volatile compared to the 1980s and 1990s, especially for non-resource intense countries. Since the mid-1990s, we have also observed a downward trend in inflation due to improved monetary policies, greater exchange rate stability, and better policy cohesiveness. However, in resource-intensive countries, inflation remains relatively high due to structural factors like greater commodity dependence, weaker policy frameworks, and limited supply-side capacity.

Rwanda has achieved remarkable success in controlling inflation and safeguarding its currency's value through sound macroeconomic policies, including its interest rate-based monetary approach. This has ensured price stability and competitiveness. Rwanda's inflation rates have generally been lower than the regional average, and its real effective exchange rates have remained relatively stable compared to other Sub-Saharan Africa countries—a testament that its nominal exchange rate has been allowed to adjust to changing fundamentals. These policies have created a predictable environment, stimulated investment and long-term planning, while maintaining currency purchasing power, fostering economic confidence, and stability.

Engendering Financial Sector Development

I will now turn to discuss the issue of financial sector development. This encompasses expanding the use of existing financial instruments and embracing new ones to facilitate savings intermediation and risk management. Despite the region historically lagging in credit-to-GDP ratios, reforms since the 2000s have spurred gradual increases, supported by regulatory enhancements and competition promotion. These efforts yielded notable benefits, including enhanced banking sector performance and stability, deeper financial intermediation, and improved financial literacy. However, there is still ample room for growth, particularly in the realm of financial markets where progress has been less pronounced.

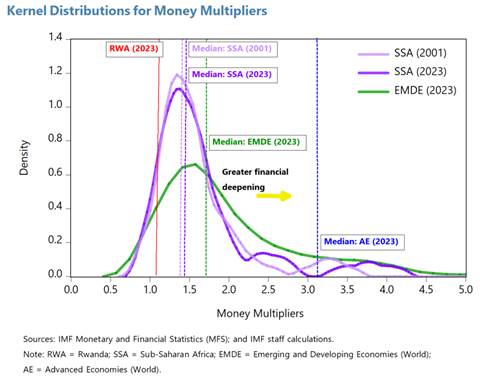

To further gauge progress in financial deepening, it is also useful to examine regional money multiplier trends. Higher multipliers in more developed financial systems signify banks' increased ability to lend efficiently, thus expanding the money supply. Evidence across Sub-Saharan Africa suggests varying effectiveness in supporting economic development, influenced by factors like banking competition, financial innovation, monetary policy frameworks, fiscal-monetary policy interactions, and exposure to global conditions. Despite recent strides, there remains substantial room for enhanced financial intermediation in the region, as median money multipliers lag behind those of emerging and advanced economies.

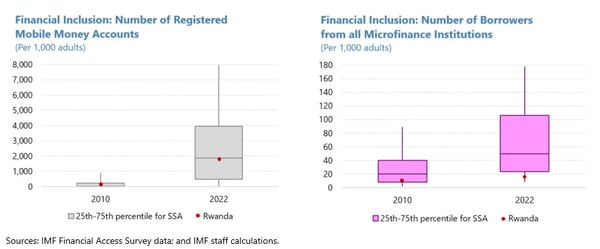

What is quite remarkable, on the other hand, is that the region is leading the world in innovative financial services based on mobile telephony. Mobile-based systems such as digital payments, digital savings, micro-insurance, peer-to-peer lending have boosted financial inclusion, especially in East Africa. Yet, there is a significant untapped potential in other countries, offering solutions to infrastructure and other shortcomings. Microfinance has also grown in some countries in SSA, aiding lower-income individuals. Conditional on solid regulatory frameworks, such innovations could cut costs, lessen cash dependence, and boost financial development in SSA economies.

I would like to acknowledge Rwanda’s impressive progress in bolstering its financial sector. Through regulatory and supervisory reforms, Rwanda has prioritized safeguarding financial stability, improved risk management, and refined monetary policy effectiveness. These efforts have facilitated prudent monetary policy conduct, increased credit availability for individuals and businesses, and demonstrated Rwanda's commitment to financial system development. The BNR has been instrumental in this journey, emphasizing financial stability, inclusion, and market deepening to foster sustainable economic growth.

Financing the Government

I would be remiss without touching on the issue of central bank lending to the government for fiscal purposes, something that many (but by no means all) central banks in the region have had to be involved in. It’s appropriateness has been an issue of much debate over the years. And recent economic developments have brought the matter once again to the fore. I am here talking about the funding squeeze many countries have been experiencing, as external financing conditions have tightened, domestic ones have followed, official development assistance declined, and tax revenue collection has been weak.

Excessive fiscal dominance has exacted a heavy toll in the region over the years, notably causing episodes of very high inflation, heightened economic uncertainty, and undermining investment and growth. Examples include DRC (1991-92, 1993-94, and 1998), Angola (1994-97), and Zimbabwe (2007-08, 2019-20). And short of 3-digit and/or hyperinflation levels, there are many other episodes of inflation accelerating to the 30-50 percent range in countries around the region—recent cases include Ethiopia, Ghana, and Nigeria. I want to be clear here and stress that by no means am I arguing that central government borrowing is the only reason for the spike in inflation. Rather, it is a predominant factor, with other, often exogenous shocks—for example, food price increases—and accommodative monetary conditions also contributing.

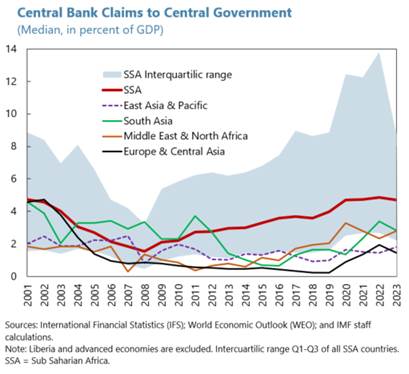

Over the years, legal constraints on central bank financing of fiscal debt have been implemented worldwide, including in our region, to address the risks of fiscal dominance. Despite this, central bank lending to governments remains a pressure point in sub-Saharan Africa. Recourse to central bank financing had started to drift to levels seen outside the region between 2000 and the global financial crisis—from 4 to 2 percent of GDP. But since then, borrowing from central banks has been trending upwards, and jumped a notch with the onset of the COVID pandemic bringing the median level of borrowing back to the 4 percent mark for the region as of 2023. This is about double the level of other regions developing regions.

Again, given the occasion, I want to say a word or two about the Rwandan experience. In recent years, the government has commendably eschewed central bank financing. This makes it one of the few countries in the region (other than those with well-developed capital markets like South Africa) that has been able to do so. This rigor is a non-trivial achievement. In the main, it has meant the recent surge in inflation has been predominantly due to exogenous food and fuel price shocks, rather than fiscal dominance.

Some Concluding Thoughts on The Challenges Going Forward

Overall, then my assessment is that central banks in the region have been instrumental in the progress countries have made over the years. All the more so given the hugely challenging circumstances that central banks operate in, weak policy transmission mechanism, the still shallow financial markets and underdeveloped regulatory frameworks.

Again, apologies for the rather broad sweep here. What makes our region so fascinating and working on issues affecting our countries so fascinating and demanding are the hours one could spend considering the difference in outcomes, say for inflation and growth, between and within countries with fixed and flexible exchange rate regimes. Take just countries in the eastern part of the Continent: was inflation higher in Ethiopia because of or despite the higher levels of growth observed over the years? How has Uganda been able to keep inflation consistently low? I could go on, but I will perhaps save these and other more nerdy questions for other fora, like the annual gathering of the Association of African Central Banks.

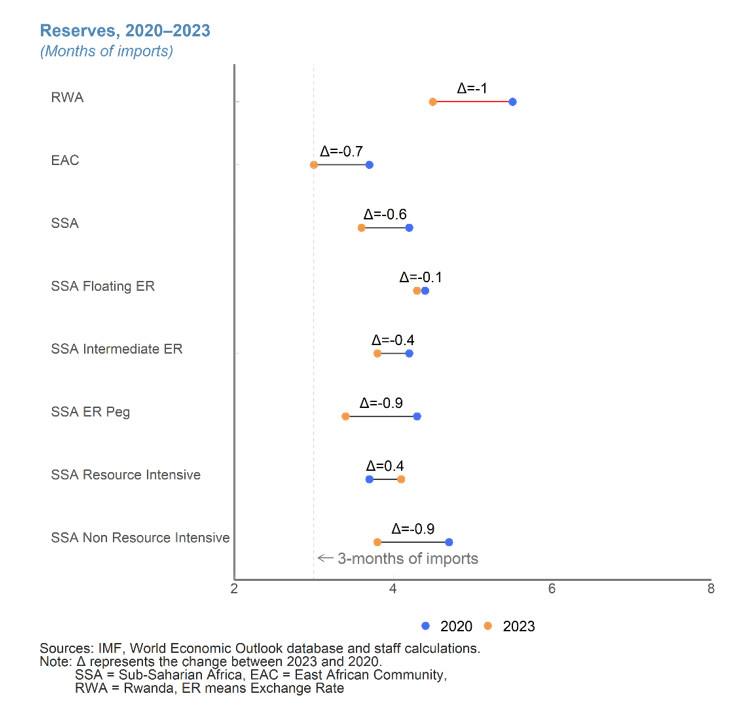

In a more forward-looking vein, I have to say the context for macroeconomic policy formulation is a hugely challenging one. The progress that has been made is now being severely tested. The region faces hurdles from a decidedly difficult external environment—something that could get more difficult still if ongoing geopolitical tensions continue to further disrupts trade and investment flows. More domestic policy challenges facing central bankers include the huge development financing needs countries continue to face, persistent current account deficits and exchange rate pressures. All there constrain the scope for monetary policy maneuver. Decreasing international reserve buffers have also heightened vulnerability to external shocks. In this difficult environment, safeguarding stability in order to foster the growth that countries need and the immiserating consequences of high inflation on the poor will be a challenging undertaking.

In this dynamic landscape, policymakers must adopt careful strategies, leveraging insights to calibrate monetary policy responses effectively, safeguarding against risks and nurturing resilience in the face of uncertainty. With this in mind, I would like to emphasize four key policy areas, which in my opinion have become increasingly important for central bankers today: exchange rate flexibility, contending with high public debt, financial sector risk management, and the growing importance of financial innovations.

Exchange rate flexibility

In Sub-Saharan Africa, the prevalence of fixed exchange rate regimes reflects a widespread "fear of floating," driven by concerns about exchange rate volatility's impact on inflation, balance sheets, and socio-political stability. This highlights the intricate balancing act policymakers face, especially amidst current global volatility. However, relying solely on fixed exchange rates limits policy flexibility and risks sudden adjustments, necessitating a more adaptable monetary strategy.

Globally, more central banks are turning to inflation targeting, prioritizing price stability while retaining the capacity to respond to economic shocks. Increasing monetary policy credibility is the antidote to the fear of floating. Monetary policy credibility, which takes time to acquire, is like a three-legged stool: saying clearly what you do, consistently doing what you say, and having the policy independency to do. Once policy credibility is achieved, the degree of exchange rate pass-through declines.

The importance of weighing these policy trade-offs emphasizes the need for a coherent macroeconomic approach, acknowledging the interplay between monetary, fiscal, and exchange rate policies. Policymakers must strike a balance between exchange rate stability, inflation control, and external competitiveness, while fostering sustainable growth. Through a holistic policy approach and enhancing policy coordination, SSA countries can better address the challenges of monetary policy in an uncertain and volatile global environment.

Contending with high public debt

Even when central banks stay clear of direct financing of the government, the pressure to ensure that there is adequate liquidity in the system and for the government’s borrowing costs to remain contained has been an age-old challenge in our countries and elsewhere. And in our region now with public debt levels quite elevated and domestic debt quite high, this challenge is set to be more acute still. Specifically, domestic debt now accounts for around half of public debt. The pressure for monetary policy to accommodate fiscal financing pressures has in the past been and going forward will be a clear threat to central bank’s ability to control inflation. The primary responsibility in dealing with this challenge of course remain firmly the responsibility of fiscal authorities.

Financial risk management

Prudent financial sector risk management is paramount, especially in countries where Pan-African banks play a pivotal role. The emergence of such banks has been a welcome feature of the economic landscape in recent years and will help foster economic integration, competition, and financial inclusion. But it comes with some risks that need to be managed carefully, notably weaker oversight from home country supervision or openings to exploit regulatory asymmetry. To tackle this, we must carefully manage rapid credit growth, uphold prudent underwriting standards, monitor concentrated exposures, utilize macroprudential tools effectively, bolster bank resolution frameworks, enhance regional supervisory coordination, and strengthen anti-money laundering/countering the financing of terrorism (AML/CFT) frameworks.

Financial innovations

With the proliferation of mobile money providers in Sub-Saharan Africa, central banks must upgrade their digital capabilities to ensure payments efficiency and manage risks, including those from crypto assets, cybersecurity, and illicit financial flows. By embracing digital innovations, central banks can foster financial inclusion and payment efficiency, by focusing, for example, on fast and cheaper payment systems. It is essential that they also understand the potential risks associated with new instruments like central bank digital currencies, such as the impact on bank intermediation, monetary policy transmission, currency substitution, capital flow management, cross-border transactions, legal and regulatory frameworks, and oversight capacity. Central banks with limited resources can take advantage of peer learning to boost capacity, particularly from those with more advanced digital payment systems, helping avoid the development of potentially incompatible cross-border technological solutions.

Central banks need to be on their toes and be ready to make bold moves in the coming years. It will be about being practical, accepting trade-offs, learning lessons from around the globe, and acting on them. Moreover, it will be crucial to keep central banks as free from political strings as possible.

With a blend of practical wisdom, an open mind for global insights, and unwavering independence, I have no doubt that central banks in Africa will overcome the challenges of the coming years.

Twishimiye Banki nkuru yu Rwanda! for its proud accomplishments over the last 60 years and wish it more success still in the years to come!

Thank you.