Building a strong, equitable economy

Transforming the US economy requires policymakers to recognize that markets

cannot perform the work of government.

The first step is to eradicate COVID-19. It has to be the first priority,

not only for public health but also for the US economy. Beyond that,

encouraging a strong and sustained recovery that delivers broadly shared

growth also requires the United States to address its long-term problems: a

costly health system that leaves millions with insufficient care, an

education system designed not to end inequality but to preserve it, lack of

basic economic stability for most families, and climate change.

Major public investments are required to deal with each issue. While it is

not necessary to worry now about paying for them, the nation should put in

place significant tax increases, primarily or entirely on the wealthy, to

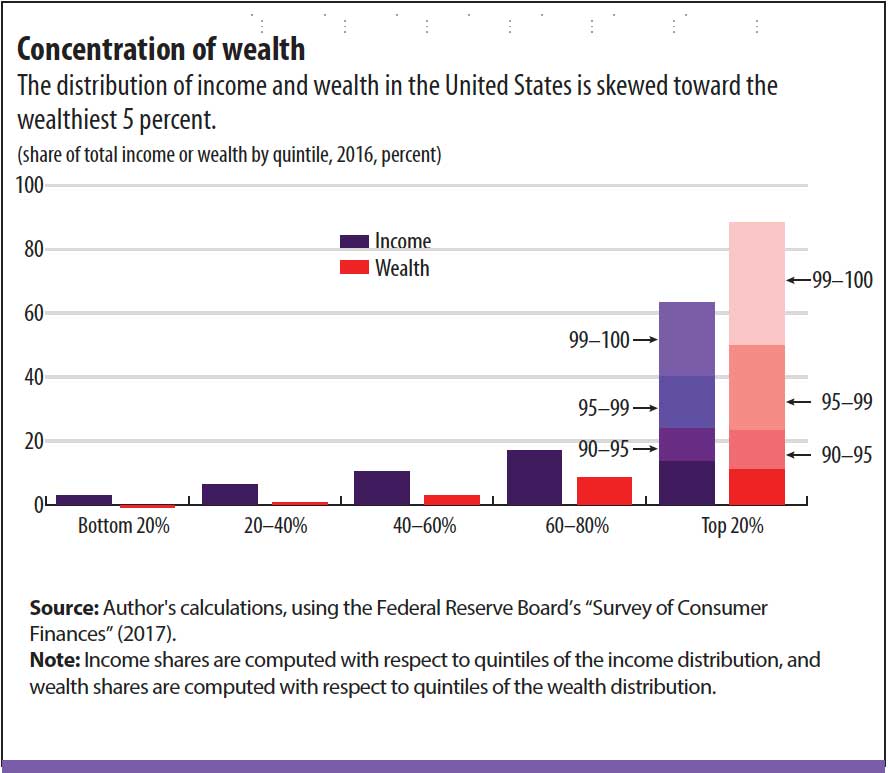

begin investing in these long-term solutions. The country should tax the

enormous wealth concentrated at the top that is being saved, or kept

overseas, and not being invested in the economy or in solving societal

problems (see chart).

Policymakers also must address the economic concentration that has created

monopsony power (a single or handful of buyers or employers) that keeps

wages down and threatens small businesses, which are the lifeblood of

innovation and economic dynamism. The first step is to ensure that the

recession and the programs designed to help businesses survive the crisis

don’t exacerbate this trend. Thus far, federal policies to address the

economic downturn have provided far greater aid to large businesses than to

small ones.

Policymakers also must ensure that federal government funds are directed to

productive uses that support workers and customers, and not to rewarding

wealthy shareholders. Corporations receiving aid should be barred from

issuing dividends and carrying out stock buybacks, and banks should be

required to suspend capital distributions during the crisis to support

lending to the real economy.

Even more fundamental to addressing excessive concentration is

strengthening US antitrust enforcement, which is weaker than it has been in

decades. The antitrust laws themselves also need to be bolstered,

particularly with respect to the rules governing mergers and exclusionary

conduct. Legislators should consider creating a digital regulatory

authority to enforce privacy laws and enhance competition in digital

markets.

The country also needs to better understand who benefits, or does not, from

recovery policies and what further actions are needed. Because overall GDP

is not up to that task, income must be disaggregated at all levels to

measure progress or lack thereof for all groups—which would enable the

United States to lay the groundwork for understanding what other actions

are needed to ensure more people benefit from the recovery.

US economic inequality is firmly tied to the issue of racial inequality.

The unmistakable message of the Black Lives Matter movement is that

Americans of color never have been able to trust government to act on their

behalf. Government must work to ensure that low-income Black, Latinx, and

Native American people can both develop and deploy their talents and skills

in the economy.

Taxing wealth, which is disproportionately owned by White Americans, is one

solution. But for that to address racial inequities adequately, the

proceeds of the wealth tax must benefit the majority of the nonwealthy. The

proceeds must be directed to the most urgently needed investments, such as

in COVID-19 testing and treatment in communities of color, in policies that

expressly and progressively support low-wage workers and care workers, and

in engagement with minority-owned small businesses. Otherwise, pervasive

inequities will be further entrenched.

A significant reason for the gender earnings gap is the lack of a national

paid family and medical leave policy and the absence of a national program

to ensure that families have access to quality, affordable

">

childcare and

prekindergarten education. Families with children that do not have access

to paid leave and childcare—or cannot afford them—have little choice but to

put careers on hold. This happens to women far more often than to men.

Legislation has been introduced in Congress to accomplish both of these

goals, and these measures should get serious consideration in the next

Congress.