Cryptocurrencies and DeFi aim to replicate money, payments, and a range of financial services. They build on permissionless distributed ledger technology such as blockchain. This technology allows for technical functions that can adapt to new demands as they arise, as well as for openness across borders. Yet crypto suffers from serious structural flaws that prevent it from serving as a sound basis for the monetary system.

First, crypto lacks a sound nominal anchor. The system relies on volatile cryptocurrencies and so-called stablecoins that seek such an anchor by maintaining a fixed value to a sovereign currency, such as the US dollar. But cryptocurrencies are not currencies, and stablecoins are not stable. This was underscored by the implosion of TerraUSD in May 2022 and persistent doubts about the actual assets that back the largest stablecoin, Tether. In other words, stablecoins seek to “borrow” credibility from real money issued by central banks. This shows that if central bank money did not exist, it would be necessary to invent it.

Second, crypto induces fragmentation. Money is a social convention, characterized by network effects—the more people use a given type of money, the more attractive it becomes to others. These network effects are anchored in a trusted institution—the central bank—that guarantees the stability of the currency as well as the safety and finality (settlement and irreversibility) of transactions.

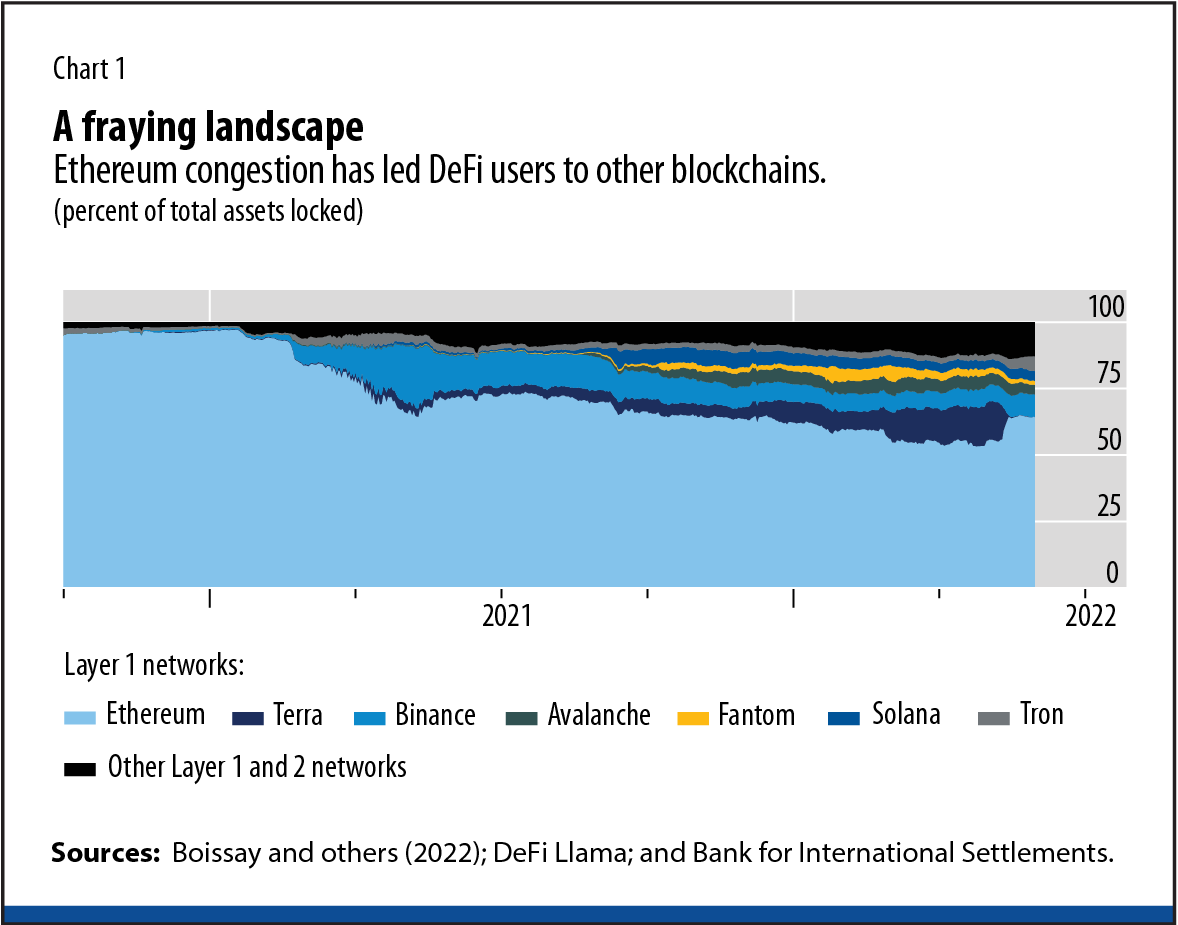

Crypto’s decentralized nature means that it relies on incentives to anonymous validators to confirm transactions, in the form of fees and rents. This causes congestion and prevents scalability. For example, when the Ethereum network (a blockchain widely used for DeFi applications) nears its transaction limit, fees rise exponentially. As a result, over the past two years, users have moved to other blockchains, resulting in growing fragmentation of the DeFi landscape (see Chart 1). This inherent feature prevents widespread use (Boissay and others 2022).

Because of these flaws, crypto is neither stable nor efficient. It is a largely unregulated sector, and its participants are not accountable to society. Frequent fraud, theft, and scams have raised serious concerns about market integrity.

Crypto has introduced us to the possibilities of innovation. Yet its most useful elements must be put on a sounder footing. By adopting new technical capabilities but building on a core of trust, central bank money can provide the foundation for a rich and diverse monetary ecosystem that is scalable and designed with the public interest in mind.

The trees and the forest

Central banks are uniquely placed to provide this core of trust, given the key roles they play in the monetary system. First is their role as the issuers of sovereign currency. Second is their duty to provide the means for the ultimate finality of payments. Central banks are also responsible for the smooth functioning of payment systems and for safeguarding their integrity through regulation and supervision of private services.

If the monetary system is a tree, the central bank is its solid trunk. The branches are banks and other private providers competing to offer services to households and businesses. Central bank public goods will support innovative services to back up the digital economy. The system is rooted in settlement on the central bank’s balance sheet.

Zooming out, we can see the global monetary system as a healthy forest (see Chart 2). In the trees’ canopies, the branches come together and allow economic integration across borders.

How can this vision be achieved? It will take new public infrastructure at the wholesale, retail, and cross-border levels.