Since the 1970s, emerging market and developing economies have aggressively tapped into global sovereign debt markets, seeking to jump-start growth or make up for transitory shortfalls in output and tax revenue. Has this borrowing had the intended effect? An analysis of the data suggests that sovereign borrowing may actually leave citizens worse off, increasing volatility and lowering investment.

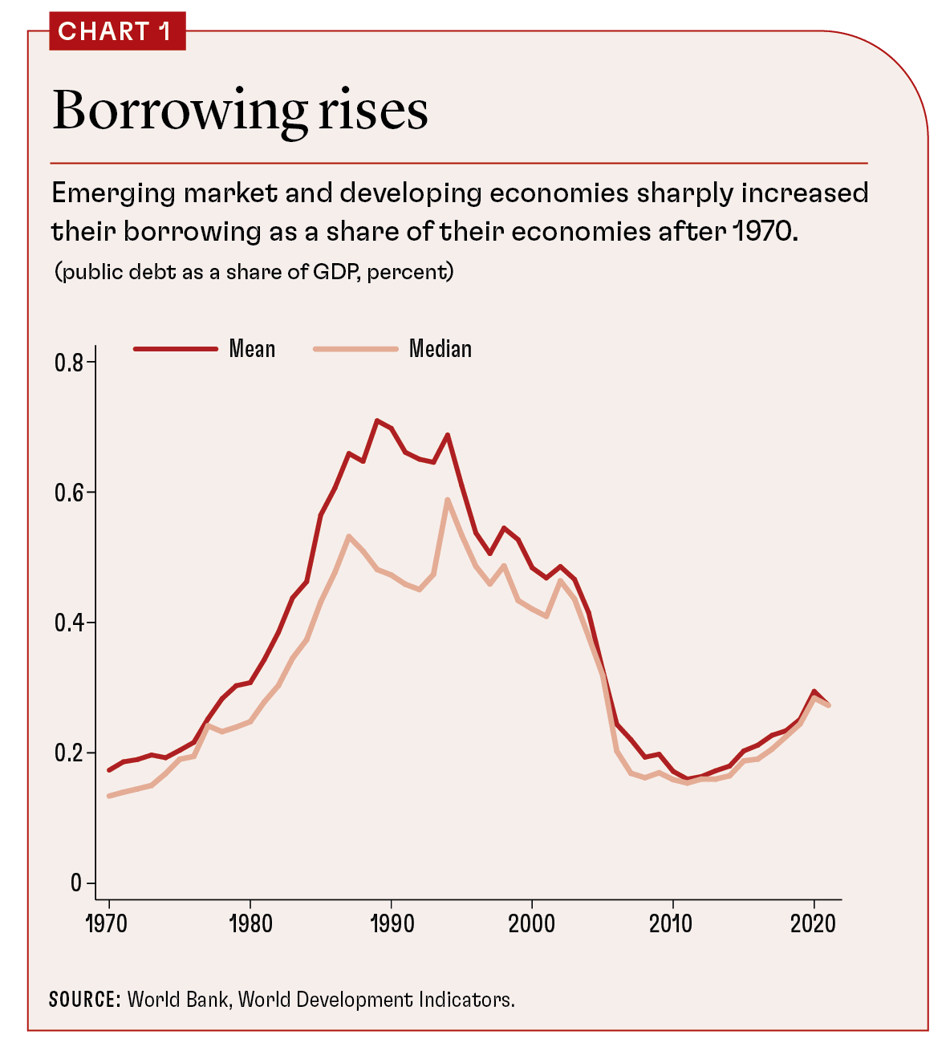

The ratio of external sovereign debt to GDP rose dramatically between 1970 and the mid-2000s, based on the average and median for a balanced sample of 52 developing and emerging market economies. Over the last 20 years of the sample, this trend has partially reversed, as shown in Chart 1.

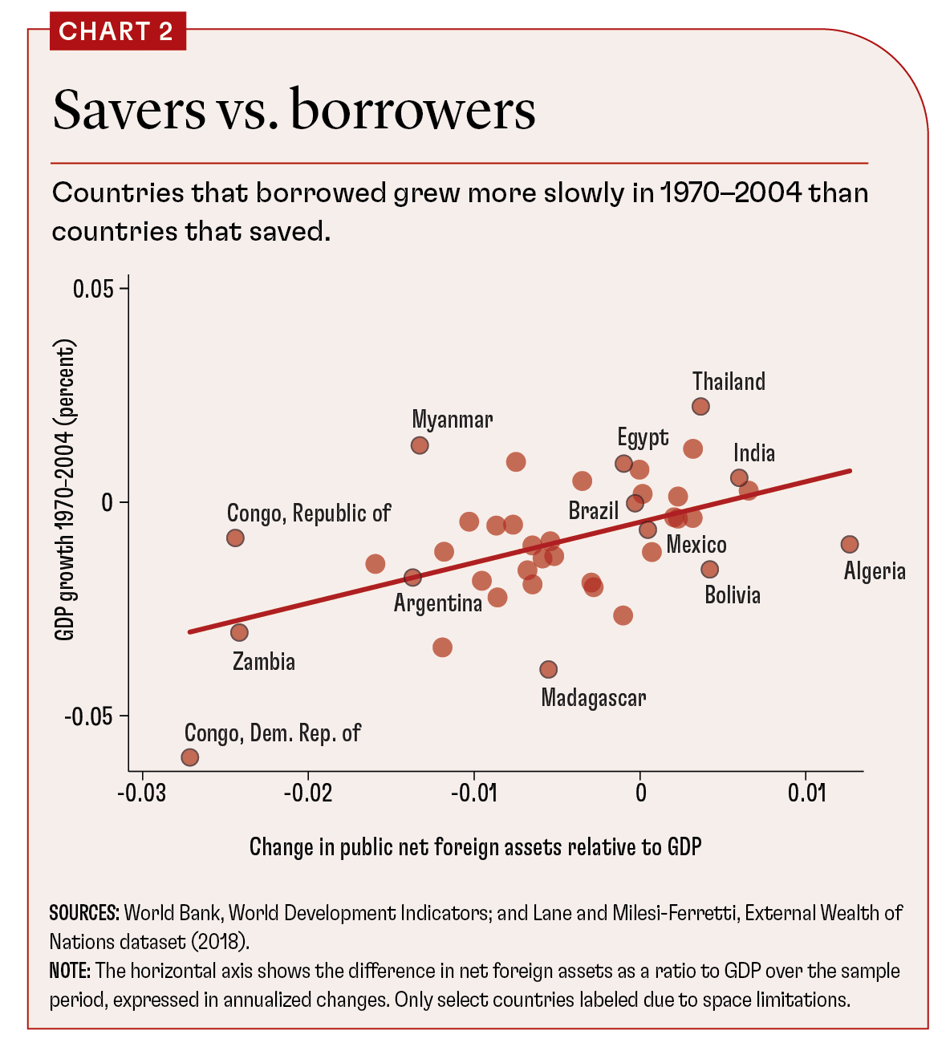

What are the costs and benefits of the surge in sovereign borrowing for the citizens of these economies? The promise, implicit or explicit, in standard economic models is that access to global capital markets facilitates investment and allows economies to insulate ("smooth") government spending from large fluctuations in output. That is, borrowing can fund large investment projects or cover temporary shortfalls in revenue, without drawing on domestic private savings. I refer to this as the "neoclassical paradigm." It predicts that countries that borrow (all else equal), should have faster growth and less volatile spending. However, this is exactly the opposite of what we see in the data. Chart 2 shows a scatter plot of the increase in government net foreign assets (foreign reserves minus external debt) on the horizontal axis and annualized per capita GDP growth relative to the United States on the vertical axis. The time period is 1970-2004, the period of the large increases in debt seen in Chart 1. The data show countries that had external public savings (foreign reserves exceeding external debt) experienced faster growth, while those that borrowed stagnated.

Impatient politicians

An alternative to the neoclassical paradigm holds that governments borrow due to present bias. That is, political incumbents prefer spending to occur while they are in office, which, without a sound set of political institutions, leads to excess borrowing. Given a large stock of debt, governments are tempted or forced to tax private activity, including private investment and capital income. This alternative perspective, developed in detail in my papers with Manuel Amador and Gita Gopinath, predicts that public borrowing crowds out private investment and retards growth. This is consistent with the scatter plot of Chart 2. It also makes a sharp distinction between public and private flows, a feature also consistent with the data. Chart 2 implies that over the long run, countries with low trend growth rates tended to borrow more.

The preceding focused on the period in which countries dramatically increased their debt. As noted, the latter half of the sample shows a decrease in debt to income, on average. The correlation depicted in Chart 2 does not hold for the later period. In fact, countries that decreased debt relatively more had slower growth in the period 2004-2022. One issue with the latter sample is that the reductions in debt sometimes resulted from debt forgiveness or default and restructuring. The data suggest that starting from low debt (as most countries did in 1970) is inherently different from low debt due to forgiveness or default. That is, the level of debt matters, but so does the history that led to that level of borrowing.

This suggests that countries that have large levels of debt differ along many dimensions besides debt. Indeed, countries differ in political institutions, which in turn induces differences in the level of debt. The ideal experiment would change the stock of debt without changes to other underlying fundamentals. In the absence of such an experiment, the best we can do is combine theory and data to distinguish cause and effect. Doing so makes a strong case that government debt crowds out investment and lowers growth. The neoclassical paradigm, in which debt and investment go hand in hand, faces a tougher challenge when confronted with the data.

Smoothing volatility

The neoclassical paradigm also holds that sovereign borrowing allows countries to smooth fluctuations in income. This is also counterfactual in the sense that over longer horizons, countries that borrow show more volatility in government expenditure and private consumption. In particular, there is a positive relationship between changes in debt and volatility of spending, indicating that more borrowing is associated with more volatile public spending. Again, this is contrary to the "smoothing" motive for borrowing predicted by the standard model.

One consideration is whether countries borrow due to large negative shocks, such as natural disasters or military conflict, generating a positive correlation due to luck rather than policy. Again, this is why it is important to have a long enough time series to smooth out the effects of temporary shocks. If a country frequently experiences large, negative shocks, they eventually come to be expected, and governments should respond by building up a buffer stock of reserves to be drawn on as necessary, rather than increasing debt levels. Clearly, this is not the case on average in the sample of countries depicted in the chart.

The data suggest that sovereign borrowing is associated with lower long-run growth and investment and greater volatility in spending. This runs counter to the neoclassical conventional wisdom but is consistent with a model of present bias due to political turnover combined with capital taxation. In short, sovereign borrowing generates volatility rather draws on it, and it is a drag on growth, rather than a means to tap into global savings to fund investment. We now turn to the question of whether the citizens of emerging market and developing economies would be better off if their governments had zero access to sovereign debt markets.