Transcript of the Food and Fuel Price Crisis: Seminar on Recent Developments, MacroeconomicImpact, and Policy Responses

October 3, 2008

Wednesday, September 24, 2008

Opening Remarks:

Dominique Strauss-Kahn, IMF Managing Director

Moderator:

Hugh Bredenkamp, Deputy Director, Strategy, Policy and Review Department

Panelists:

Patricia Alonso-Gamo, Assistant Director, Strategy, Policy and Review Department

Benedicte Christensen, Deputy Director, African Department

Sanjeev Gupta, Senior Advisor, Fiscal Affairs Department

Thomas Helbling, Advisor, Research Department

| Download the presentation (1.31 mb PDF) |

MR. STRAUSS-KAHN: Thank you for coming.

Our message today is very simple: the world must not forget the food and fuel crisis, and because we are now all focused on the financial crisis, for good reasons, the problems cased by the surge in food and fuel prices are not making headlines anymore. So, the very message is that we cannot lose sight of the other crisis, which takes place all over the world but has more consequences in poor countries.

Last June, as you know, the IMF issued its assessment on food and fuel prices, and today we want to update what has been said three months ago. Having in mind that the crisis has such a severe impact on the poor that we cannot just say okay—as I will comment a little more later—prices are probably going to stabilize or to decrease, and so it's behind us. It's true that prices have eased during the recent months, but they're still above the level where they were at the onset of the recent surge. So, the situation is probably better than it was a few months ago but it's still very, very difficult. Additional aid, which was promised—I won't say as always, but unfortunately as often—failed, at least in large part, to materialize, which means that most of those countries were awaiting aid and a large part of this aid is yet not available.

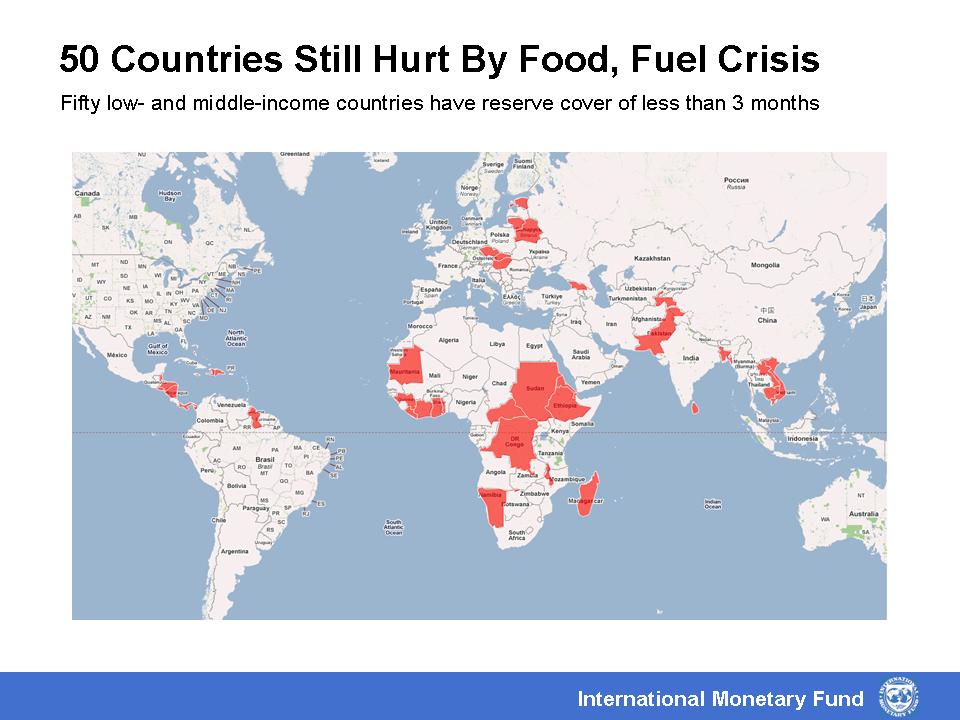

Let me just try to highlight some facts. Of course many, probably all, countries around the world have suffered from the increase in prices, but 50 of them are really hurt (Slide 2: "50 Countries Still Hurt by Food and Fuel Crisis"), and the impact, far from being decreasing, has continued to mount, so 50 countries among the low- and middle-income countries remain at risk in 2008 and 2009. These countries-some very big, some very small-are shown on this first slide. If you look at net fuel-importing low-income countries, the increase in the fuel bill between 2007 and 2008 is around 3.2 percent of GDP, which is an amount close to $60 billion.

{kind=link}

And now if you look at food prices, and at 43 net food importers, the impact is 0.8 percent of GDP, which is a little above $7 billion. So what has happened in no way can be considered something which is not significant. It's a very significant shock, with the oil pressure having more influence on balance of payments problem and food prices having more influence on inflation and the purchasing power of the people in these countries.

Having said that, what is the macroeconomic impact? There are several concerns: the weakening of balance of payments for some countries; the problem of imbalances in domestic budgets for other countries. Probably the inflation question is the one I would like to underline.

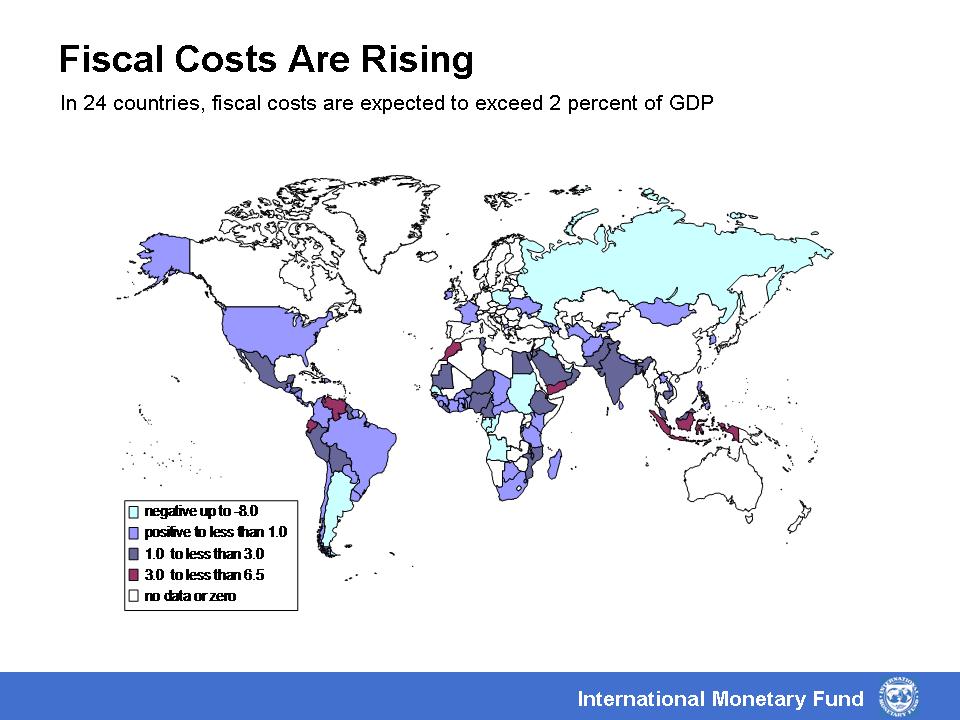

To fight inflation, many countries have accepted fiscal costs, and those fiscal costs are obviously increasing (Slide 3: "Fiscal Costs are Rising"). What did they do? They tried to reduce taxes or tariffs on food, to have a decrease in prices, or a reduced increase in prices. They tried to organize some subsidies. They also sometimes accept a rise in public wages. All this, of course, has a lot of influence on the fiscal sustainability of the country.

{kind=link}

Again, the slide shows 24 countries where the influence is over 2 percent of GDP. The concern is not only the overall cost but also the fact that in our view very often—not always but very often—the subsidies are not targeted enough. They should be targeted to the poor, to the ones who need them more. But often you have general subsidies. For instance, subsidies on energy—gasoline for instance—affect only the upper part of society using this kind of product and probably could be avoided. So we try to convince countries to have more targeted subsidies.

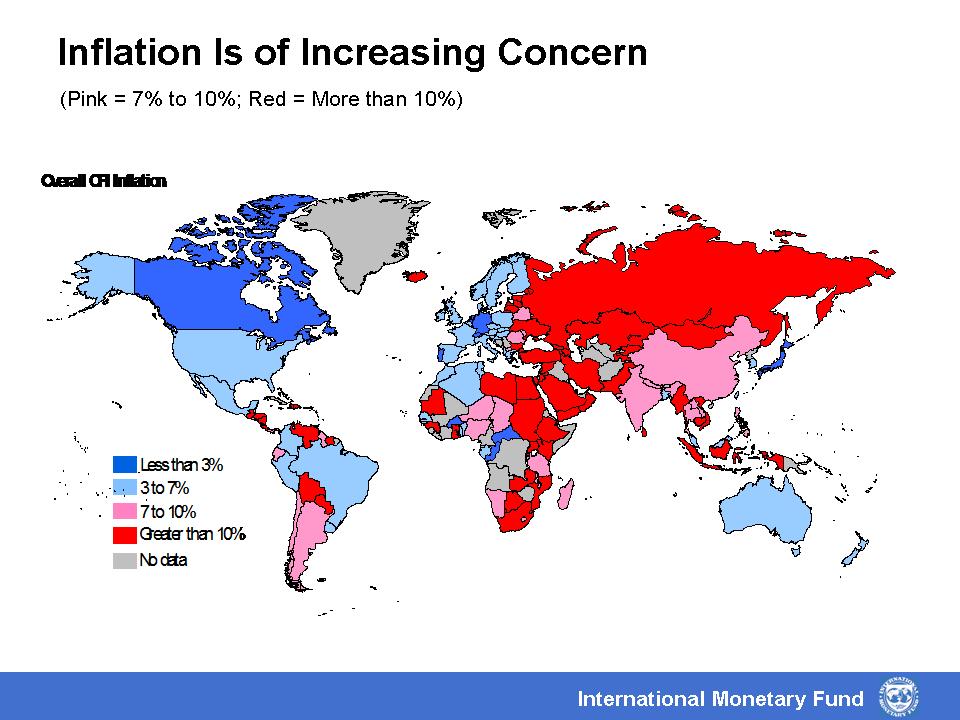

Now, if we look at inflation (Slide 4: "Inflation is of Increasing Concern"), which is, as I said, a question of increasing concern, we see that in the second quarter of 2008 the increase was around 3 percent. We expect at the end of 2008 that the average inflation will be around 13 percent, which is a rather great impact, and you see in this slide all the countries where we expect inflation to be over 10 percent.

{kind=link}

Now, we all know that inflation has a greater impact on the poor—it hurts particularly the poor—and that the one group that is least protected against inflation is the group having the lowest income. So, again, the question of fighting inflation is not only a kind of IMF mantra that inflation is bad and you should fight against inflation for macroeconomic reasons. Of course it does exist, but also that consequences of inflation are poorly distributed and that the poor are the ones who are the most hurt.

My last remark is about what we can do. What can the international community do? What can the Fund do?

Obviously, the world has to do more—helping the country fighting inflation; helping the poor; helping the country to have a sustainable growth path to get through this period. I would like to stress two priorities. The first one is helping countries bring inflation under control, which is certainly the most difficult thing for these countries but also one of the most important things, not only as I just said before for the future and sustainability of the economic program, but also for inequality and poverty in the countries themselves. The second priority is to try to convince governments to target the different kind of safety net they're likely to put in place—which is not easy because it's much more sophisticated. For any minister it is much easier to announce a general measure which is understandable by everybody, that can be implemented very rapidly—even if they know that it will be less effective than a measure which will take more time to be implemented, that will look stronger from a particular point of view but will be more targeted to the poor. So, the natural trend is to go to what is simple. And I can understand that this was the first reaction to the crisis months ago. But now that we see that the problem is not behind us, it's certainly time to retarget those subsidies and tariffs, to create safety nets really dedicated to those who need them.

On the other hand, the donors also have to do their part. As you know, an important meeting at the UN level is taking place this week, but I must say that so far the international community's response has been disappointing. It is not only a question of money, it is not only a question of donors—as I said before, it's also a question of implementing the right policies. Nevertheless it's also a question of money and donors. And we cannot be in a situation where you have a big international conference and a lot of pledges appear, a lot of institutions or countries are proposing to put money in different kind of funds, and at the end of the day the money is not totally available. I really want to stress this. It's an appeal for donors to do what they say they will do.

But it's not only a question of donors. I want to say a few words on what the Fund is doing. We're working on the three legs we traditionally use. The first one is policy advice, and we try in most of those countries to give the good advice. One of the examples I just gave was about the structure of the safety net. Another can be on the way to manage monetary policy, to avoid an increase in inflation without destroying the possibility of growth.

The second leg is technical assistance, and we have a lot of teams in the field providing technical assistance.

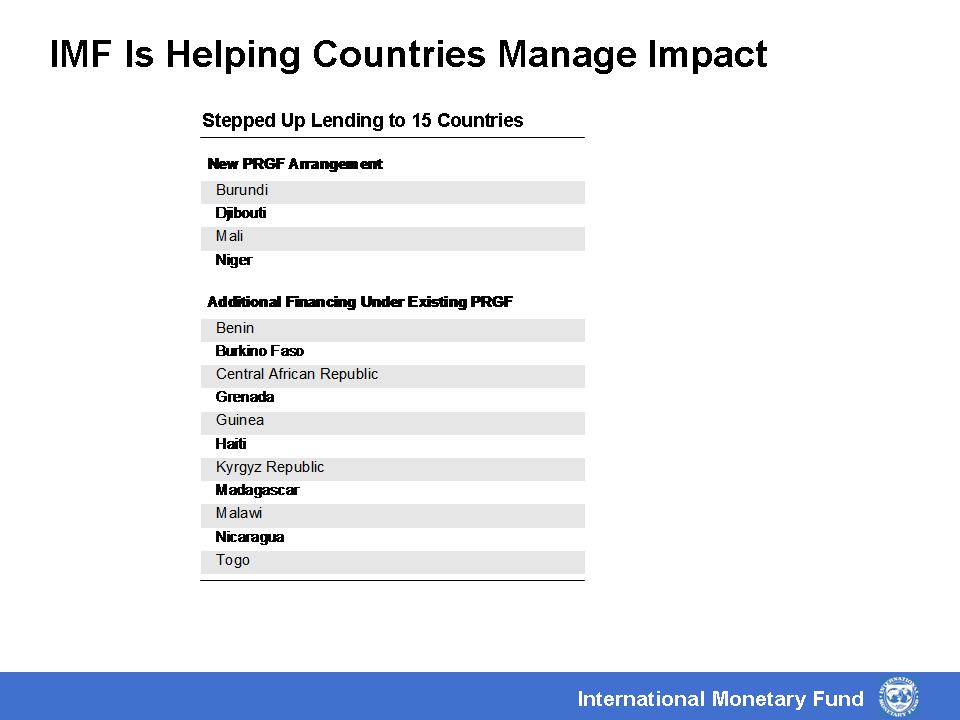

And the third leg is lending. As far as lending is concerned, two points. The first one is we already increased our loans to 15 countries with new or existing PRGF arrangements (Slide 5: "IMF is Helping Countries Manage Impact"). Maybe some other countries are in the pipeline - when they have problem concerning their balance of payments directly linked to increases in prices, we're ready to help them.

{kind=link}

Last Friday the Board of the IMF reformed significantly the Exogenous Shocks Facility (ESF) which has existed for quite a while but was a bit difficult to use by the countries because of the conditions and the way it was organized. So we streamlined, simplified, and opened this ESF. I don't know if I should say that hopefully it will be used by a country, because it means that country will have a problem. But at least if a country has a problem hopefully now the instrument will likely be useful. I know that we already are in contact with some countries that are interested in this new version of the ESF, and probably in the coming weeks we will see a couple of them using this new facility to try to solve their problems.

A word to conclude. Everybody understands, and especially in this institution, that a large part of our time and our work is devoted to the financial crisis even if this crisis is not directly an IMF crisis, meaning by that that the IMF is mostly concerned by crises having balance of payments consequences. the current financial crisis hasn't yet had those kinds of balance of payments consequences. Nevertheless the Fund is doing its part, sometimes behind the scene. At the 2008 Spring Meetings we estimated that the full cost of the total losses in the U.S. financial sector would be $1.1 trillion. At that time some said that was too much. Now we just adjusted this estimate to $1.3 trillion. Now the 1.3 trillion is to compare to 700 billion already written down. So it means that there's more to come. And in this respect I think the Fund is playing its role of alerting the international financial community to the risk we are facing and, as I told you, providing some advice—because we have here a lot of experience about what has happened in other countries. But even as we work on the financial crisis, we should not forget what I called at the beginning the other crisis. And the other crisis for a large part of the world is the most important one, because the financial crisis has of course a lot of consequences in the U.S. and in Europe, but less in Asia, South America and Africa through the general slowdown in economic output. On the contrary, the other crisis, the crisis on prices, fuel and food, has direct consequences on everybody, but mostly on the emerging market countries and the low-income countries. I think it's our role to signal that. Thank you very much for coming and for sharing our concerns about this problem. I'm going now to let you work after my introduction. Thank you again for being here.

MR. BREDENKAMP: Good morning. let me again welcome you to this briefing. My name is Hugh Bredenkamp, I'm a Deputy Director in the Funds Strategy Policy and Review Department and head of the IMF's New Low Income Country Strategy Unit.

I have with me four colleagues at the table who will be familiar to any of you who attended the briefing three months ago. Benedicte Christensen is Deputy Director of the African Department, Sanjeev Gupta is the Senior Advisor in the Fiscal Affairs Department, Patricia Alonso-Gamo is Assistant Director in the Strategy Policy and Review Department and head of the PRGF Operations Division, and Thomas Helbling is an Advisor in the Research Department.

The Managing Director has set the scene for us. His key message was that the shock from higher world food and fuel prices is still very much with us, and, indeed, is continuing to do significant damage to the economic prospects and to the prospects for stability and poverty reduction in many developing countries around the world. I will talk for a few minutes now about some of the more detailed analysis behind our updated assessment. We will then open to the floor for questions and comments and I'll turn to my colleagues for help in responding to those.

Let's first take another look at how the key energy and food prices have evolved since the report that we issued last June. You can see in this slide that the solid red line is the latest projection for energy prices that will be in the September World Economic Outlook (WEO). And the comparable data and forecast for food prices is the solid black line at the bottom. The dotted lines show where we expected energy and food prices to go at the time of the Spring WEO which was underlying our assessment of the food and fuel shock that we presented last June.

As you can see since the last assessment, prices have actually been generally above what we had anticipated. And this is somewhat contrary to popular perception at the moment; people are focused on the fact that energy and many other commodity prices have been easing in recent weeks. But the reality is that for most of the last three months, they've been higher than certainly we had been assuming, and that is one reason why the shock is still very much with us and significant. Looking ahead from the recent developments also, some of the fundamental factors that we argued last time would keep prices high over the median term are still very much with us. We still see the prospect of continuing strong demand for commodities, especially in the big emerging market economies.

We also see limited scope for positive supply responses, both in energy and in food in the median term. And for these reasons, we see the likelihood that these prices will remain at elevated levels.

Even though the prices have come off from some of the peaks, especially for fuel, fuel prices are still around double where they were before the shock started in the beginning of 2007, and food prices are around 40 percent above where they were pre-shock.

What does this mean for countries' balance of payments positions? This chart shows the cumulative hit taken by low income countries since the beginning of 2007. These figures are in percent of GDP, so these are significant amounts.

The recent estimates have risen for two years; one reason is that, of course, as time passes, since this is measuring cumulative impact, we've got three months more of negative shock that we're adding to the total; and secondly, because as I just showed in the previous chart, for most of this period, prices have been above where we had expected them to be last June.

Now, as the Managing Director emphasized, while the costs have continued to mount, additional donor support has really not been forthcoming, at least not in anything like the amounts that were promised or envisaged, and so the result has been that countries have had to continue drawing down their own foreign exchange reserves to manage the balance of payments losses that they're facing. And what this table shows is how that translates into numbers of vulnerable countries, which we have defined here as countries having reserve positions that cover less than three months of their imports. And so you can see that, whereas in the spring we were expecting 47 countries to be in that vulnerable reserve situation by the end of 2008, we now expect 50 countries to be in that position, so it has actually increased slightly, again, consistent with the notion that the shock, far from having diminished, is actually still accumulating. As you can see here, two-thirds of those 50 countries are low income countries.

We also looked out to 2009 to see how things might evolve in the coming year. For 2009, we see, even in the baseline, no improvement in at least this indicator, looking at the number of vulnerable countries; in fact, the number edges up slightly further from 50 to 51 countries.

It is, of course, true that the commodity prices at the moment are particularly volatile, especially oil prices. Oil price jumped $25 on one day earlier this week. With particular uncertainties surrounding the oil price, we looked at a couple of alternative scenarios for our 2009 projection, one in which oil prices stay low, by which we mean hovering at round $104. Even under that assumption, the number of vulnerable countries doesn't go down by very much, it drops from 51 to 47 at the end of 2009.

If, by contrast, oil prices were to go back up to the peak that they reached earlier this year, then the number of vulnerable countries would increase, obviously, to about 58 countries.

The other main macroeconomic indicator that we emphasized in the last briefing was inflation. This is the other main aspect where countries feel the impact of the food and fuel price shock most directly.

At the briefing we gave last time, our expectation was that inflation would peak sometime in 2008 and fall back by the end of the year to a level slightly below where they were at end 2007. As you can see our current projections, that is no longer our expectation, unfortunately. We see inflation continuing to rise, especially in low income countries, where it spikes up quite significantly by end 2008. The reasons for this are partly that the past through - from world prices to domestic prices—has been a more protracted process then we had expected or hoped, partly because of policy decisions that have been made at the country level, and partly because monetary policies in particular have not been tightened in the way that we had assumed and have been advising to resist the inflation pressures.

As I said, this is a particular problem in low income countries, and this is a major concern for us. The more that secondary inflation effects (the generalized effect that you get on inflation indirectly on the rest of the consumption basket) becomes entrenched, the more difficult and the more costly it's going to be for countries to get inflation back down to comfortable levels again.

And as the MD emphasized, a sustained rise in inflation, aside from being damaging to growth prospects, would also be directly harmful to the poor, who are at least able to protect themselves.

The third dimension to this is the fiscal effect. And here we're looking at the fallout effects on government budgets, where we also have a number of concerns. In general, the fiscal costs of the shocks are continuing to rise, up from about .6 to .7 percent of GDP on average now. Most of the costs are accounted for by fuel subsidies, around two-thirds of the increase in fiscal costs since 2006. And the use of subsidies and tax cuts of various kinds that governments are using to try and soften the impact, especially of oil prices, but also, to some extent, of food, is spreading.

The number of countries that are using these instruments is increasing. Total cost of food and fuel subsidies now is expected to exceed two percent in as many as 24 countries, two percent of GDP, which is a very significant amount for the budgets that these countries have.

And as the MD stressed, part of the problem here is that social safety net measures, while understandably are broad-based initially, remain poorly targeted, and our efforts to help countries put in place more cost effective measures that are directed at the most needy will have to continue to push on this problem. We're also, incidentally, seeing some evidence now, which is also a concern, of countries conceding higher public sector pay rises, in part as a response to the food and fuel price shocks, and this is a particular concern because public sector pay often is a leading indicator and even a causal factor in more broader wage developments. And the more that wages try to keep up with the price shocks, the more risk there is of generalized secondary inflation problems which countries will have to then try to squeeze out.

Finally, just to reiterate what the managing director said with regard to IMF financial support for low income countries affected by the food and fuel price shock, here again is the table of 15 countries.

Just to make it clear what we mean here, these are four new PRGF arrangements, where additional funding was built into the new arrangements explicitly to reflect the costs of the food and fuel shock on these countries.

For the other 11, these are countries that already had PRGF arrangements in place and where we proposed and succeeded in getting increases in the amounts of money available to these countries under the PRGF arrangements. So let me leave it there, that hopefully gives a bit more detail and a bit more background to the assessment. We can open up to questions and answers. Thanks.

MR. Bakvis: Peter Bakvis with the International Trade Union Confederation. About two-thirds of our 168 million members are in developing or transition countries. I have three short questions. One is on the impact that the financial crisis might have on further price fluctuations, specifically of food. We've seen in the past week that oil prices are going wild, and some people attributed that to people fleeing equity or even the U.S. dollar, and placing into oil futures.

And I was looking this morning at the commodity market, something called rough rice, I'm not sure what really that is, but I notice it's gone up ten percent in the past week, and I'm wondering if one can foresee more of that in the months and weeks to come.

Two brief observations and questions on some of your policy recommendations. Now, I know that the IMF encourages further targeting of assistance programs, and that poses two kinds of difficulties. Generally, I know you're in favor, for example, of cash transfers rather than general food subsidies, which, in theory, is fine, but generally the poorer the country is, the less it is able to administer cash transfers or any kind of targeting program, and potentially millions could fall through the cracks, whereas with the general subsidy, it's not targeted, some people who maybe don't need it benefit, but at least everybody does have access to some, you know, cheaper food stuff.

And the other question is where you set the target level. Is it on the extreme poor, is it slightly above? How do you address those particular concerns?

And my third question is about the comments that were made about avoiding unsustainable wage increases that could set off an inflationary spiral. How does the IMF define that? You know, many low income workers are both private sector, by the way, and public sector. In some countries the government decrees private sector wages, as well, sets minimum wages at least, attempting to maintain their buying power. Now, are you implying that low income people should accept the decline in buying power, and if so, by how much? Thank you.

MS. SCOTT: Heather Scott with Market News International. Two things. You mentioned the monetary policy responses have not been what you expected or have been advising; can you give some insight as to why that's the case? Is it lack of autonomous central banks or political issues with raising interest rates, or what do you see is the problem there?

And also, the report notes that countries have been resistant to using flexible exchange rate regimes to absorb the shocks of inflation. How concerned are you about that, and also, again, can you explain why they have been so resistant to that change, and if that is a widespread problem across many of these countries?

MR. HELBLING: In terms of the commodity market implications what we have seen in recent days with extreme volatile prices, there are two layers of influences. One key layer is linkages between the global financial crisis and global economic prospects. Global growth is a key determinant of commodity prices, it affects demand, and clearly, firms, producers, everybody has been reassessing their views of global economic prospects. How the financial crisis will play out is still uncertain, so that part is of extreme volatility.

The second layer is much more short term, is to invest repositioning after the financial crisis. Some of the investment banks offer commodity financial product. Some of these products have counterparty risks to the extent that these are products issued over the counter, in over the counter markets. With what happened to Lehman Brothers, people reassess counterparty risks in some of these products. So there was quite a substantial investment to repositioning, so that was the other layer. That layer I would expect to fade in the coming days and weeks, and we're going back to the fundamentals, and ultimately the question is, how the financial crisis will play out, how it will be resolved, and what is the real economy impact, and there are still many questions out there.

MR. BREDENKAMP: On the questions that were raised about targeting social safety net measures, and the extent to which they can reach the needy, maybe, Sanjeev, you could say a few words, and then Benedicte could maybe add something from the perspective of African economies.

MR. GUPTA: Let me start by noting at the outset that we do recognize that targeting poses difficulties in a number of countries, in part because these countries don't have adequate social policy instruments to use, and they don't have the capacity to target benefits. This has meant that these countries can't use mechanisms such as targeted cash transfers. Nevertheless, there are many things which the government can do, and have done, and I can give you some examples. One could consider raising prices of goods consumed primarily by the poor, more gradually, and these could be goods such as basic cereals or kerosene. That's a consideration that governments can take into account.

They could also finance some spending programs from the savings that result from subsidy reform, from targeting, that is, on programs that benefit largely the poor, and this was done in Ghana more recently. And, of course, one could consider using in depth means of targeting, which are, you know, geographical or categorical targeting mechanisms that is looking at the characteristics of the poor, and then using those as a means to transfer benefits to them.

And, of course, many countries, from India to Bangladesh, have relied on public works programs, which are mechanisms to transfer income. These are self-targeting programs. And in Latin America and other places, the school lunch programs, which are another way of transferring income to the poor households, has been used quite effectively. Now, these are imperfect but they are more cost effective than universal subsidies in protecting poor households. I think that's the basic message that one has to keep in mind, that one can't just continue to rely on universal subsidies, especially, as the MD noted, now that some of the initial price increases are behind us, now one should be thinking of looking at which are less expensive so as to reduce the fiscal costs, because if the fiscal costs continue to rise, we will probably have an impact on other kinds of high priority spending which the governments will not be able to finance, and which can have implications for the MDGs and long term growth prospects of the country. Thank you.

MS. ALONSO-GAMO: I can just add just a couple of examples of what has been done in some of the African countries. The first reaction of most governments was to reduce taxes in some cases. Also, there were some price freezes, and that was understandable because there were risks of social unrest, but we now see a couple of countries that are starting to reverse these more general measures, because they prove very expensive on the fiscal side. Senegal in mid September announced they're removing the price controls and also some of the subsidies they had on some of the food and energy products, and how did that happen? It happened through an analysis of who benefited from these subsidies and price controls. And we, in part, helped also the government analyze this. We sent a group of experts on poverty and social impact to analyze who benefited from these measures, and it turned out that it was well-to-dos that tended to benefit.

Now, what is the government doing instead? Well, it is increasing, for instance, feeding programs of school children, trying to hit at where maybe the poor would benefit more.

Similarly, in the case of Togo, the government did not introduce these various subsidy programs in part because it really didn't have the budgetary space to do so, but instead, there was a problem with civil servants, who hadn't been paid for some time. The government instead repaid what they owed the civil servants in wages, because, as you know, the urban part of the population cannot benefit from substance farming, and therefore, they are mostly at risk, sort of hit immediately by rising food prices. In addition, they helped also the agricultural sector by giving targeted subsidies for fertilizer and for seeds. And again, these are just examples of how it was done in practice.

MR. BREDENKAMP: On the question about wage increases and what would you find as excessive. In general, it's an unfortunate fact of life that when a country gets hit by a terms of trade shock, that is when the price of major goods that it imports rises relative to the goods that it produces and exports, the real incomes in that country have to go down, there is no way around that, and the only question is how the real income loss is distributed across the population.

One impact is that typically real wages have to be lower than they otherwise would be. Now, that doesn't mean, by any means, that we would advocate wage freezes, that wage earners should not still be compensated for inflation, or that wages should not continue to rise to the extent that there is productivity growth going on in the economy, but the extent to which this effect on real wages has to be allowed to happen will vary significantly from country to country, depending on the extent to which the net importer or net exporter of the goods that are suffering the price shock. One can't give a generalized answer about what the implications would be, but one can make estimates country by country, looking at the circumstances, and that's what we would try to help policy-makers do case by case. I don't know if you want to add anything to that, Patricia.

MS. ALONSO-GAMO: I think that what Hugh has said nails it. When we're looking at inflation, policy-makers have to look at what is core inflation and what is the inflation that is caused by the food and fuel prices. What you would want is for wage increases to reflect what are increases in core inflation. But if you have an adverse shock, you know, everybody is poorer by that amount and no one should be compensated by the additional food and fuel shock, because then you're just feeding inflation. There's no real wealth behind these increase. That takes me to what is the monetary policy response, and as I said, the intent of the policy-makers is to differentiate between core inflation and the food and fuel inflation, and try to prevent for the first round impact of the food and fuel, let the prices move for that, but then to try and prevent the increase from getting settled or entrenched to the core inflation and then just leading to an inflationary spiral.

We don't have a unique response of what the monetary policy response should be, first because there are different types of countries theater facing different problems, and the panel showed it very clear. You have the advanced economies where, in fact, the issue is being complicated by the financial crisis, because the monetary policy response has to be looking both at the impact of the food and fuel, but also there are the issues of financial markets and liquidity, which is muddying the response. Then you have the emerging markets, which in many cases have moved to an inflation targeting regime, and there they have an issue of credibility, because you have countries where they have suddenly a very wide difference between what core inflation and headline inflation, and they have to persuade people in the market that they are committed to maintaining their core inflation target, and at the same time, headline inflation is much, much higher. So how do they maintain this credibility over the long term? And then you have low-income countries which have been the most affected, because food is a higher share of the basket for them, and in many cases have fewer mechanisms, and that may explain why a lot of countries have stuck to the exchange rate angle, because they either have exchange rate regimes or they use that as their anchor.

MR. BREDENKAMP: Do you want to say something else, Patricia, on this question of why countries have been resistant to allowing the exchange rates to take part of the adjustment?

MS. ALONSO-GAMO: We are not saying what countries should or shouldn't do. I think that the circumstances differ. What we have noticed is that, first, we have a large number of countries that have been effected at - exchange rate regime, so in those cases, they don't have an exchange mechanism. But then we have a large number of countries that have been effected which do have a floating exchange rate, and what we've seen is that they have been reluctant to let the exchange rate depreciate, especially the ones that have been adversely effected. Now, that may be because we have the trade-off between adjusting to the shock, and at the same time if the exchange rate depreciates, you have further inflation, so they have a difficult dilemma there.

There is no unique answer, it depends on the country's circumstances and what the policy should be. What's clear is that if you have mounting fiscal costs, and the exchange rate is not moving, and if you're losing reserves, at some point something has to give, and what is the best policy combination for each country? One has to look at it on a country by country basis. One important message from our study is that the circumstances differ very widely. You have food exporters that are fuel importers. You have all kinds of combinations. In fact, countries are net gainers, but still they have fiscal problems, and they have issues of passing on the fuel and food price increases to the population. I mean you have big exporters that are gaining on the balance of payments, but still face the same distributional problems. You have issues of distribution between the rural and the urban population. So each country policy response really has to be looked at individually.

I just want to add a couple of comments on why countries have not tightened monetary policy sufficiently and why they have maybe been behind the curb. I think it has also been difficult for policy-makers to implement policies following these shocks. It's not just a matter of that they knew they should do something differently. We have had very close policy dialogue with all the countries, because most of the African countries have a program with the IMF. We have also discussed with countries how they shouldn't overreact, they shouldn't step so hard on the brakes that really the real economy is adversely affected because of the shocks.

But when it comes to the practice, how do you go about it, how do you set monetary targets and interest rates from the central bank? It is more difficult, also because the transmission mechanism, the way monetary policy impacts the real economy in these countries, it's not always well known. We observe afterwards the effect that there actually has been increasing inflationary pressures. We also observe that interest rates of central banks have not increased as much as they probably should. But it's not all this easy when policy-makers are in the moment to actually react correctly. We are debating these issues with the countries, and many of them are very sensitive to having inflation rising too much because of the impact on the poor.

MR. BREDENKAMP: Okay. We're running a little over, but since we started later, I think we can continue for a few more minutes and take some more questions if anybody has additional issues.

MR. BARKLEY: Tom Barkley from Dow Jones. I was just wondering if you could address the whole idea of decoupling, and I'm wondering whether you expect emerging countries to be less resilient than they have been to the overall slow down in the global economy, and what that means for their inflation outlook?

MR. BREDENKAMP: Why don't we just take that one and see how it goes?

MS. CHRISTENSEN: Just in terms of the impact, at least on Africa, if we were to look at the global slow down, and also the financial turmoil, I think it's probably less the direct impact from the financial slowdown on Africa. But what will have an impact is the impact on commodity prices. If the financial slowdown leads to decreasing demand in the global economy, and it effects commodity prices also of the exporting countries, that will certainly have an impact. If you look at the trend growth in Africa compared to the rest of the world, you see that the trend can vary. Africa has picked up and actually has started to grow stronger than certainly some other regions of the world, but if you look at the difference from this trend, how it fluctuates, you actually will see that it follows very closely also the global economic situation. So certainly a continent like Africa is not immune, and it will be affected one way or the other by the transmission mechanism. The way this impact will happen varies.

MR. BREDENKAMP: I would add that there can be, of course, real spill-over effects, and also financial ones. Whereas some emerging markets come under strain from the financial spill-over effects of the global financial crisis, although we haven't seen any of these countries tipping into crisis themselves yet, fortunately. There are low income countries, of course, that have started to engage with international capital markets. Some of them are beginning to rely on private capital to fund some of the investment budgets in particular, and some of these countries may start to run into difficulties in rolling over those kinds of debts or issuing money that they were counting on to execute investment spending, but we have not really seen that happening yet, and it's something that we're monitoring closely.

These are issues which will be covered, of course, extensively in the World Economic Outlook Presentation and in the Global Financial Stability Report that will be presented and extensively discussed in the days leading up to the annual meetings in a couple of weeks time. Any other questions? If not, I thank you all again for coming.

IMF EXTERNAL RELATIONS DEPARTMENT

| Public Affairs | Media Relations | |||

|---|---|---|---|---|

| E-mail: | publicaffairs@imf.org | E-mail: | media@imf.org | |

| Fax: | 202-623-6220 | Phone: | 202-623-7100 | |