The expected recovery in sub-Saharan Africa is slower than in other regions, leading to widening divergences. (photo: peeterv by Getty Images)

Seven Charts that Show Sub-Saharan Africa at a Crucial Point

October 26, 2021

After an unparalleled contraction in 2020, sub-Saharan Africa is set to grow by 3.7 percent in 2021 and 3.8 percent in 2022. The recovery is supported by rising commodity prices, improving global trade and financial conditions. But this welcomed rebound is relatively modest by global standards, leading to a widening income disparity with developed economies.

Related Links

Seven charts taken from our latest Regional Economic Outlook tell the story of the forecast for sub-Saharan Africa:

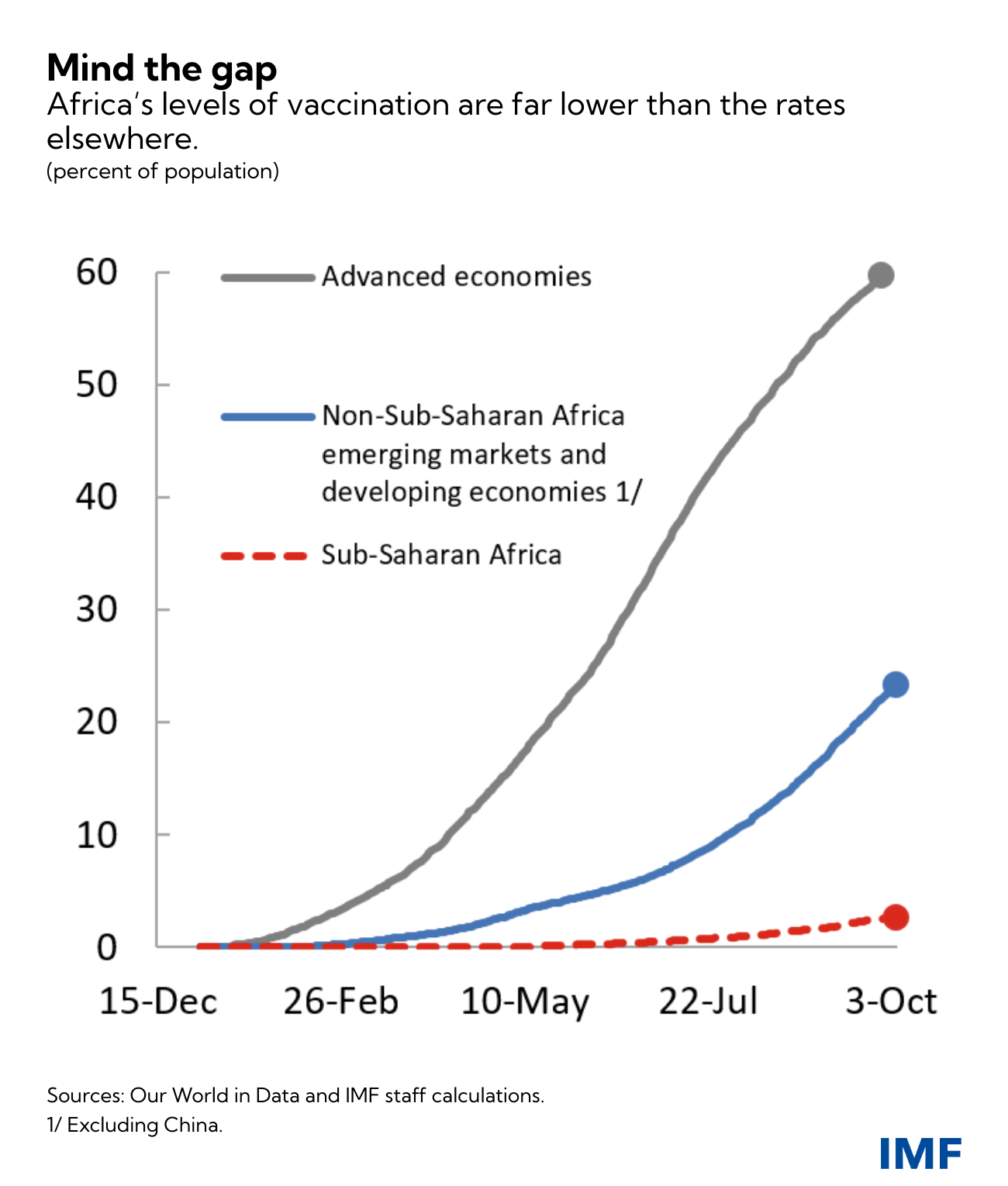

- The vaccine rollout in sub-Saharan Africa has been the slowest in the

world, leaving the region vulnerable to repeated waves of COVID-19. The

region has fully vaccinated only 3 percent of its population, well

below the level needed to reach herd immunity. Although the world is set to

produce around 12 billion doses in 2021, it will likely be more than a year

before a meaningful number of people are vaccinated in sub-Saharan Africa.

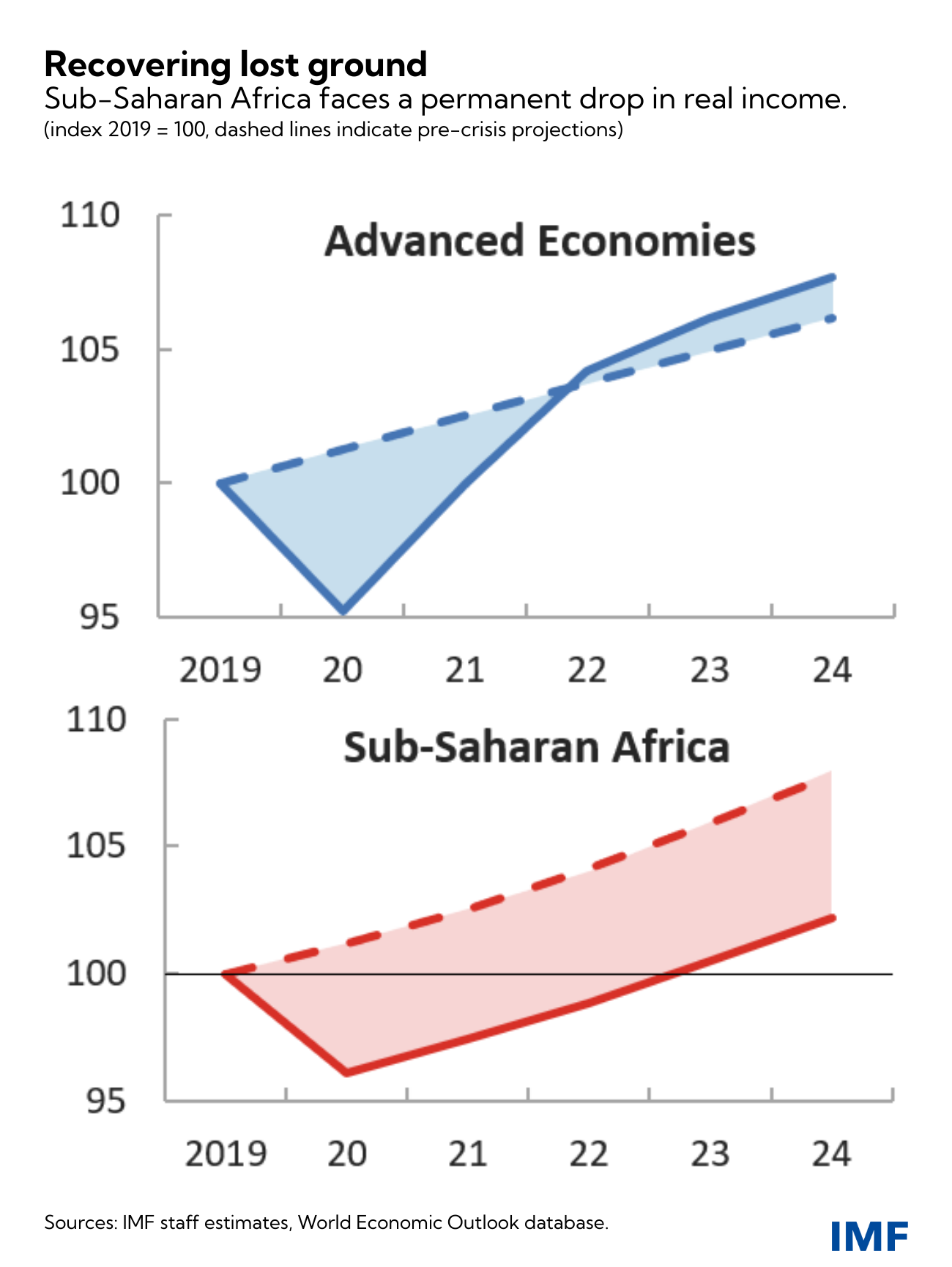

- The expected recovery is slower than in other regions, leading to widening

divergences. Differences in growth rates between regions are expected to

continue over the medium term amid persistent global disparities in vaccine

access and stark differences in the availability of policy support.

Advanced economies are forecasted to return to their pre-crisis growth path

by 2023. Sub-Saharan Africa, on the other hand, does not regain the lost

ground any time soon. The region would have to grow twice as fast in the

next three years to match the type of recovery seen in advanced economies.

- The pandemic has also worsened the pre-existing divergence across

sub-Saharan African countries and within individual countries. Even before

the pandemic, non-resource-intensive countries that have a diversified

economic structure had been growing faster than resource-rich countries.

But this gap has been exacerbated by the pandemic, which has highlighted

key disparities in resilience.

Similarly, the pandemic has elevated divergence within individual countries, along lines of employment, gender, geographic residence, socioeconomic status, and formal/informal workers. Rising food prices, combined with reduced incomes, also mean that households must reduce food consumption, threatening past gains in poverty reduction, nutrition, and food security.

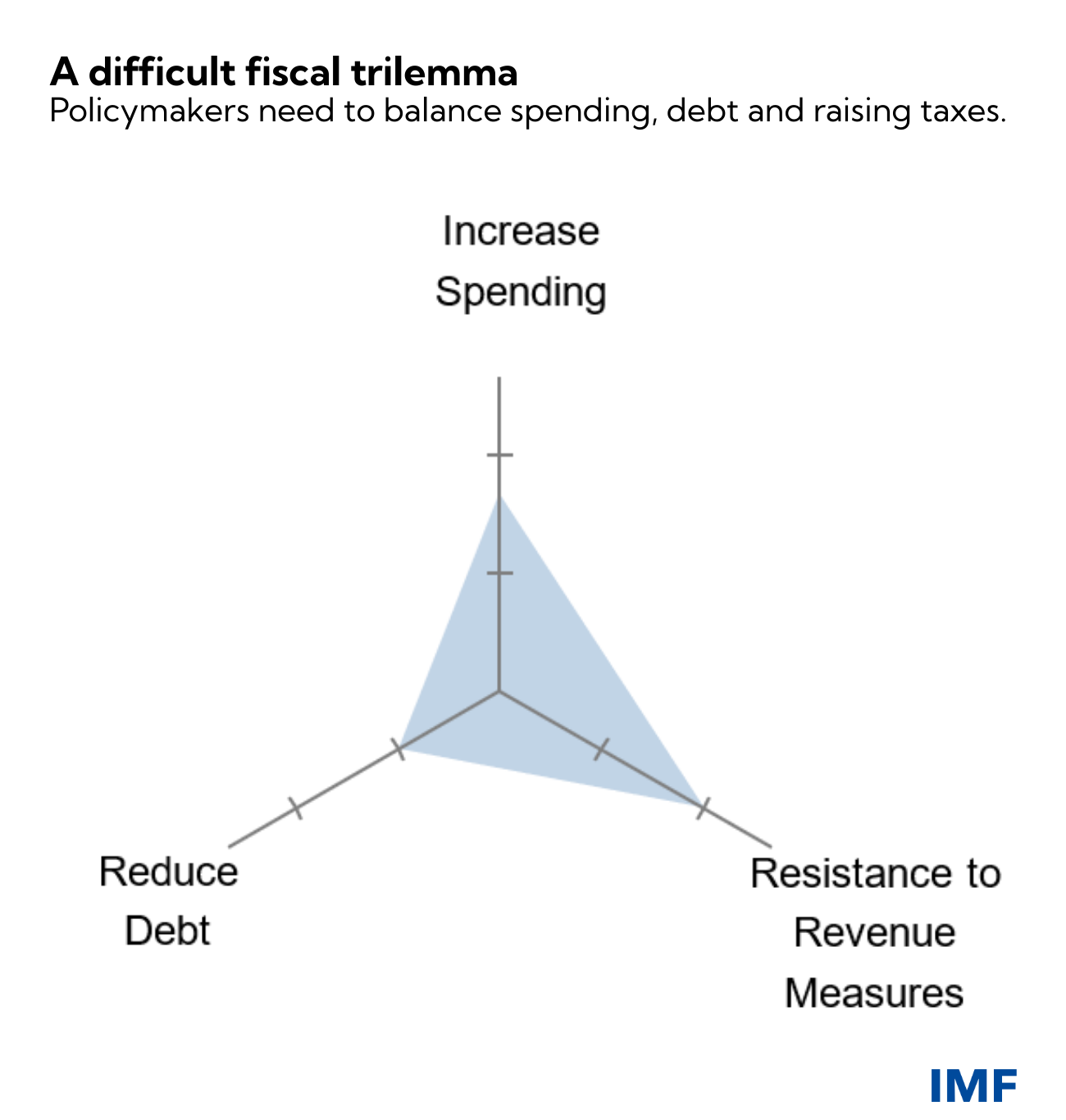

- Sub-Saharan African countries are facing a difficult fiscal policy

trilemma—balancing tradeoffs between pressing development-spending needs,

containing public debt, and mounting resistance to tax revenue

mobilization. Meeting these goals has never been easy, but the pandemic has

made it even more difficult. The spending needs of sub-Saharan Africa are

growing and becoming pressing as the pandemic takes a toll on health,

employment, education, infrastructure investment, and poverty reduction

efforts. Climate change adds to the burden.

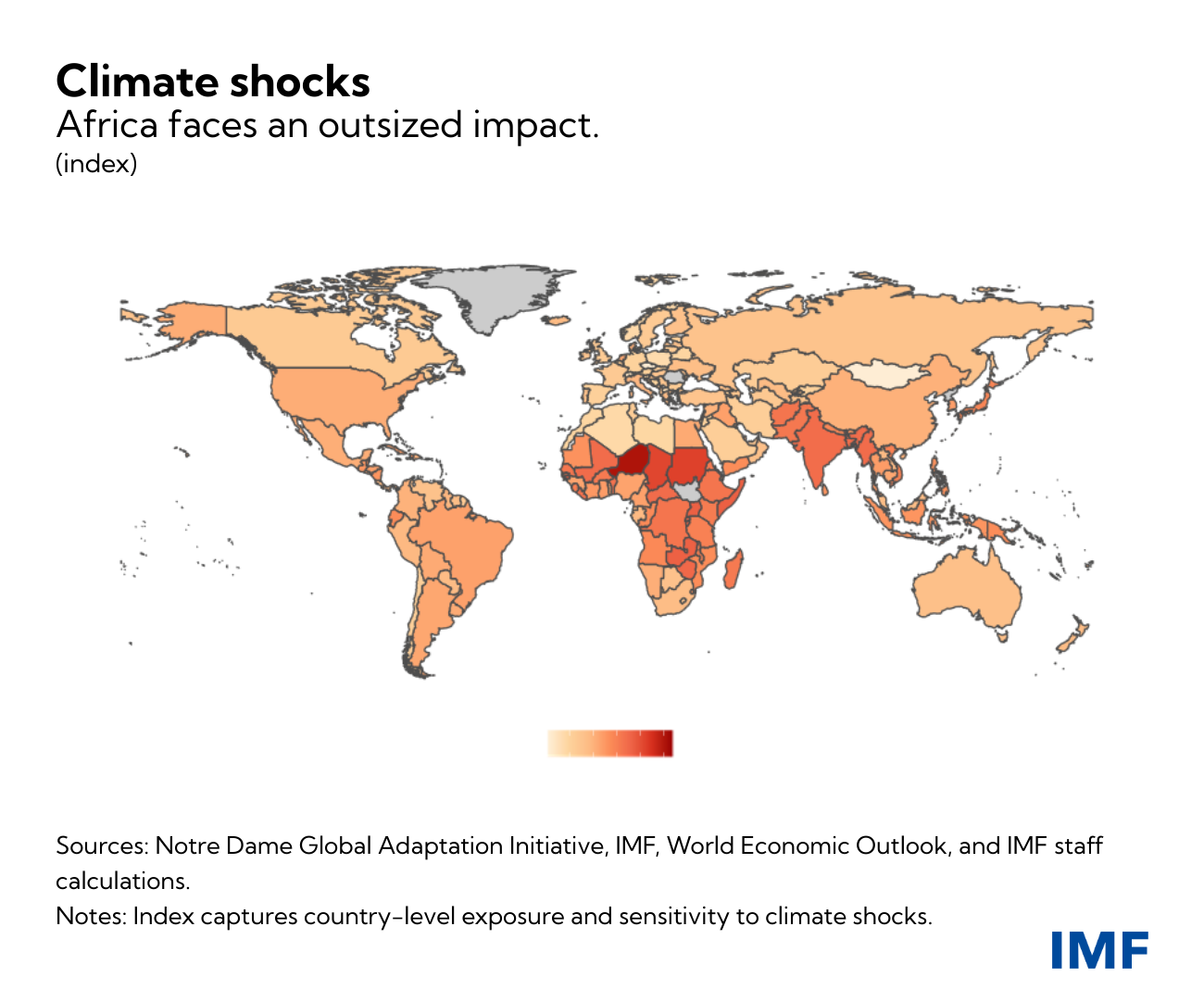

- Sub-Saharan Africa is the world’s smallest contributor to greenhouse gas

emissions—less than 5 percent of global emissions—but nonetheless the

region is perhaps the most vulnerable to climate shocks. One-third of the

world’s droughts already take place in sub-Saharan Africa, and its

dependence on rain-fed agriculture makes it particularly vulnerable.

Climate change can also act as a multiplier for conflict and fragility,

worsening pre-existing tensions, weak governance, and other socio-economic

concerns. Adapting to climate change, and assisting in worldwide mitigation

efforts, will require new and robust climate-finance mechanisms.

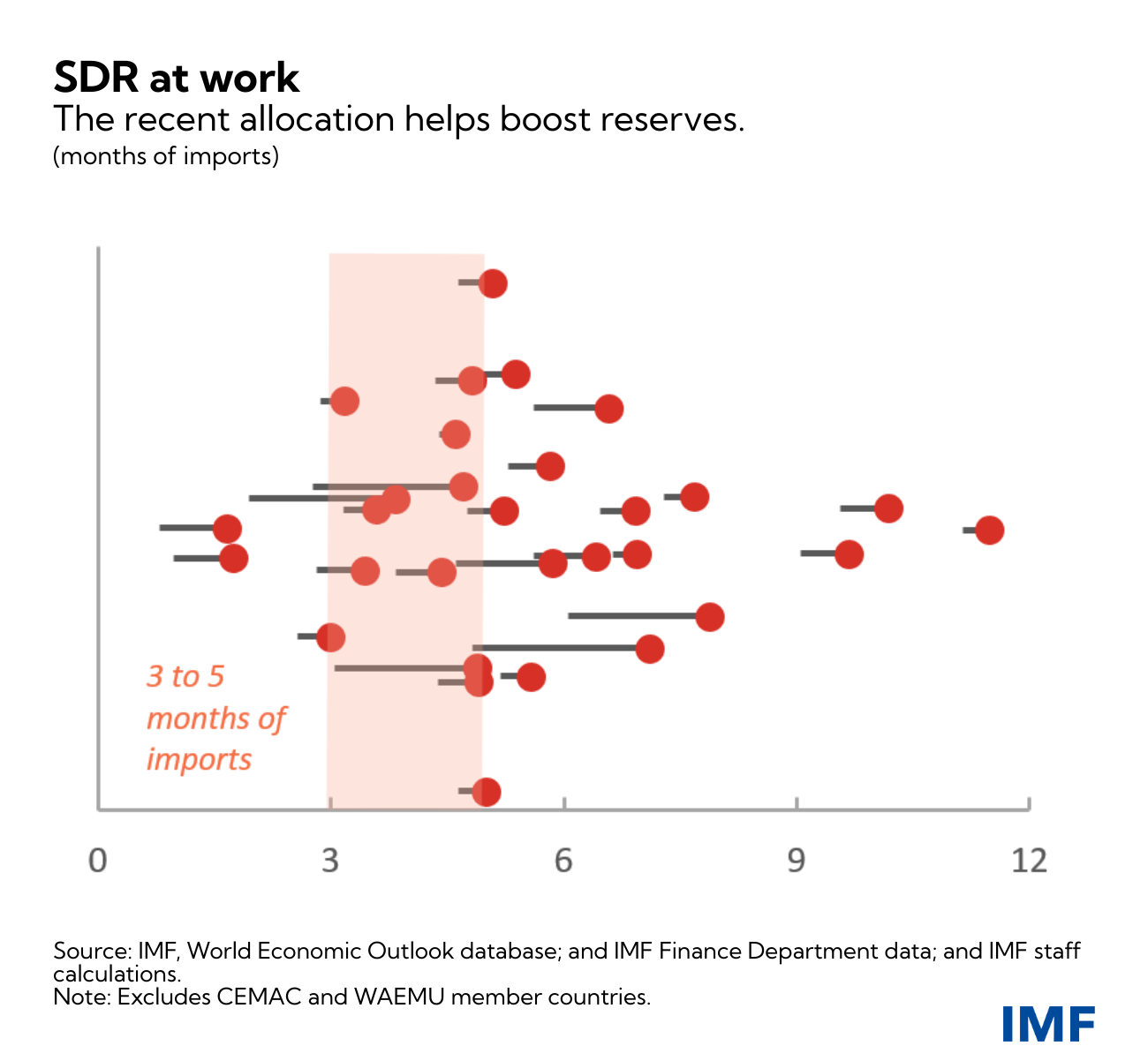

- International cooperation remains vital. Without external financial and

technical assistance, the divergent recovery paths of sub-Saharan Africa

and the rest of the world may harden into permanent fault lines,

jeopardizing decades of hard-won progress. So far, international

organizations and donors have mobilized swiftly to support the region.

Looking ahead, the voluntary channeling of Special Drawing Rights (SDR) from countries with strong external positions to those most in need

can further magnify the impact of the new SDR allocation. Used wisely,

these resources could shape the region’s post-pandemic recovery path.

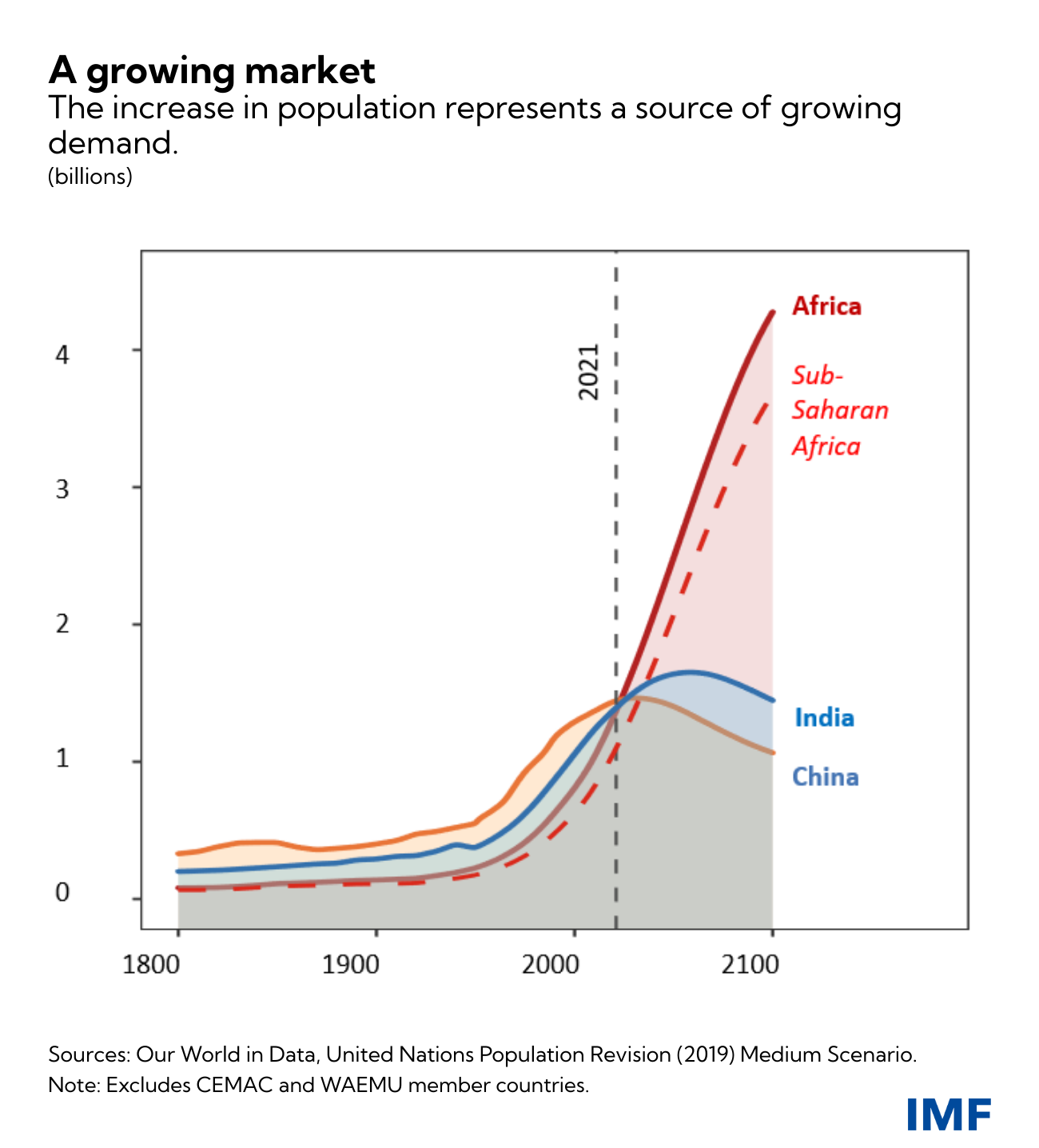

- Despite the difficult years ahead, the region’s potential as a source of

global demand remains undiminished. Over the next three decades, the global population is set to

increase by about 2 billion. Half of that growth will take place in

sub-Sahara Africa, as the region’s population is projected to double from

about 1 billion to 2 billion. This makes the region potentially one of the

world’s most dynamic economies, and one of its most important markets.