Emerging markets must balance overcoming the pandemic, returning to more normal policies, and rebuilding their economies

As the COVID-19 pandemic enters a second year, concerns are rising about how well emerging markets will fare. So far, they have been agile in responding to the economic fallout from the pandemic with unprecedented rescue packages for their hard-hit sectors and households. After a short-lived period of financial stress in March 2020, most emerging markets were able to return to global financial markets and issue new debt to meet their financing needs. However, in a global recovery in which some countries are rebounding faster than others and uncertainty is high regarding the pandemic, there is likely to be more market volatility. This will test the ability of policymakers in emerging markets to navigate a shifting landscape, manage their policy trade-offs, and achieve a durable recovery.

The emerging market universe is diverse and defies a uniform narrative. Although there is no formal definition, emerging markets are generally identified based on such attributes as sustained market access, progress in reaching middle-income levels, and greater global economic relevance (see box). Even so, these economies are dissimilar, and the distinction between emerging markets and other developing economies is also imprecise.

Emerging markets have made remarkable progress in strengthening their macroeconomic policies since the turn of the century, which helped them more than double per capita incomes on average. Monetary policies in 65 percent of the countries we have identified as emerging markets follow forward-looking inflation-targeting regimes, and inflation has fallen and stabilized in most. Public finances in several are guided by fiscal rules. Many embraced major banking sector reforms after the financial crises of the 1990s. Progress was tempered by the global financial crisis in 2008–09, but not derailed.

Good economic track record

This economic track record helped policymakers in emerging markets deploy bold measures during the pandemic without unraveling market confidence. Economic relief measures included increases in government spending, liquidity support to firms and banks, release of bank capital buffers with the intent to support lending, and asset purchase programs by central banks to stabilize domestic markets. Low domestic inflation and monetary easing by advanced economies also gave central banks in emerging markets room to cut domestic policy rates substantially. Household savings increased in most emerging markets following the onset of the pandemic. Much of the domestic savings went to finance the government, reducing the need for foreign borrowing, which, together with lower private investment, kept current account deficits in check.

However, some measures—such as direct monetary financing of budget deficits or temporary freezes on loan repayments—raise new risks. Policymakers defended them as temporary tools to alleviate enormous economy-wide strains. Higher fiscal deficits have also added to already elevated sovereign debt in some countries. In others, high corporate sector debt, including of state-owned enterprises, and unhedged foreign exchange exposures in corporate debt pose contingent fiscal risks in the event of corporate distress. Increased government debt held by domestic banks also intensifies the link between the health of the government and that of the banking system.

The pandemic is far from over, so it is too early to determine which measures have worked. Economic activity contracted sharply in most emerging markets in 2020. However, the IMF’s April 2021 World Economic Outlook estimates suggest that without the policy measures implemented across the world—including in advanced economies and emerging markets—the contraction in global GDP would have been three times worse.

What is an emerging market?

There is no official definition of an emerging market. The IMF World Economic Outlook classifies 39 economies as “advanced,” based on such factors as high per capita income, exports of diversified goods and services, and greater integration into the global financial system. The remaining countries are classified as “emerging market and developing” economies. Among these, 40 are considered “emerging market and middle-income” economies by the IMF Fiscal Monitor, based on their higher incomes.

Income isn’t the only characteristic of an emerging market. Most are economies with sustained strong growth and stability that can produce higher-value-added goods and are more like advanced economies not only when it comes to income, but also in participation in global trade and financial market integration. To identify an emerging market, we looked at

- Systemic presence: The size of the country’s economy (nominal GDP), its population, and its share of exports in global trade

- Market access: The share of a country’s external debt in global external debt, as well as whether it is included in global indices used by large international institutional investors and the frequency and amount of international bonds issued

- Income level: A country’s GDP per capita in nominal US dollars

We derive a score for each economy not considered advanced, using five weighted variables:

- 0.40×nominal GDP+

- 0.15×population+

- 0.15 ×GDP per capita+

- 0.15×share of world trade+

- 0.15×share of world external debt

If a country is ranked in the top 20 for 2010–20, it receives a score of 1 for that variable. Otherwise, it is assigned zero. The final score is calculated as the weighted sum of the individual scores. This approach identifies the following countries in the emerging market group, in alphabetical order: Argentina, Brazil, Chile, China, Colombia, Egypt, Hungary, India, Indonesia, Iran, Malaysia, Mexico, the Philippines, Poland, Russia, Saudi Arabia, South Africa, Thailand, Turkey, and the United Arab Emirates. Two countries were excluded: Nigeria because of its classification as a low-income country (eligible for IMF Poverty Reduction and Growth Trust financing) during the sample period considered (2010–20) and Qatar because of its population of less than 5 million.

These 20 emerging market countries account for 34 percent of the world’s nominal GDP in US dollars and 46 percent in purchasing-power-parity terms. These countries are also featured in commonly used indices for emerging markets, such as those of J.P. Morgan, Morgan Stanley Capital International, and Bloomberg.

FRANCISCO ARIZALA is an economist and DI YANG is a research analyst in the IMF’s Strategy, Policy, and Review Department.

Divergent responses

Divergent recoveries in emerging markets reflect differences in economic positions and policy responses. Those that were able to contain the virus or inoculate their populations (such as China and the United Arab Emirates) are recovering earlier. Those with ample fiscal buffers, market access, or both were able to deploy greater fiscal support (such as the Philippines and Poland). Central bank credibility allowed some to cut policy rates to record lows and engage in unconventional monetary policy without severe exchange rate pressure (Fratto and others 2021). Emerging markets with macroeconomic imbalances or elevated debt burdens continue to face sharp trade-offs between supporting recovery and reducing imbalances (among them Argentina, Egypt, and Turkey).

The road ahead could be somewhat bumpier. Because of threats from new COVID-19 strains, countries will have to weigh the many trade-offs between continued efforts to mitigate spread of the virus—which will likely require maintaining economic support to households and firms—and normalizing policies and rebuilding economic resilience. Securing adequate vaccines is only a first step. Financial market volatility against a backdrop of rising US long-term rates must be deftly managed, particularly for countries with large external financing needs. And political and social support will be central to implementing structural reforms. There are a number of areas requiring policy action, although the priorities will vary from country to country.

Targeting corporate sector support: As the health crisis comes under control, countries must begin to transition from wholesale crisis emergency support measures to those that target support to viable firms and eventually allow a handover to private-led growth. How fast this can be done will depend on the link between growth and employment in the corporate sector and whether a country can afford to support viable firms long enough to allow them to shake off pandemic-induced distress. How efficiently that happens will depend on the strength of labor market institutions, safety nets, banking system oversight, and insolvency procedures for a smooth reallocation of resources. As shown in the IMF’s April 2021 Global Financial Stability Report, distinguishing between corporate liquidity and solvency will not be easy. Some companies in emerging markets entered the crisis with already elevated debt, and the economy-wide implications of corporate distress need to be better assessed.

While advanced economies face similar challenges, the ensuing trade-offs are likely to be more acute for emerging markets because they typically face more imposing budget constraints. Emerging markets also tend to have weaker frameworks to deal with corporate bankruptcies. Policy interventions must therefore be designed to reduce both risks from excessive liquidations that lead to a wave of bankruptcies and risks of creating zombie firms that can operate on excessive credit support but cannot invest in new activity (Pazarbasioglu and Garcia Mora 2020). Past experience (such as Poland in 1992, Mexico in 1994, many southeast Asian countries in 1997–98, and Turkey in 2001) suggests that successful strategies include timely asset quality reviews as well as a combination of out-of-court workouts, debt relief, and disposal of nonperforming assets (Araujo and others, forthcoming).

Because bank-based financing is more prevalent than market financing in emerging markets, corporate distress could affect financial stability if banks have to recognize increased loan losses after the pandemic. To provide greater transparency, bank asset quality reviews may be necessary in some cases—especially because regulatory measures were eased during the crisis. The rise of shadow, or nonbank, financing of the corporate and household sectors in some emerging markets also raises risks because the nonbank sector is largely unregulated. Hence, a longer-term priority is designing stronger debt resolution and insolvency regimes and developing so-called macro-financial tools to monitor risks to the overall economy from the nonbank financial sector.

Generating job-rich, balanced, and sustainable growth: Beyond the immediate recovery, a vital step toward long-term economic health is raising productivity and lessening the scarring effects of the crisis on investment, employment, human capital (because of setbacks to learning), and financial system strength. The long-term growth payoffs from structural reforms can be significant if they are well designed and properly sequenced (Duval and Furceri 2019). Some priorities include

- introducing market-oriented reforms, including for state-owned enterprises (such as in China, India, and Mexico)

- strengthening social safety nets (for example, in Chile and China)

- closing infrastructure gaps (for example, in Indonesia and the Philippines)

- implementing pension, product market, labor market, and governance reforms in many countries

Clear communication on policy intentions, with measures to protect the vulnerable, is essential as well to building social support for difficult reforms.

It is also the time to build stronger economies than emerging markets had before the pandemic—by taking steps to create better and more equal access to health care and education, strengthening public infrastructure, and retraining workers displaced by the pandemic. Building resilience to climate change and steering digitalization for inclusive growth are also necessary. COVID-19 has caused more loss of human life in countries with weak health systems and social safety nets. It has triggered greater economic losses in service-oriented sectors and among unskilled, young, and female workers. To ensure a sustained recovery that does not leave anyone behind, the rise in inequality and poverty must be contained. Reducing informality, which accounts for one-fourth to one-third of the economy for most emerging markets (Medina and Schneider 2019), will allow more people to benefit from better wages and redistributive measures.

Some countries are seizing opportunities: in Asia, digitalization is transforming the efficiency of production, communication, and the inclusiveness of government operations (Gaspar and Rhee 2018). Indonesia is addressing the threat from deforestation through a program on sustainable land use. Some emerging markets, such as Malaysia, are strengthening the financial regulatory framework to better monitor and manage transition risks as they move to reduce the economy’s carbon footprint.

Restoring macroeconomic resilience: The crisis was a sore reminder of the importance of building economic health during peaceful times. Emerging markets will soon need to start rebuilding fiscal, external, and macro-financial buffers to prepare for the next crisis. That means reestablishing fiscal rules and restoring financial regulatory standards, which were set aside during the pandemic, and rebuilding external reserves if they are running low. Priorities will vary and will need to be addressed without hurting growth prospects—raising tax capacity for spending on public services where safety nets are weak, taking steps to reduce debt and debt accumulation (fiscal consolidation) where the sovereign debt burden is high, and tightening macroprudential policies on financial institutions where financial stability risks are elevated.

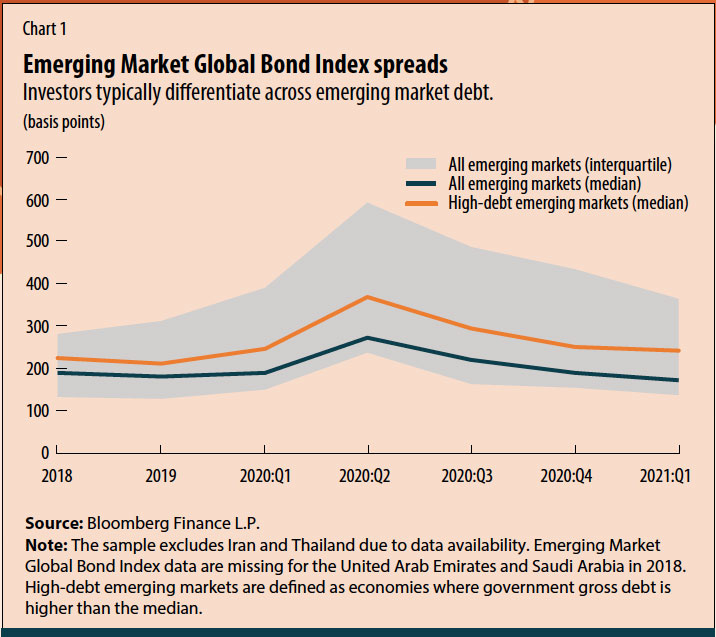

Governments in many emerging markets will need to balance different goals, such as raising spending on public investment and social safety while resuming fiscal consolidation to keep public debt on a firm downward path. Public and external debt have risen significantly for the median emerging market economy, reaching 59 and 44 percent of GDP, respectively, in 2020, and gross financing needs are projected to stay above 10 percent of GDP in 2020–21. While low global interest rates have kept debt servicing costs manageable, external borrowing costs should not be expected to stay low indefinitely. Investors typically differentiate across emerging market debt (see Chart 1). Even when debt is incurred in domestic currency, the sizable share of domestic debt held by foreigners makes the domestic financial market an important transmitter of external financial shocks (see Chart 2). Sustained high debt and gross financing needs will likely aggravate policy trade-offs and expose emerging markets to abrupt changes in the risk appetite of investors.

As the IMF’s April 2021 Fiscal Monitor argues, stronger tax revenue generation would allow policymakers to provide better public services without adding to debt burdens. Tax revenues in emerging markets indeed stand below 20 percent of GDP on average compared with over 25 percent of GDP in advanced economies. Emerging market governments also tend to spend a higher share of their revenues to meet interest payments.

In the post-pandemic environment, policy space has shrunk. With higher fiscal deficits and debt, larger financing needs, and less room to cut domestic interest rates, policies must therefore be better integrated to achieve the best outcomes for growth and stability, while maintaining the autonomy of fiscal, monetary, and regulatory authorities. For example, where inflation pressure is subdued, monetary policy can continue to support domestic demand, even as fiscal support is withdrawn.

Other policy trade-offs must also be managed as multispeed recoveries give

rise to market pressure. While a flexible exchange rate generally acts as

an external shock absorber, under some conditions, the effects can be the

opposite. For instance, depreciation in the domestic currency can increase

the stock of foreign-exchange-

denominated liabilities, further intensifying market pressure. Pass-through

from depreciation can generate inflation pressure when monetary policy

credibility is not fully established. Concerns about navigating financial

volatility are foremost in the minds of many policymakers in emerging

markets and are a major plank of the IMF’s work on the Integrated Policy

Framework.

Rebuilding resilience

Past crises demonstrate that emerging market policymakers can overcome adverse shocks and rebuild economic resilience. Moreover, medium-term growth in most emerging markets is projected to remain strong. However, a collective global effort is crucial for emerging markets to realize their growth potential and generate much-needed dynamism in global activity, trade, investment, and finances.

First, emerging markets must reclaim their hard-won macroeconomic strength , as they did after the financial crises in the 1990s and early 2000s and the global financial crisis that began in 2008. With recovery from the pandemic proceeding at divergent speeds, emerging markets must also learn from one another how best to navigate risks and maintain resilience. This affects more than just emerging markets. With their growing systemic relevance in the global economy, a strong emerging market universe will also drive global stability.

Second, major advanced economies must do their part: Multilateral cooperation on free trade, vaccine supply, and taxes; commitment to providing dollar liquidity under resurgent financial stress; and joint action toward climate change are all essential. Some emerging markets will need financing support to invest in building back stronger without further aggravating climate change.

Third, global development and financial institutions must be complementary in their efforts: For the IMF, this will mean working through its key responsibilities—policy dialogue and advice, financial support, including through precautionary lines, and capacity building—serving as a convening platform for cross-country learning and leveraging relevant expertise from other international institutions to help its most dynamic member countries regain their footing in the post-pandemic landscape.

RUPA DUTTAGUPTA is a division chief in the IMF’s Strategy, Policy, and Review Department.

CEYLA PAZARBASIOGLU is director in the IMF’s Strategy, Policy, and Review Department.

References:

Araujo, J., J. Garrido, E. Kopp, R. Varghese, and Y. Weijia. Forthcoming. “Corporate Debt Resolution in the Time of COVID-19.” IMF Departmental Paper, International Monetary Fund, Washington, DC.

Duval, R., and D. Furceri. 2019. “How to Reignite Growth in Emerging Market and Developing Economies.” IMFBlog, October 9.

Fratto, C., B. Harnoys Vannier, B. Mircheva, D. de Padua, and H. Poirson. 2021. “Unconventional Monetary Policies in Emerging Markets and Frontier Countries.” IMF Working Paper 21/14, International Monetary Fund, Washington, DC.

Gaspar, V., and C. Y. Rhee. 2018. “The Digital Accelerator: Revving Up Government in Asia.” IMFBlog, September 26.

Medina, L., and F. Schneider. 2019. “Shedding Light on the Shadow Economy: A Global Database and the Interaction with the Official One.” CESifo Working Paper 7981, Munich Society for the Promotion of Economic Research.

Pazarbasioglu C., and A. Garcia Mora. 2020. “Strengthen Insolvency Frameworks to Save Firms and Boost Economic Recovery.” World Bank Blog, May 18.

Opinions expressed in articles and other materials are those of the authors; they do not necessarily represent the views of the IMF and its Executive Board, or IMF policy.