Loading component...

Facing Crisis Upon Crisis: How the World Can Respond

April 14, 2022

Loading component...

IMF Communications Department

MEDIA RELATIONS

PRESS OFFICER:

Phone: +1 202 623-7100Email: MEDIA@IMF.org

April 14, 2022

PRESS OFFICER:

Phone: +1 202 623-7100Email: MEDIA@IMF.org

As prepared for delivery

1. Introduction

Thank you, Tino. It is a great honor for the IMF to partner with the Carnegie Endowment.

Our institutions are committed to shared peace and prosperity—especially vital goals at this crucial moment for the world we live in.

To put it simply: we are facing a crisis on top of a crisis.

First, the pandemic: it turned our lives and economies upside down—and it is not over. The continued spread of the virus could give rise to even more contagious or worse, more lethal variants, prompting further disruptions—and further divergence between rich and poor countries.

Second, the war: Russia’s invasion of Ukraine, devastating for the Ukrainian economy, is sending shockwaves throughout the globe.

Above all is the human tragedy—the suffering of ordinary men, women, and children in Ukraine, among them over 11 million displaced people. Our hearts go out to them.

The economic consequences from the war spread fast and far, to neighbors and beyond, hitting hardest the world’s most vulnerable people. Hundreds of millions of families were already struggling with lower incomes and higher energy and food prices. The war has made this much worse, and threatens to further increase inequality.

And for the first time in many years, inflation has become a clear and present danger for many countries around the world.

This is a massive setback for the global recovery.

In economic terms, growth is down and inflation is up. In human terms, people’s incomes are down and hardship is up .

These double crises—pandemic and war—and our ability to deal with them, are further complicated by another growing risk: fragmentation of the world economy into geopolitical blocs—with different trade and technology standards, payment systems, and reserve currencies.

Such a tectonic shift would incur painful adjustment costs. Supply chains, R&D, and production networks would be broken and need to be rebuilt.

Poor countries and poor people will bear the brunt of these dislocations.

This fragmentation of global governance is perhaps the most serious challenge to the rules-based framework that has governed international and economic relations for more than 75 years, and helped deliver significant improvements in living standards across the globe.

It is already impairing our capacity to work together on the two crises we face. And it could leave us wholly unable to meet other global challenges—such as the existential threat of climate change.

It is a consequential moment for the international community.

The actions we take now, together, will determine our future in fundamental ways. It reminds me of Bretton Woods in 1944 when, in the dark shadow of war, leaders came together to envision a brighter world. It was a moment of unprecedented courage and cooperation.

We need that spirit today, as we face bigger challenges and more difficult choices.

2. Bigger Challenges, More Difficult Choices

The global recovery was already losing momentum before the war in Ukraine, partly because of Omicron-related disruptions.

In January, we cut our global growth forecast to 4.4 percent for 2022. Since then, the outlook has deteriorated substantially, largely because of the war and its repercussions. Inflation, financial tightening, and frequent, wide- ranging lockdowns in China—causing new bottlenecks in global supply chains—are also weighing on activity.

As a result, we will be projecting a further downgrade in global growth for both 2022 and 2023. Fortunately, for most countries, growth will still remain in positive territory. That said, the impact of the war will contribute to forecast downgrades for 143 economies this year—accounting for 86 percent of global GDP.

Yet, as you will see in our World Economic Outlook next week, prospects vary greatly across countries: from catastrophic economic losses in Ukraine, to a severe contraction in Russia, to countries facing spillovers from the war through commodity, trade, and financial channels.

Economies facing downgrades include net importers of food and fuel—in Africa, the Middle East, Asia, and Europe.

Higher commodity prices have lifted growth prospects for many exporters of oil, natural gas, and metals. But these countries are also impacted by higher uncertainty, and their gains are far from enough to offset an overall global slowdown, largely driven by the war.

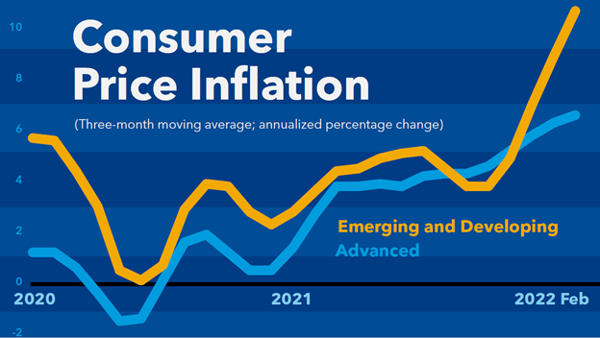

At the same time, higher energy and food prices are adding to inflationary pressures, squeezing real incomes of households around the world. [ Chart 1, below]

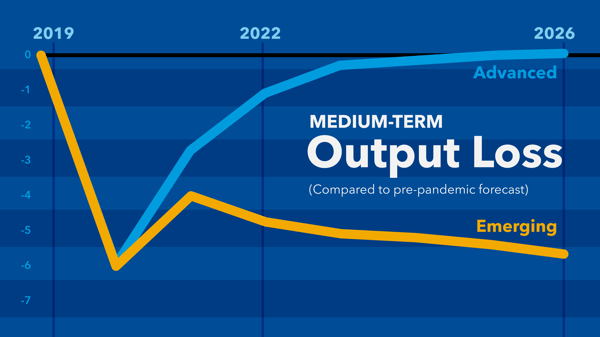

Medium-term prospects have also taken a hit.

For most countries, output is now expected to take even longer to return to its pre-pandemic trend. [Chart 2, below] Most emerging and developing countries are not just grappling with the economic fallout of the war, but also the scarring effects of the pandemic crisis. This includes job losses and learning losses—costs borne mostly by women and young people.

The recovery remains deeply divergent between rich and poor.

On top of this, the outlook is extraordinarily uncertain—well beyond the normal range. The war and sanctions could escalate. New Covid variants could emerge. Crops could fail.

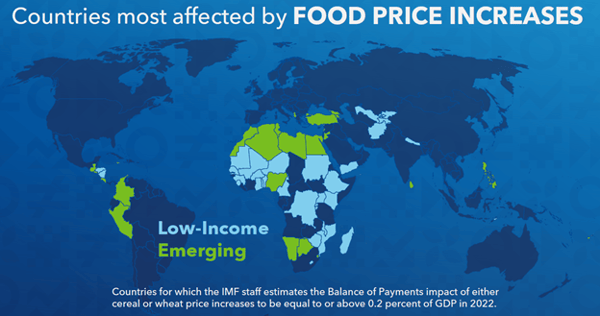

Before the war, Russia and Ukraine provided 28 percent of global wheat exports; Russia and Belarus supplied 40 percent of exports of potash, a crucial fertilizer. Now, grain and corn prices are soaring, and leaders across Africa and the Middle East are telling me that supplies are running low.

Food insecurity is a grave concern. [Chart 3, below] We must act now with a multilateral initiative to bolster food security. The alternative is dire: more hunger, more poverty, and more social unrest—especially for countries that have struggled to escape fragility and conflict for many years.

Food and energy prices, along with supply chain issues, continue to push up inflation. For advanced economies, inflation is already reaching a four-decade high. And we now project it to remain elevated for longer than previously estimated.

This is the most universally complex policy environment of our lifetime—posing tremendously difficult choices:

How can policymakers rein in high inflation and rising debt, while maintaining critical spending and building foundations for durable growth?

3. Policy Action to Safeguard the Recovery and Build Resilience

The immediate priorities are to end the war in Ukraine, confront the pandemic, and tackle inflation and debt.

End the war

We know from global experience that conflict is the enemy of development and prosperity. The high cost of war has crippled and continues to cripple so many countries.

As we hope for peace, we must do all we can to help Ukraine and all impacted countries.

For our part, the IMF stepped up with $1.4 billion in emergency financing to help meet Ukraine’s immediate spending needs. Last week, we also launched a special account that gives a secure way to provide further funding to Ukraine. And, together with international partners, we are preparing for the massive reconstruction effort that will be required.

We are also actively working to support Ukraine’s heavily affected neighbors such as Moldova—a country of just 2.6 million people which has already welcomed over 400,000 refugees. And we are stepping up support for the 20 percent of our member countries experiencing fragility or conflict.

Confront Covid

At the same time, Covid continues its deadly march. To fight it, we need a comprehensive toolkit that includes vaccines, testing, and anti-viral treatments. This should be deployed everywhere.

Recent analysis from IMF staff and our partners shows that this can be done for a modest $15 billion this year, and $10 billion each year thereafter.

Surely, if we have learned anything from the pandemic, it is that health security is economic security.

Tackle inflation

Just as important for economic security is tackling inflation.

Inflation is a threat to financial stability and a tax on ordinary people struggling to make ends meet. In many countries, it has become a central concern, and there is a rising risk that inflation expectations could become de-anchored, which could make inflation more entrenched and harder to control.

In the face of this challenge, central banks should act decisively, keeping their finger on the pulse of the economy and adjusting policy appropriately. And, of course, communicating clearly.

Emerging and developing economies face the added risk of potential spillovers from monetary tightening in advanced economies—not only higher borrowing costs but also the risk of capital outflows.

To address these challenges, countries should be prepared to use the full set of tools available. These range from extending debt maturities and using exchange rate flexibility to foreign exchange interventions and capital flow management measures. Helping countries nimbly respond in such circumstances is precisely why we recently updated the Fund’s institutional view on this topic.

These country-level tools need to be coupled with international efforts to help economies move safely through the monetary tightening cycle.

Maintaining access to liquidity is particularly crucial. IMF lending—currently over $300 billion—has helped our member countries significantly in this regard. As has last summer’s $650 billion SDR allocation. Low-income countries are using up to 40 percent of their SDRs on Covid-related priorities, like vaccines and other essential spending.

Address debt

But even with assistance, many policymakers face the difficult task of addressing rising debt. This is why spending must be carefully prioritized—on safety nets, health, and education—and targeted to the most vulnerable.

A credible medium-term fiscal path, including equitable tax policies, is key—it will help create the space needed to deliver this support, without compromising public debt sustainability.

For some countries—especially among the 60 percent of low-income nations already in or near debt distress—debt restructuring will be required. To help many of them, the G-20’s Common Framework for debt treatment must be improved with clear procedures and timelines for debtors and creditors.

It should also be expanded to other highly-indebted vulnerable countries that can benefit from creditor coordination. Timely and orderly debt resolution is in the interest of both debtors and creditors.

These steps alone will not bring a durable and inclusive recovery. For that, policymakers must stay focused on seizing the opportunities of the major structural transformations underway. The two most important are the green transition and the digital revolution.

Climate change

As the most recent UN climate report highlights, the threat to our planet is not going away. On the contrary, it is getting worse. We must mitigate it everywhere, adapt where necessary, and build resilience against the shocks to come.

We know what needs to be done: a comprehensive approach including carbon pricing and investment in renewables, with compensation and new opportunities for those adversely affected by the green transition. These measures can also bolster energy security.

The IMF is stepping up to help. Yesterday, our Executive Board approved the creation of a new Resilience and Sustainability Trust. By providing affordable longer-term funding and catalyzing private investment, it will help address macro-critical challenges such as climate change—and future pandemics.

The digital revolution

The final global issue I will touch on today is the digital revolution. This includes reskilling workers for an increasingly digital economy; unlocking the potential of innovations such as central bank digital currencies; and strengthening the regulatory framework around crypto-assets.

Over 100 of our member countries are actively investigating this crucial area—and we are assisting, with policy advice and capacity building.

We used to say ‘the future is digital’; now the future is here, bringing new sources of productivity, growth, and jobs!

4. Conclusion: Indivisible

Let me conclude:

In the past seven weeks, the world has experienced a second major crisis—a war on top of a pandemic. This risks eroding much of the progress we have made over the past two years, climbing back from Covid.

Add to this the growing threat of fragmentation into geopolitical and economic blocs.

In a world where war in Europe creates hunger in Africa; where a pandemic can circle the globe in days and reverberate for years; where emissions anywhere mean rising sea levels everywhere—the threat to our collective prosperity from a breakdown in global cooperation cannot be overstated.

The only effective remedy to these risks is international cooperation. It is our only hope for a fairer, more resilient future. And it is our duty.

With near universal membership, the IMF is a tried and tested platform for global collaboration. Drawing on the collective strength of our members, we are providing urgently needed policy advice and financing to those hardest hit by the double crisis. And we stand ready to work with our international partners to do even more.

At the Bretton Woods conference in 1944, U.S. Treasury Secretary Henry Morgenthau laid out an “elementary economic axiom” to help guide the founders of the IMF: “Prosperity, like peace, is indivisible.”

In today’s more shock-prone world, the challenges we face are just as indivisible. Our efforts to solve them must be indivisible as well.

Thank you.

# # #

Chart 1:

Chart 2:

Chart 3: